Glossary

A space to share our views and insights on the industry.

Real-Time Payments (RTP) Laundering Risks

Real-Time Payments (RTP) laundering risks refer to the misuse of instant payment systems to move, layer, or cash out illicit funds at high speed. These risks arise when criminals exploit payment rails that allow funds to be transferred almost instantly, often with limited time for financial institutions to detect, investigate, or stop suspicious activity before the money moves onward.

Real-time payment systems are designed for speed, convenience, and certainty. But those same features can be misused by fraudsters, mule networks, scam syndicates, and money laundering groups to move proceeds across accounts, wallets, payment service providers, and banks within minutes or seconds.

How Real-Time Payments Can Be Misused

Criminals may use real-time payment channels to receive scam proceeds, fragment funds across multiple mule accounts, rotate beneficiaries, or quickly move money into cash, crypto, remittance channels, or offshore accounts.

Common misuse patterns include:

- Scam victims authorising payments to fraudster-controlled accounts

- QR codes redirecting funds to unintended beneficiaries

- Mule accounts receiving multiple small-value instant transfers

- Rapid pass-through activity with little or no retained balance

- Funds split across several accounts shortly after receipt

- Dormant or newly opened accounts suddenly receiving frequent credits

- PayNow, UPI, PayID, Osko, FAST, wallet, or instant-transfer channels being used to layer funds

Because many RTP transactions are authorised by the customer, they may pass authentication checks even when the underlying purpose is fraudulent. This makes behavioural and beneficiary-level monitoring critical.

Why RTP Laundering Is Difficult to Detect

Traditional transaction monitoring systems may struggle to detect RTP laundering because individual payments can appear normal in isolation. A small transfer, a QR payment, or a peer-to-peer transaction may not trigger concern on its own.

The risk becomes clearer when institutions connect multiple signals, such as sender diversity, transaction velocity, beneficiary behaviour, payment references, device links, account age, and rapid onward movement.

In real-time payment environments, the detection window is narrow. By the time a victim reports the scam or an alert is reviewed, the funds may already have been dispersed across mule accounts or converted into other value stores.

Red Flags of RTP Laundering

Financial institutions should monitor for patterns such as:

- Multiple inbound payments from unrelated senders into the same account

- Sudden activity in dormant or low-activity accounts

- Repeated QR-linked or instant-payment credits

- Payment references mentioning prizes, donations, fees, gambling, investments, or urgent support

- Rapid outbound transfers shortly after funds are received

- Funds split across multiple accounts within a short period

- Frequent beneficiary additions or changes

- Low retained balances after high transaction volume

- Multiple accounts sharing devices, IP addresses, phone numbers, or identity attributes

- Customer complaints or fraud reports linked to the same recipient account

The strongest signal is often not one suspicious transaction, but a repeated pattern of fast-moving funds across connected accounts.

Examples of RTP Laundering Typologies

RTP laundering can appear across several scam and financial crime typologies, including:

- QR code donation diversion: Fraudsters replace legitimate donation QR codes with codes linked to their own accounts.

- PayNow-linked account misuse: Criminal actors use shared or surrendered access to genuine customer accounts to move illicit funds.

- Fake gambling or “scambling” networks: Scam proceeds are moved through fake online gambling platforms and mule accounts using instant payments.

- UPI jumped deposit scams: Victims unknowingly authorise larger outbound payments after receiving small inbound credits.

- Authorised push payment scams: Victims are manipulated into initiating transfers to fraudster-controlled accounts.

Why It Matters for Financial Institutions

RTP laundering sits at the intersection of fraud, payments, and AML. A transaction may begin as a scam loss, but once the funds move through mule accounts, payment wallets, bank accounts, or remittance channels, it becomes a wider financial crime and money laundering concern.

Banks, fintechs, payment service providers, and wallet operators need monitoring systems that can identify not just the first payment, but the wider money trail that follows.

Effective detection requires a connected view of customer behaviour, beneficiary risk, account relationships, payment velocity, and network-level movement.

How FinCense Helps

Tookitaki’s FinCense helps financial institutions detect RTP laundering patterns by combining transaction monitoring, behavioural analytics, mule account detection, screening, and case management in one platform.

FinCense can help identify unusual payment velocity, multiple victim payments into common beneficiaries, rapid onward transfers, dormant account reactivation, suspicious QR or instant-payment behaviour, shared device or identity indicators, and connected account networks.

Through the Anti-Financial Crime (AFC) Ecosystem, FinCense also helps institutions stay updated on emerging typologies, allowing them to respond faster as criminals adapt to new real-time payment channels.

Key Takeaway

Real-time payments have transformed financial access and convenience. But their speed can also be exploited by criminals to move illicit funds before traditional controls can respond.

For financial institutions, the priority is clear: detect the money trail in real time, connect fraud and AML signals, and identify laundering behaviour before funds disappear across the network.

Financial Abuse in Domestic Relationships

What is financial abuse in domestic relationships?

Financial abuse in domestic relationships refers to the misuse of money, assets, accounts, credit, financial access, or economic dependence to control, exploit, isolate, or harm another person within an intimate, family, household, or caregiving relationship.

Unlike many forms of financial crime, financial abuse often takes place behind a layer of trust. The perpetrator may be a spouse, partner, family member, caregiver, employer, or authorised representative. The victim may appear to be willingly carrying out transactions, but the activity may be driven by coercion, manipulation, fear, dependence, or misuse of authority.

For financial institutions, this creates a complex detection challenge. The transaction may look legitimate on paper, but the behaviour behind it may indicate exploitation.

Why financial abuse matters in financial crime compliance

Financial abuse is not only a social harm issue. It can also become a financial crime risk when the victim’s accounts, assets, identity, or authority structures are misused to move, disguise, or launder funds.

In domestic settings, perpetrators may exploit:

- Shared household accounts

- Joint assets

- Power-of-attorney arrangements

- Elderly relatives’ retirement or trust accounts

- Foreign domestic worker accounts

- Victims’ savings, insurance products, or investments

- Personal information used for impersonation

- Emotional or economic dependence

This makes financial abuse difficult to detect because many transactions can appear consistent with ordinary family, caregiving, or household activity.

Common indicators of financial abuse

Financial abuse may involve visible and subtle warning signs. These indicators are not proof of abuse on their own, but they may justify closer review when seen together.

Common red flags include sudden changes in account activity, unexplained liquidation of long-term savings, new beneficiaries or payout instructions, rapid transfers out of joint accounts, unusual remittance patterns, repeated small withdrawals from elderly customers’ accounts, and high-value instructions made through channels inconsistent with the customer’s usual behaviour.

Other warning signs may include a third party speaking on behalf of the customer, customers appearing confused or pressured, inconsistent explanations for transactions, sudden use of digital channels by customers who usually prefer branch or assisted banking, and account activity that benefits another party more than the named account holder.

How financial abuse can become a laundering risk

Financial abuse can intersect with money laundering when exploited funds are moved into criminal activity or when victim-controlled accounts are used as conduits for illicit proceeds.

For example, a victim may be forced to liquidate legitimate savings, with the funds later mixed with proceeds from drug trafficking. An elderly customer’s retirement account may be drawn down in structured amounts to disguise theft. A foreign domestic worker may be coerced into receiving and remitting illicit funds under the cover of routine worker remittances. A spouse may impersonate a partner to access equity from shared household assets and move the funds into accounts they control.

In each case, the abuse is not only the extraction of money. It is also the misuse of trusted relationships to conceal the source, ownership, control, or purpose of funds.

Key scenarios under financial abuse in domestic relationships

1. Forced liquidation of savings used to finance drug trafficking

In this scenario, a domestic abuser coerces the victim into liquidating long-term assets such as fixed deposits, insurance-linked savings plans, retirement products, or investment holdings. The reason may be framed as an urgent family need, debt pressure, or relationship obligation.

The payout is redirected to an account controlled by or accessible to the abuser. The funds are then used to support drug trafficking activity, including procurement, transport, or distribution. Once narcotics are sold, the proceeds may be mixed with the victim’s original funds and routed through linked accounts, cash-intensive businesses, or third-party payment channels.

