What is PEP Screening? A Complete Guide for Banks and Fintechs

.svg)

In 2016, the Monetary Authority of