The key risk is that legitimate victim-owned money becomes intertwined with criminal proceeds, making the laundering chain harder to identify.

2. Power-of-attorney abuse through structured elder account drawdowns

Here, a trusted family member misuses power-of-attorney authority over an elderly relative, often someone experiencing cognitive decline. The perpetrator uses this authority to draw funds from retirement accounts, trust accounts, or savings.

Instead of taking a single large amount, the perpetrator structures the activity through moderate transfers into the elder’s main deposit account or accounts controlled by the perpetrator. These funds are then withdrawn in smaller, staggered transactions that resemble routine expenses or business activity.

Detection becomes harder when the elder holds accounts across multiple institutions, as no single institution may see the full pattern of drawdowns.

3. Foreign domestic worker accounts used as laundering conduits

In this scenario, an employer engaged in criminal activity coerces a foreign domestic worker into opening or maintaining a financial account. The employer deposits illicit proceeds into the worker’s account and describes the payments as bonuses, service payments, household support, or other seemingly legitimate transfers.

The worker is then instructed to send the funds outward through remittances or account transfers labelled as family support, debt repayment, or personal obligations. To reduce detection, transfers may be split into smaller amounts and sent to multiple beneficiaries.

The abuse lies in the worker’s lack of real control. The laundering risk lies in the exploitation of the assumption that foreign worker remittances are routine and low risk.

4. Spousal impersonation fraud used to extract equity from household assets

This scenario involves a cohabiting spouse who uses intimate knowledge of the partner’s personal and financial details to impersonate them over voice or assisted banking channels. The perpetrator may fraudulently authorise drawdowns, refinancing, or withdrawals against funds or assets held in the partner’s name.

The proceeds are routed into a joint account to make the transaction appear like a legitimate household movement. Soon after, the funds are transferred to accounts controlled solely by the perpetrator.

Important red flags include sudden lump-sum credits into a joint account from a product not previously linked to household activity, rapid transfers to single-spouse accounts, and high-value instructions made through channels the genuine account holder does not typically use.

Why detection is difficult

Financial abuse is difficult to identify because the transaction may appear authorised, routine, or explainable. A spouse may have access to a joint account. A family member may legally hold power-of-attorney. A domestic worker may regularly send remittances. An elderly customer may make small withdrawals often.

The issue is not always the transaction itself. It is the pattern, context, and beneficiary of the activity.

Financial institutions need to look beyond isolated transactions and assess whether the behaviour aligns with the customer’s known profile, history, vulnerabilities, account purpose, and expected financial activity.

What financial institutions should monitor

Banks, fintechs, and payment providers should consider monitoring for patterns such as:

- Sudden liquidation of long-term savings or investment products

- Changes to payout instructions shortly before redemption

- New beneficiaries linked to high-value or unusual transfers

- Rapid movement of funds from joint accounts to one party’s sole account

- Structured withdrawals from elderly customers’ accounts

- Unusual account activity following power-of-attorney activation

- Foreign worker accounts receiving funds inconsistent with income profile

- Remittances to multiple unrelated beneficiaries

- High-value instructions through unfamiliar channels

- Customer behaviour suggesting pressure, confusion, fear, or lack of control

These indicators become stronger when seen together over time.

Controls that can help

Financial institutions can strengthen detection by combining transaction monitoring with customer risk context and behavioural indicators.

Useful controls include enhanced monitoring for vulnerable customer segments, periodic review of power-of-attorney and authorised representative activity, alerts for sudden liquidation of long-term products, detection of rapid outflows from joint accounts, relationship-based monitoring across linked accounts, and escalation workflows for suspected coercion or financial abuse.

Frontline staff training is also important. Branch, call centre, relationship management, and operations teams may notice behavioural signals before a transaction monitoring system does.

The role of technology

Technology can help institutions detect financial abuse by identifying patterns that are difficult to spot manually.

Advanced monitoring systems can connect customer profile data, account behaviour, transaction history, beneficiary relationships, digital activity, and case investigation notes. This helps investigators understand whether a transaction is part of a broader pattern of coercion, exploitation, or laundering.

AI-led alert prioritisation, network analytics, scenario-based monitoring, and behavioural baselining can also help institutions detect cases where activity appears legitimate in isolation but suspicious when viewed across time, accounts, and relationships.

Conclusion

Financial abuse in domestic relationships is a complex and often hidden form of harm. It sits at the intersection of trust, control, vulnerability, and financial crime.

For financial institutions, the challenge is to recognise that abuse may not always look like theft or fraud at first glance. It may appear as a family transfer, a routine remittance, a power-of-attorney instruction, a joint account movement, or a customer-authorised withdrawal.

The strongest defence is a context-led approach: understand the customer, monitor patterns over time, connect related accounts and parties, and escalate when financial activity suggests coercion, exploitation, or loss of control.

In modern financial crime prevention, detecting financial abuse is not only about protecting the institution. It is also about protecting vulnerable people from being used, controlled, or harmed through the financial system.

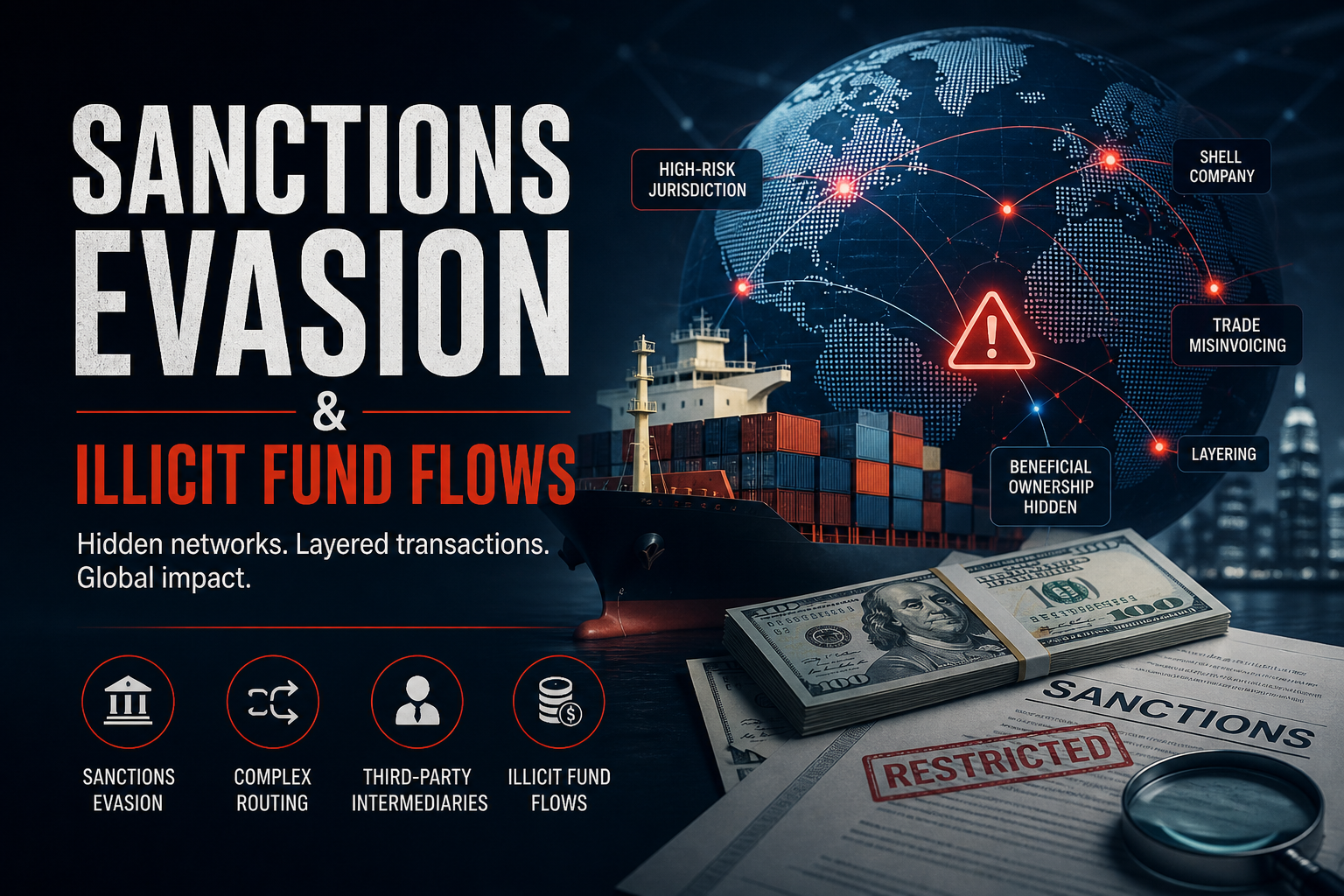

Sanctions Evasion & Illicit Fund Flows: What Financial Institutions Need to Watch

Sanctions evasion is no longer confined to a handful of high-risk jurisdictions or obvious counterparties. It has evolved into a complex, adaptive practice where illicit fund flows are carefully embedded within legitimate trade, payment, and financial activity.

For financial institutions, the challenge is not just identifying sanctioned entities. It is understanding how financial crime is being structured to avoid detection altogether.

What Is Sanctions Evasion?

Sanctions evasion refers to the deliberate attempt by individuals, entities, or networks to bypass economic or financial restrictions imposed by governments or international bodies.

These restrictions may target:

- Specific countries or regions

- Designated individuals or organisations

- Sectors such as energy, defence, or dual-use goods

Evasion occurs when actors restructure transactions, relationships, or financial flows to obscure their connection to sanctioned parties or restricted activities.

What Are Illicit Fund Flows in This Context?

Illicit fund flows are the movement of money that is illegal in origin, purpose, or destination — or structured to appear legitimate while concealing underlying sanctions exposure.

In sanctions evasion cases, these flows are often:

- Routed through multiple jurisdictions

- Split across accounts, entities, or payment types

- Embedded within otherwise legitimate commercial or financial activity

The objective is simple: make the movement of restricted value look like normal business.

How Sanctions Evasion Has Evolved

Traditional sanctions evasion relied on direct methods — undisclosed ownership, falsified documentation, or simple routing through less scrutinised jurisdictions.

Today, the approach is far more layered.

Evasion techniques now focus on:

- Embedding activity within legitimate systems (trade, payments, platforms)

- Fragmenting transactions to avoid visibility

- Using intermediaries with plausible commercial roles

- Creating narratives that justify the flow of funds

What makes this evolution significant is that individual transactions often appear commercially valid. The risk only becomes visible when viewed across relationships, timing, and behaviour.

Common Sanctions Evasion Typologies

While methods continue to evolve, several patterns are consistently observed across financial systems:

1. Trade-Based Concealment Through Intermediaries

Restricted goods or services are procured through third-country distributors or trading firms to obscure the true buyer and end use. Payments are fragmented across invoices, logistics costs, and service fees.

2. Corporate Service Payment Layering

Funds are routed as advisory fees, consulting charges, retainers, or administrative payments across multiple entities. The receiving parties may appear legitimate, but their commercial role is often unclear.

3. Merchant Settlement and Platform-Based Laundering

Illicit funds are embedded within merchant collections, refunds, and settlement flows processed through payment aggregators or digital platforms. Reversals and payout recycling add further complexity.

4. Humanitarian and NGO Channel Misuse

Transactions are structured as grants, field support payments, or programme expenses routed through NGOs or partner entities. The operational context appears legitimate, but visibility into end use is limited.

Key Risk Indicators Financial Institutions Should Track

Sanctions evasion rarely reveals itself through a single transaction. It emerges through patterns.

Some indicators to watch:

- Payments routed through third-country intermediaries without clear commercial rationale

- Fragmented settlement patterns across multiple accounts, currencies, or transaction types

- Repeated transactions involving entities with limited operational substance

- Payment flows that do not align with the customer’s business profile or expected behaviour

- Unusual use of refunds, reversals, or non-standard payment structures

- Complex chains involving multiple layers of counterparties with unclear relationships

The absence of transparency is often the strongest signal.

Why Detection Is Increasingly Difficult

The biggest challenge is that sanctions evasion is designed to blend in.

Each participant in the financial ecosystem sees only part of the activity:

- Banks see account behaviour

- Payment providers see transaction flows

- Trade participants see invoices and shipments

Individually, these signals may appear normal.

The risk lies in what connects them.

Without cross-entity visibility and contextual analysis, the broader pattern remains hidden.

What Needs to Change

Static rules and isolated monitoring are no longer sufficient.

Effective detection now depends on:

- Behavioural monitoring, not just transaction thresholds

- Network-level analysis across entities, accounts, and flows

- Real-time detection capabilities to identify evolving patterns

- Scenario-driven intelligence based on real-world typologies

- Stronger collaboration across institutions and jurisdictions

Sanctions evasion is not a single event. It is a coordinated process.

Detection needs to reflect that.

Final Thought

Sanctions evasion today is less about breaking the rules directly and more about rewriting the appearance of compliance.

Funds move.

Transactions clear.

Everything looks normal.

Until it doesn’t.

For financial institutions, the focus must shift from identifying isolated anomalies to understanding the broader financial story being constructed.

Because in sanctions evasion, what matters is not just where the money goes — but how convincingly it gets there.

Infrastructure Kickbacks and Laundering via Public Works

Definition

Infrastructure kickbacks and laundering via public works refer to the misuse of large-scale government-funded infrastructure projects — such as road construction, public housing, water systems, or digital connectivity programmes — as vehicles for bribery, embezzlement, and money laundering. In this typology, public officials and private contractors collude to inflate project costs, manipulate procurement processes, and channel illicit profits through complex financial transactions that disguise the true origin of funds.

Public infrastructure projects in Southeast Asia and Australia involve billions of dollars annually, creating an environment vulnerable to corruption and financial crime. When oversight gaps or opaque procurement systems exist, these projects become ideal channels for siphoning public funds and reintegrating them into the legitimate economy. The schemes often operate under the guise of legitimate payments to contractors, consultants, or subcontractors, masking kickbacks and illicit enrichment as normal business expenses.

This typology is not limited to developing economies. Even in advanced jurisdictions like Singapore and Australia, corruption risks persist through subcontracting networks, shell companies, and professional enablers who facilitate fund layering. The complexity of public works — involving multiple agencies, cross-border suppliers, and high transaction volumes — allows bad actors to exploit loopholes in procurement oversight and anti-money laundering controls.

How It Works (Modus Operandi)

At its core, this typology blends public-sector corruption with financial system exploitation. It typically follows a multi-stage process:

1. Procurement Capture and Tender Manipulation

The process begins with collusion between public officials and contractors to secure inflated tenders or exclusive contracts. Officials in charge of tender design, bidding, or approval manipulate criteria to favour pre-selected firms. In some cases, project budgets are padded during the planning phase, ensuring excess funds that can later be diverted.

In the Philippines, investigations into flood control and road improvement projects have revealed the use of ghost contractors — paper entities created to win bids and issue fake invoices for work never performed. These entities are often registered under relatives or associates of public officials, allowing the diversion of millions in public funds.

In Malaysia, procurement capture has been linked to politically connected contractors who dominate bidding for infrastructure works. Reports have highlighted inflated pricing for highway and public transport projects, with excess funds funnelled through consultancy fees and overseas accounts.

2. Use of Intermediary and Shell Entities

Once contracts are awarded, payments flow to legitimate contractors who then distribute portions to shell subcontractors or consultants. These intermediaries issue invoices for fabricated or overpriced services. The layering process begins here — funds are moved through multiple accounts, disguised as payments for materials, design work, or logistics.

In Singapore, while public procurement integrity remains high, vulnerabilities arise from cross-border subcontractors involved in foreign development projects. Offshore companies, especially those registered in low-tax jurisdictions, can act as fronts for laundering proceeds through consultancy payments or licensing fees.

In Australia, regulators have identified cases where contractors transferred funds to “associated entities” under the pretext of equipment leasing or subcontracting, masking the real flow of bribes. These transactions often involve large cash withdrawals, transfers to personal accounts, or conversions into real assets like vehicles and properties.

3. Integration of Illicit Proceeds

The final stage involves integrating the laundered funds into the legitimate economy. This can take the form of property investments, luxury asset purchases, or reinvestment into new business ventures. Some funds are recycled back into political campaigns or used to finance future projects, perpetuating a cycle of corruption and influence.

The Australian Federal Police have uncovered cases where kickbacks from regional construction projects were channelled through real estate investments in Sydney and Melbourne, using nominee owners to obscure beneficial ownership. Similarly, Philippine investigations have traced misappropriated infrastructure funds to casino junkets and offshore bank accounts, showing how illicit proceeds move fluidly between corruption and laundering typologies.

Red Flags / Risk Indicators

Financial institutions, auditors, and regulators play a crucial role in identifying anomalies tied to this typology. Common red flags and risk indicators include:

Transactional Red Flags

- Repeated payments to newly incorporated entities that have limited operational history or no online presence.

- Large payments classified as “consultancy,” “advisory,” or “subcontracting” services without clear supporting documentation.

- Round-number transactions or multiple payments just below reporting thresholds.

- Cross-border transfers to accounts in jurisdictions unrelated to the project’s scope.

- Frequent cash withdrawals following government disbursements or project payments.

- Unusual flow of funds between contractors, shell entities, and politically exposed persons (PEPs).

Behavioural and Operational Indicators

- Bidding patterns where a small group of companies repeatedly win public tenders.

- Similar language, formatting, or submission errors across different bidders, suggesting collusion.

- Family or business links between contractors and public officials involved in procurement.

- Rapid formation of subcontractors immediately before a project tender.

- Involvement of politically connected intermediaries or consultants with no technical role in the project.

Institutional Risk Factors

- Weak procurement oversight and insufficient post-award auditing.

- Decentralised project management structures that obscure accountability.

- Lack of beneficial ownership disclosure in contractor registration.

- Overreliance on paper-based or manual invoicing systems vulnerable to manipulation.

In Singapore, strong anti-corruption frameworks and digital procurement systems have mitigated several of these risks. However, financial institutions remain alert to foreign-linked transfers and politically exposed clients engaged in large-scale contracting.

In Malaysia and the Philippines, ongoing anti-corruption drives have revealed systemic issues, from weak supplier vetting to manipulation of project milestones.

In Australia, the integration of AML controls into public procurement compliance frameworks is improving, yet private contractors remain a high-risk node for laundering schemes.

Why It Matters (Industry Impact or Relevance)

The impact of infrastructure kickbacks and laundering via public works extends far beyond immediate financial loss. It erodes public trust, diverts funds from essential development, and undermines governance integrity. From an AML perspective, these schemes reveal how corruption and money laundering are intertwined, requiring cross-sector collaboration to detect and disrupt.

Economic and Reputational Costs

In the Philippines, the misuse of infrastructure funds in flood control and bridge projects has contributed to persistent development bottlenecks, while also fuelling public scepticism towards government spending. In Malaysia, scandals surrounding major transport projects have shaken investor confidence and triggered calls for procurement reform. Even in Australia, local government procurement audits have flagged conflicts of interest and weak contractor due diligence, highlighting vulnerabilities in mature economies.

Regulatory and Compliance Implications

For financial institutions, the typology underscores the importance of identifying corruption-linked laundering. Transactions linked to infrastructure contracts may appear legitimate but can conceal illicit activity. Banks and payment providers must enhance their risk assessment of clients involved in public-sector contracting, particularly those dealing with high-value projects, cash-intensive transactions, or politically exposed entities.

Regulators in Singapore and Australia have emphasised the need for beneficial ownership transparency and enhanced due diligence for government-linked payments. Meanwhile, initiatives in the Philippines and Malaysia are focusing on digital procurement platforms and e-payment monitoring to improve traceability and reduce human discretion in tender processes.

A Growing Regional Priority

Across the region, public infrastructure spending is accelerating — from the Philippines’ “Build Better More” initiative to Malaysia’s new transport corridors and Australia’s renewable energy projects. As investment scales up, so too does the incentive for illicit actors to capture these funds. The cross-border nature of supply chains and financial transactions makes collaborative intelligence essential to prevention.

The AFC Ecosystem and similar industry collectives play an important role in sharing red flags, typologies, and real-world scenarios that bridge the gap between anti-corruption enforcement and AML compliance. By democratising access to intelligence on how such schemes operate, financial institutions can strengthen early detection and prevent the integration of corrupt proceeds into legitimate channels.

Conclusion

Infrastructure kickbacks and laundering via public works exemplify how corruption, procurement fraud, and financial crime converge in high-value, high-impact sectors. For compliance professionals, detecting such schemes requires not only transactional vigilance but also contextual understanding — of who is being paid, for what purpose, and through which intermediaries.

As countries like Singapore, Malaysia, the Philippines, and Australia continue to invest heavily in infrastructure, this typology serves as a critical reminder: every road, bridge, or power plant is not just an economic asset — it’s a potential test of integrity, governance, and accountability. Strengthening financial oversight, data-sharing, and scenario-based monitoring is the surest path to ensuring that public wealth is protected from private corruption.

Tornado Cash

Introduction

In an era where financial privacy is increasingly valued, Tornado Cash has emerged as a powerful tool for preserving anonymity in cryptocurrency transactions. Tornado Cash leverages the principles of decentralization and cryptographic technology to provide users with a reliable and secure method of obfuscating their digital asset transactions.

In this article, we will explore the concept of Tornado Cash, its unique features, and its implications for privacy-conscious individuals in the cryptocurrency space. Let's dive into the world of Tornado Cash and unlock the potential of decentralized privacy.

Key Takeaways

- Tornado Cash is a decentralized privacy solution for cryptocurrency transactions.

- It offers trustless and non-custodial privacy through the use of smart contracts and anonymity pools.

- Tornado Cash provides financial privacy, protects against surveillance and tracking, and enhances the fungibility of cryptocurrencies.

- Users can access the Tornado Cash interface, deposit and withdraw funds, and should be aware of gas fees and transaction confirmation times.

- Regulatory considerations, such as OFAC compliance, and diversifying privacy options are crucial when using Tornado Cash.

- The Tornado Cash ecosystem includes the TORN token, support on various blockchains, and integration partnerships.

Introducing Tornado Cash: Understanding the Need for Privacy in Cryptocurrency Transactions

Tornado Cash addresses the growing demand for financial privacy in the cryptocurrency space. It allows users to obfuscate their transaction history and retain their anonymity while engaging in digital asset transfers. Privacy-focused tools like Tornado Cash raise concerns about money laundering risks, requiring enhanced due diligence (EDD) for users.

How Tornado Cash Works: Unveiling the Decentralized Privacy Protocol

- Trustless and Non-custodial Nature: Tornado Cash operates in a trustless and non-custodial manner, ensuring that users retain full control of their funds throughout the process.

- The Role of Smart Contracts: Tornado Cash utilizes smart contracts, particularly zero-knowledge proofs, to achieve privacy without requiring users to disclose sensitive information.

- The Anonymity Pool Concept: Tornado Cash pools users' funds together, making it difficult to trace individual transactions, thereby preserving privacy.

Benefits of Tornado Cash: Exploring the Advantages of Decentralized Privacy

- Preserving Financial Privacy: Tornado Cash allows users to shield their transaction history, protecting their financial privacy from prying eyes.

- Protecting against Surveillance and Tracking: By obfuscating transaction trails, Tornado Cash helps users mitigate the risk of surveillance and tracking by third parties.

- Ensuring Fungibility of Cryptocurrencies: Tornado Cash enhances the fungibility of cryptocurrencies by making individual tokens indistinguishable from one another, ensuring they are equally interchangeable.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

Tornado Cash in Action: Navigating the Process of Privacy-enhanced Transactions

- Accessing the Tornado Cash Interface: Users can access the Tornado Cash interface through supported wallets and connect to compatible networks.

- Depositing and Withdrawing Funds: The process involves depositing funds into the anonymity pool and later withdrawing them while maintaining privacy.

- Understanding Gas Fees and Transaction Confirmation Times: Users should be aware of gas fees associated with their transactions and the time required for confirmation on the blockchain network.

Tornado Cash and Regulatory Considerations: OFAC Compliance and Alternatives

- OFAC Compliance and Mitigating Risks: Users must be mindful of regulatory compliance and potential risks associated with using Tornado Cash, particularly regarding Office of Foreign Assets Control (OFAC) requirements.

- Exploring Alternatives and Diversifying Privacy Options: Users may consider diversifying their privacy-enhancing strategies by exploring alternative privacy solutions and combining different protocols.

Tornado Cash and Its Ecosystem: Insights into the Tornado Cash Coin

- The Role of TORN Tokens: TORN is the native governance token of Tornado Cash, allowing holders to participate in the protocol's decision-making process.

- Tornado Cash on Different Blockchains: Tornado Cash operates on multiple blockchains, providing users with flexibility and options for their privacy needs.

- Tornado Cash Integrations and Partnerships: The protocol actively seeks integrations and partnerships to expand its reach and offer enhanced privacy features to a wider user base.

Coupon Fraud

Introduction

Coupons have long been a popular method for consumers to save money on their purchases. However, where there are opportunities for savings, there are also those who seek to exploit them. Coupon fraud is a deceptive practice that undermines the integrity of the couponing system and poses significant challenges for retailers, manufacturers, and consumers alike.

In this article, we delve into the world of coupon fraud, examining its various forms, the consequences it entails, and the measures taken to combat this illicit activity.

Key Takeaways

- Coupon fraud affects manufacturers, retailers, and consumers alike. It leads to financial losses for businesses and erodes consumer trust in the couponing system.

- Coupon fraud can take multiple forms, including counterfeiting coupons, altering valid coupons, and using coupons on products for which they are not intended (known as coupon glittering).

- Engaging in coupon fraud is illegal and can result in fines, imprisonment, and a criminal record. The severity of the punishment varies depending on the jurisdiction and the scale of the fraud.

- To combat coupon fraud, manufacturers are continually enhancing security features on coupons, such as unique barcodes, holograms, and watermarks.

- Retailers and consumers play a crucial role in combating coupon fraud. Retailers are implementing point-of-sale systems that can detect fraudulent coupons, while consumers are encouraged to verify the authenticity of coupons and understand their terms and conditions.

Understanding Coupon Fraud

Coupon fraud encompasses a range of deceptive practices aimed at obtaining discounts or benefits that individuals are not entitled to. It can involve counterfeiting coupons, altering valid coupons, using expired coupons, or misrepresenting product purchase requirements. Fraudsters employ various techniques to manipulate the couponing system, costing manufacturers and retailers millions of dollars each year.

Examples of Coupon Fraud

- Counterfeiting Coupons: Fraudsters create fake coupons that resemble legitimate ones, often using advanced graphic design software. These counterfeit coupons can be distributed online or through illicit channels, deceiving both retailers and consumers.

- Coupon Glittering: Also known as "code stripping," this form of fraud involves using coupons on products for which they are not intended. By exploiting coding loopholes in the coupon system, fraudsters can use coupons on items other than those specified, leading to improper discounts.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

The Impacts of Coupon Fraud

Coupon fraud has far-reaching consequences for all parties involved. Let's explore some of the key impacts:

- Financial Losses: Coupon fraud costs manufacturers and retailers substantial financial losses. Fraudulent redemptions drain revenue, disrupt inventory management, and erode profitability.

- Consumer Trust: Coupon fraud erodes consumer trust in the couponing system. When individuals encounter fake or invalid coupons, it diminishes their confidence in the effectiveness and fairness of legitimate coupons.

Legal Implications of Coupon Fraud

Coupon fraud is not only unethical but also illegal. Engaging in coupon fraud can result in serious legal consequences, including fines, imprisonment, and criminal records. While the severity of the punishment may vary depending on the jurisdiction and the scale of the fraud, it is essential to understand that coupon fraud is a punishable offence.

Notorious Coupon Fraud Cases

One notable coupon fraud case is that of Lori Ann Talens, who masterminded a large-scale counterfeit coupon operation. Talens created fake coupons and sold them online, resulting in significant financial losses for manufacturers. Her case highlighted the impact of coupon fraud and the need for robust measures to combat such criminal activities.

Combating Coupon Fraud

Coupon fraud is a pervasive issue that requires the collective effort of manufacturers, retailers, and consumers to combat it effectively. Here are some measures taken to address coupon fraud:

Advanced Coupon Security Features

Manufacturers continually enhance coupon security features, making them harder to counterfeit or misuse. These may include unique barcodes, holograms, watermarks, or embedded security threads.

Retailer Vigilance

Retailers play a crucial role in combating coupon fraud by training their employees to recognize counterfeit or altered coupons. Additionally, implementing point-of-sale systems that can detect fraudulent coupons helps prevent their redemption.

{{cta('bdd96089-cde2-43f3-95a3-3f6d7b74af38','justifycenter')}}

Conclusion

Coupon fraud is a detrimental practice that undermines the integrity of the couponing system, causing financial losses to manufacturers and eroding consumer trust. The consequences of engaging in coupon fraud can be severe, both legally and reputationally. It is crucial for individuals to understand the ethical and legal implications associated with coupon fraud and support efforts to combat this illicit activity. By promoting awareness, implementing robust security measures, and fostering a culture of integrity, we can preserve the effectiveness and fairness of the couponing system. Manufacturers, retailers, and consumers must work together to combat coupon fraud and uphold the integrity of the couponing process.

While coupon fraud poses significant challenges, there are measures in place to address and mitigate this issue. Manufacturers are constantly improving the security features of coupons, making them more difficult to counterfeit or misuse. Unique barcodes, holograms, watermarks, and embedded security threads are just some of the advancements in coupon security.

Retailers also play a vital role in the fight against coupon fraud. They train their employees to identify counterfeit or altered coupons and implement point-of-sale systems that can detect fraudulent coupons. By maintaining vigilance and staying informed about emerging fraudulent tactics, retailers can prevent the redemption of fake coupons and protect their business.

For consumers, it is essential to be vigilant and cautious when using coupons. Verify the authenticity of coupons before use, ensuring they are obtained from reputable sources. Familiarize yourself with the terms and conditions of coupons to avoid unintentional misuse. By practicing responsible couponing, consumers can help prevent the perpetuation of coupon fraud.

In conclusion, coupon fraud is a deceptive practice that undermines the integrity of the couponing system. It leads to financial losses for manufacturers, erodes consumer trust, and carries legal implications. Through collaborative efforts between manufacturers, retailers, and consumers, we can combat coupon fraud and maintain the effectiveness and fairness of the couponing process. By promoting awareness, implementing robust security measures, and exercising responsible couponing practices, we can protect the integrity of the couponing system and ensure its benefits for all stakeholders involved.

Frequently Asked Questions

What is Coupon Fraud?

Coupon fraud involves deceptive practices aimed at obtaining unauthorized discounts or benefits. This can include counterfeiting coupons, altering valid coupons, or using expired coupons.

What are Some Examples of Coupon Fraud?

Examples include counterfeiting coupons, altering the terms on valid coupons, and "coupon glittering," which involves using coupons on products for which they are not intended.

What are the Financial Impacts of Coupon Fraud?

Coupon fraud leads to significant financial losses for manufacturers and retailers. It disrupts inventory management and can erode profitability.

What are the Legal Implications of Coupon Fraud?

Coupon fraud is illegal and can result in fines, imprisonment, and a criminal record. The severity of the punishment can vary depending on the jurisdiction and the scale of the fraud.

How Can Coupon Fraud be Prevented?

Prevention measures include advanced security features on coupons, retailer vigilance in identifying fraudulent coupons, and consumer awareness about the terms and conditions of coupon use.

FedRAMP

Introduction

As government agencies increasingly embrace cloud computing, ensuring the security and integrity of sensitive data becomes paramount. The Federal Risk and Authorization Management Program (FedRAMP) has emerged as a crucial framework for evaluating and authorizing cloud service providers (CSPs) to ensure they meet rigorous security standards.

In this article, we will delve into the world of FedRAMP, understand its compliance requirements, explore the certification process, and examine the key controls that CSPs must adhere to. Let's explore the vital aspects of FedRAMP and its significance in safeguarding sensitive government data. In the realm of cloud security, compliance with FedRAMP standards is crucial to avoid operational risk and potential breaches.

Key Takeaways

- FedRAMP sets rigorous security standards for cloud service providers seeking authorization to handle federal data.

- Compliance with FedRAMP controls, mapping to NIST 800-53, and continuous monitoring are essential requirements.

- The certification process involves documentation, engagement with a 3PAO, and submission of the authorization package.

- The approved list and FedRAMP Marketplace showcase authorized CSPs for government agencies.

- FedRAMP compliance offers enhanced security, cost reduction, efficiency gains, and expanded business opportunities.

Introducing FedRAMP: Defining Compliance for Cloud Service Providers

FedRAMP is a government-wide program that standardizes the security assessment, authorization, and continuous monitoring of cloud services. Its objective is to provide a consistent and risk-based approach to ensure the security and privacy of federal data stored and processed in cloud environments.

Understanding FedRAMP Compliance: Key Requirements and Guidelines

- FedRAMP Controls Framework: The FedRAMP controls framework outlines the security controls that CSPs must implement and document in their systems. These controls align with the National Institute of Standards and Technology (NIST) Special Publication 800-53.

- Mapping Security Controls to NIST 800-53: CSPs must demonstrate how they meet the security control requirements outlined in NIST 800-53, which covers various security domains such as access control, incident response, and system integrity.

- Continuous Monitoring and Assessment: FedRAMP requires CSPs to implement continuous monitoring practices to ensure ongoing compliance with security requirements. Regular assessments, audits, and reporting are essential elements of this process.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

The FedRAMP Certification Process: Navigating the Authorization Journey

- Documentation and System Security Plan (SSP): CSPs are required to create a System Security Plan (SSP) that documents their security controls, processes, and procedures. This plan serves as the foundation for the certification process.

- Third-Party Assessment Organization (3PAO) Engagement: CSPs engage with a FedRAMP-accredited 3PAO to conduct an independent assessment of their systems and security controls. The 3PAO evaluates the implementation of security controls and provides an assessment report.

- FedRAMP Authorization Package Submission: CSPs compile the necessary documentation, including the SSP, assessment report, and other supporting materials, and submit the FedRAMP authorization package for review by the Joint Authorization Board (JAB) or an agency-specific authorizing official.

The Approved List and the FedRAMP Marketplace: Showcasing Trusted Cloud Service Providers

The FedRAMP Program Management Office maintains an approved list of cloud service offerings that have successfully achieved FedRAMP compliance. This list serves as a resource for government agencies to identify and select trusted CSPs. Additionally, the FedRAMP Marketplace provides a platform for CSPs to showcase their authorized offerings.

FedRAMP in Action: Realizing the Benefits of Compliance

- Enhanced Security and Risk Management: FedRAMP compliance ensures robust security measures, risk management practices, and continuous monitoring, reducing the risk of data breaches and unauthorized access.

- Cost Reduction and Efficiency Gains: FedRAMP streamlines the authorization process, allowing CSPs to reuse security assessment artifacts across multiple agencies, reducing duplication efforts and costs.

- Expansion of Business Opportunities: Achieving FedRAMP compliance opens doors to lucrative opportunities in the government sector, as agencies prioritize authorized CSPs for their cloud computing needs.

Frequently Asked Questions

What is FedRAMP and what is its purpose?

FedRAMP is a government-wide program that standardizes the security assessment, authorization, and continuous monitoring of cloud services for the protection of federal data stored and processed in the cloud.

What are the key requirements and guidelines for FedRAMP compliance?

The FedRAMP controls framework outlines the security controls that Cloud Service Providers (CSPs) must implement, which align with the NIST 800-53 standards.

How does the FedRAMP certification process work?

The FedRAMP certification process involves creating a System Security Plan (SSP), engaging with a FedRAMP-accredited third-party assessment organization (3PAO) for an independent assessment, and submitting the authorization package for review.

What is the significance of the approved list and the FedRAMP Marketplace?

The approved list maintained by the FedRAMP Program Management Office helps government agencies identify and select trusted CSPs, while the FedRAMP Marketplace allows CSPs to showcase their authorized offerings.

What are the benefits of achieving FedRAMP compliance?

FedRAMP compliance ensures enhanced security and risk management, cost reduction through streamlined authorization processes, and increased business opportunities in the government sector.

Wire Fraud

Introduction

Wire fraud has become a prevalent form of cybercrime that poses significant risks to individuals, businesses, and financial institutions. Perpetrators of wire fraud employ various deceptive tactics to manipulate victims into wiring funds or providing sensitive information for illicit purposes.

In this article, we will delve into the realm of wire fraud, understand its implications, explore the legal framework surrounding it, and discuss proactive measures to prevent and report such fraudulent activities. Robust wire fraud prevention measures include identity verification, phishing awareness, and suspicious activity reporting.

Key Takeaways

- Wire fraud involves deceptive tactics to manipulate victims into wiring funds or providing sensitive information.

- Wire fraud is a felony offence, punishable by fines and imprisonment.

- Law enforcement agencies such as the FBI, U.S. Secret Service, and FinCEN play a crucial role in investigating wire fraud.

- Protect yourself from wire fraud by strengthening cybersecurity practices, recognizing common red flags, and educating yourself and your employees.

- Report instances of wire fraud to the FBI through the IC3 platform and coordinate with your financial institution.

Understanding Wire Fraud: Unveiling the Threat Landscape

Wire fraud involves the use of electronic communications or wire transfers to deceive victims into providing money, sensitive information, or other valuable assets to fraudulent entities. Perpetrators often employ social engineering techniques, phishing emails, or compromised communication channels to manipulate victims.

The Legal Landscape: Wire Fraud and its Consequences

- Wire Fraud as a Felony: Wire fraud is a federal crime in the United States and is classified as a felony. It carries severe penalties, including fines and imprisonment, depending on the nature and scale of the fraudulent activity.

- Wire Fraud Statute and Prosecution: The wire fraud statute is encompassed within Title 18, Section 1343 of the United States Code. It provides the legal framework for prosecuting individuals engaged in wire fraud.

- Punishment for Wire Fraud: The punishment for wire fraud varies depending on several factors, such as the amount of money involved, the level of sophistication, and the impact on victims. Convicted individuals may face substantial fines and imprisonment, often exceeding several years.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

Investigating Wire Fraud: The Role of Law Enforcement Agencies

- Federal Bureau of Investigation (FBI): The FBI is a primary federal law enforcement agency responsible for investigating and combating various cybercrimes, including wire fraud. They collaborate with other agencies and coordinate efforts to apprehend and prosecute fraudsters.

- U.S. Secret Service: While primarily known for protecting high-ranking officials, the U.S. Secret Service also investigates financial crimes, including wire fraud. They focus on cases involving counterfeit currency, financial institution fraud, and computer crimes.

- Financial Crimes Enforcement Network (FinCEN): FinCEN is a bureau of the U.S. Department of the Treasury that collects and analyzes financial transaction data to combat money laundering, terrorist financing, and other financial crimes. They work in conjunction with other agencies to identify patterns and track illicit funds.

Read More: Understanding Social Security Fraud and Its Impact on Society

Protecting Yourself from Wire Fraud: Proactive Measures

- Strengthening Cybersecurity Practices: Implement robust cybersecurity measures, including multi-factor authentication, encryption, and regular software updates. Conduct regular employee training on recognizing and preventing wire fraud.

- Recognizing Common Red Flags: Be vigilant for warning signs of wire fraud, such as unsolicited requests for money or personal information, suspicious email addresses or phone numbers, and urgent requests for immediate wire transfers.

- Educating Yourself and Employees: Stay informed about the latest techniques used in wire fraud and educate yourself and your employees about potential threats. Encourage a culture of cybersecurity awareness and promote a proactive approach to fraud prevention.

{{cta('c2265f53-7251-4b3c-91d7-20ef8707a8f3','justifycenter')}}

Reporting Wire Fraud: Taking Action Against Fraudsters

- Reporting to the FBI: If you fall victim to wire fraud, report the incident to the FBI through their Internet Crime Complaint Center (IC3) website. Provide all relevant details and evidence to aid in their investigation.

- Utilizing the Internet Crime Complaint Center (IC3): The IC3 is a partnership between the FBI, the National White Collar Crime Center (NW3C), and the Bureau of Justice Assistance (BJA). It serves as a central hub for reporting cybercrimes, including wire fraud.

- Coordinating with Financial Institutions: Notify your financial institution immediately if you suspect wire fraud. They can assist in freezing accounts, recovering funds if possible, and launching their internal investigations.

Read More: Cyber Fraud: Real-Life Examples and Prevention Strategies

Impersonation

Introduction

In today's digital age, where online interactions are increasingly common, the risk of impersonation has become a pressing concern. Impersonation refers to the act of pretending to be someone else with the intent to deceive or defraud others. Whether it's assuming another person's identity online or imitating a public figure, impersonation can have serious consequences for individuals and society as a whole.

This article delves into the world of impersonation, shedding light on its examples, the full meaning behind it, the act of impersonating, and the distinction between impersonation and impersonating. By understanding the intricacies of impersonation, we can better protect ourselves and navigate the digital landscape with vigilance.

Key Takeaways

- Impersonation involves intentionally assuming another person's identity with the intent to deceive, defraud, or harm others, often exploiting various mediums like social media, email, or phone calls.

- Impersonation can manifest in various forms, such as online identity theft, phishing scams, caller ID spoofing, and impersonating public figures. Techniques used by impersonators can range from social engineering to identity theft and spoofing.

- Impersonation poses significant risks, including financial loss, reputation damage, identity theft, and emotional distress. Legal consequences can include criminal charges, civil lawsuits, and actions by online platforms.

- While both terms are often used interchangeably, "impersonation" refers to the overarching concept, and "impersonating" focuses on the specific actions or behaviors involved in assuming another's identity.

- Individuals can protect themselves by strengthening online security, adjusting privacy settings, and verifying identities. Reporting impersonation incidents to law enforcement and online platforms is crucial for taking appropriate action.

What is Impersonation?

Impersonation involves assuming another person's identity or pretending to be someone you're not. It is an intentional act carried out with the motive to deceive, defraud, or harm others. Impersonators often utilize various mediums, such as social media platforms, email, or phone calls, to engage with their targets and manipulate them for personal gain. By adopting another person's identity, they aim to exploit trust, gain access to sensitive information, or carry out fraudulent activities.

The Meaning of Impersonation

The term "impersonation" refers to the act of assuming or mimicking the identity of another individual or entity. It involves deliberately portraying oneself as someone else, often with the intention to deceive, mislead, or manipulate others. Impersonation can occur in various contexts, both online and offline, and is driven by different motivations, ranging from financial gain to personal gratification or even malicious intent.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

Examples of Impersonation

Impersonation can take many forms, and its examples are diverse. Some common instances of impersonation include:

- Online Identity Theft: Impersonating someone on social media or creating fake profiles to deceive others.

- Phishing Scams: Sending fraudulent emails or messages pretending to be a trusted entity to extract personal information.

- Caller ID Spoofing: Manipulating caller identification to make it appear as if the call is coming from a different person or organization.

- Impersonating Public Figures: Pretending to be a well-known personality, such as a celebrity or public official, to gain attention or spread false information.

- Business Impersonation: Presenting oneself as an employee or representative of a legitimate company to deceive customers or partners.

The Act of Impersonating: Delving Deeper

To understand the act of impersonating, it is essential to explore its underlying aspects. Impersonating involves more than just imitating someone's physical appearance or mannerisms. It requires a comprehensive understanding of the individual being impersonated, including their behaviours, communication style, and personal information.

Impersonators often invest time and effort in studying their targets to convincingly assume their identity. They may gather information from public sources, social media profiles, or even engage in social engineering tactics to gain access to sensitive details. The act of impersonating goes beyond mere imitation and involves a level of deception that can be highly sophisticated.

Impersonators may employ various techniques to enhance their impersonation, such as:

- Social Engineering: Manipulating individuals or situations to extract personal information or gain trust.

- Identity Theft: Stealing personal data, such as social security numbers or login credentials, to assume someone's identity.

- Spoofing: Falsifying digital footprints, such as IP addresses or email headers, to appear as someone else.

- Psychological Manipulation: Exploiting emotions, vulnerabilities, or relationships to deceive or control others.

By understanding the intricacies of the act of impersonating, individuals can be more vigilant and better equipped to identify and prevent potential impersonation attempts.

Impersonation vs. Impersonating: Understanding the Difference

While the terms "impersonation" and "impersonating" are often used interchangeably, there is a subtle distinction between the two. Impersonation refers to the overarching concept of assuming another person's identity, while impersonating focuses on the specific action or behavior of pretending to be someone else.

Impersonation can involve various activities, including creating fake profiles, assuming a false identity, or deceiving others by imitating someone's characteristics or traits. On the other hand, impersonating refers to the active engagement in the act of assuming another person's identity, whether online or in person, with the intent to deceive or defraud others.

Understanding this distinction is important as it helps us navigate discussions surrounding impersonation and enables clearer communication when addressing specific aspects of the practice.

The Risks of Impersonation

Impersonation poses significant risks to individuals, organizations, and society as a whole. Some key risks associated with impersonation include:

- Financial Loss: Impersonators may use stolen identities to carry out fraudulent financial transactions, leading to substantial monetary losses for victims.

- Reputation Damage: By impersonating someone, malicious actors can tarnish their target's reputation by engaging in illegal or unethical activities under their name.

- Identity Theft: Impersonation can result in the theft of personal information, which can be used for identity theft or further fraudulent activities.

- Privacy Invasion: Impersonators may intrude upon an individual's privacy by accessing their personal accounts, private messages, or confidential information.

- Emotional Distress: Being impersonated can cause significant emotional distress, including feelings of violation, betrayal, or powerlessness.

These risks highlight the importance of proactive measures to detect and prevent impersonation attempts, protecting individuals and organizations from potential harm.

Consequences of Impersonation

The consequences of impersonation can be severe, both legally and personally. Depending on the jurisdiction and the nature of the impersonation, the following consequences may apply:

- Legal Ramifications: Impersonation is considered a criminal offense in many jurisdictions, and perpetrators can face criminal charges, fines, and imprisonment if convicted.

- Civil Lawsuits: Impersonation victims may choose to pursue civil litigation to seek compensation for financial losses, damages to their reputation, or emotional distress.

- Online Platform Actions: Social media platforms, online marketplaces, and other digital platforms often have policies in place to address impersonation. Impersonators can face account suspension, content removal, or permanent bans from these platforms.

- Damage to Relationships: Impersonation can lead to strained relationships, trust issues, and the erosion of personal and professional connections. Victims may experience a breakdown in trust with friends, family, or colleagues who were deceived by the impersonation.

- Reputational Damage: Impersonation can have long-lasting effects on a person's reputation. The actions carried out by impersonators, especially if they involve illegal or unethical behaviour, can stain the reputation of the individual being impersonated. Rebuilding trust and repairing a damaged reputation can be a challenging and time-consuming process.

Protecting Yourself from Impersonation

While it may not be possible to completely eliminate the risk of impersonation, there are several measures individuals can take to protect themselves:

- Strengthen Online Security: Use strong, unique passwords for all online accounts and enable two-factor authentication when available. Regularly update software and be cautious of phishing attempts.

- Privacy Settings: Adjust privacy settings on social media platforms to restrict access to personal information and posts. Be mindful of the information shared publicly, as it can be used by impersonators for their advantage.

- Verify Identity: Be cautious when interacting with individuals or organizations online. Verify the identity of unknown contacts through independent channels or official websites before sharing personal information or engaging in financial transactions.

- Educate Yourself: Stay informed about the latest impersonation techniques and scams. Be skeptical of suspicious requests for personal information or financial transactions, especially from unfamiliar sources.

{{cta('c2265f53-7251-4b3c-91d7-20ef8707a8f3','justifycenter')}}

Reporting Impersonation Incidents

If you believe you have been a victim of impersonation or have come across an impersonation attempt, it is essential to report the incident to the relevant authorities or platforms:

- Law Enforcement: Contact your local law enforcement agency and provide them with detailed information about the impersonation incident. They can guide you on further steps to take and investigate the matter.

- Online Platforms: If the impersonation occurred on a social media platform, online marketplace, or other digital platform, report the incident to the platform's support or abuse team. They can take appropriate action, such as suspending the impersonator's account or removing malicious content.

Legal Implications of Impersonation

Impersonation can have significant legal consequences, as it is considered a form of fraud and deception. The exact legal implications may vary depending on the jurisdiction, but some common legal considerations related to impersonation include:

- Criminal Charges: Impersonation can result in criminal charges, such as identity theft, fraud, or false impersonation. Penalties may include fines, probation, or imprisonment, depending on the severity of the offense.

- Civil Lawsuits: Impersonation victims may choose to pursue civil litigation against the impersonator to seek compensation for damages, financial losses, or emotional distress. Successful lawsuits can result in monetary judgments or court-ordered injunctions against the impersonator.

Conclusion

Impersonation is a deceptive practice with serious consequences for individuals and society. By understanding the risks, examples, and implications of impersonation, individuals can take proactive steps to protect themselves and mitigate the potential damage caused by impersonators. It is crucial to remain vigilant, practice good online security habits, and report any suspected impersonation incidents to the appropriate authorities or platforms. By staying informed and proactive, we can navigate the digital landscape with greater confidence and protect ourselves from the threats of impersonation.

Frequently Asked Questions

What is Impersonation?

Impersonation is the act of intentionally assuming another person's identity to deceive, defraud, or harm others.

How Does Impersonation Differ from Impersonating?

"Impersonation" refers to the general concept of assuming another's identity, while "impersonating" focuses on the specific actions or behaviors involved in doing so.

What are Some Common Types of Impersonation?

Common types include online identity theft, phishing scams, caller ID spoofing, impersonating public figures, and business impersonation.

What Risks are Associated with Impersonation?

Risks include financial loss, reputation damage, identity theft, invasion of privacy, and emotional distress.

How Can One Protect Themselves from Impersonation?

Protective measures include using strong, unique passwords, enabling two-factor authentication, adjusting social media privacy settings, and verifying the identity of people or organizations before sharing personal information.

Fraudster

Introduction

In an interconnected world driven by technology and online interactions, the presence of fraudsters and scammers poses a significant threat to individuals and organizations alike. These cunning individuals employ various tactics to deceive and manipulate their targets for personal gain. Understanding the modus operandi of fraudsters is crucial in safeguarding ourselves and our communities against their deceptive schemes.

In this article, we will explore the world of fraudsters, shed light on their typical characteristics, explore the meaning of acting fraudulently, and uncover how they exploit social media platforms to steal valuable information. By being aware of their strategies and taking proactive measures, we can effectively protect ourselves from falling victim to their fraudulent acts.

Key Takeaways

- Fraudsters engage in deceptive practices with the intention of deceiving others for personal gain.

- Fraudsters employ various tactics such as impersonation, scamming, and fraudulent actions to exploit individuals and gain financial or personal information.

- Social media platforms have become popular avenues for fraudsters to target victims due to their wide user base and ease of communication.

- Common scams perpetrated by fraudsters on social media include phishing, romance scams, and identity theft.

- To protect yourself from fraudsters on social media, it is important to exercise caution, verify profiles and websites, and avoid sharing personal information with unknown individuals.

- Strong passwords, two-factor authentication, and regular privacy settings review are essential for enhancing online security.

Who is a Fraudster?

Typical Characteristics

Fraudsters exhibit certain common traits and behaviors that enable them to carry out their deceptive activities. These individuals are often highly manipulative and skilled at gaining the trust of their targets. They are opportunistic and exploit vulnerabilities for personal gain. Fraudsters can be charming and persuasive, adept at disguising their true intentions behind a façade of legitimacy. They may display a lack of empathy and have a propensity for taking advantage of others for financial or personal gain.

Synonyms for Scammer

When discussing individuals engaged in fraudulent activities, various terms are used to describe them. A scammer is one such synonym commonly used to refer to fraudsters. Scammers are individuals who use deceit and trickery to defraud others, often through schemes that appear legitimate but are designed to extract money or valuable information. These individuals exploit the trust of their victims and employ tactics such as phishing, identity theft, or fake investment schemes to carry out their fraudulent activities.

{{cta('4129950d-ed17-432f-97ed-5cc211f91c7d','justifycenter')}}

Understanding Fraudulent Actions

Defining Fraudulently

Acting fraudulently refers to engaging in deceptive practices with the intention of deceiving others for personal gain. It involves intentionally misrepresenting information or manipulating circumstances to exploit unsuspecting victims. Fraudulent actions can take various forms, such as financial fraud, insurance fraud, or online scams. These actions can have severe consequences, including financial loss, damage to reputations, and emotional distress for the victims.

The Impact of Fraud

Fraudulent actions have far-reaching implications for both individuals and society as a whole. Victims of fraud may experience significant financial losses, leading to financial instability and stress. The aftermath of fraud can also result in emotional distress, mistrust, and a sense of violation. Furthermore, fraudulent activities undermine the integrity of financial systems and erode public trust in institutions. They contribute to increased costs for businesses, governments, and individuals, as efforts are made to combat and prevent fraud.

Infamous Fraudsters in History

Notorious Fraudsters

Throughout history, there have been notable cases involving infamous fraudsters who have gained notoriety for their elaborate schemes. These individuals have orchestrated large-scale frauds, often targeting financial institutions or investors. Examples include figures like Bernie Madoff, who orchestrated one of the largest Ponzi schemes in history, and Charles Ponzi himself, who gave rise to the term "Ponzi scheme." These cases serve as reminders of the significant impact fraudsters can have on individuals and the financial system.

Alleged Fraudsters

The term "alleged fraudster" refers to individuals who have been accused of engaging in fraudulent activities but have not yet been proven guilty in a court of law. Allegations of fraud can be levelled against individuals in various contexts, including corporate fraud, securities fraud, or internet scams. It is important to recognize that until proven guilty, individuals should be considered innocent, and legal processes should be followed to establish their culpability.

Unraveling Social Media Exploitation

Social Media and Fraud

Fraudsters have adapted to the digital age by exploiting social media platforms to carry out their deceitful activities. They leverage the vast reach and interconnectedness of these platforms to target potential victims and gain access to their personal information. Social media provides fraudsters with a means to create fake profiles, initiate phishing attacks, spread malware, or engage in identity theft. They may also use social engineering techniques to manipulate individuals into revealing sensitive information.

Stealing Information

Fraudsters employ various methods to steal valuable information from unsuspecting victims on social media. This can include impersonating trusted individuals or organizations, creating fake accounts or websites, or enticing individuals to click on malicious links or download malicious attachments. By tricking users into sharing personal details, such as login credentials or financial information, fraudsters can gain unauthorized access to accounts or carry out identity theft.

Protecting Yourself

To safeguard against social media exploitation by fraudsters, it is crucial to adopt security measures and exercise caution while using these platforms. Here are some steps to protect yourself:

- Be wary of unsolicited friend requests or messages from unknown individuals.

- Verify the authenticity of profiles and websites before sharing personal information.

- Use strong, unique passwords and enable two-factor authentication for added security.

- Regularly review your privacy settings and limit the amount of personal information visible to the public.

- Avoid clicking on suspicious links or downloading files from untrusted sources.

- Educate yourself about common social media scams and stay updated on the latest fraud techniques.

- Report any suspicious activity or accounts to the platform administrators.

By staying vigilant and taking proactive steps to protect your online presence, you can reduce the risk of falling victim to social media fraud and thwart fraudsters' attempts to exploit your information.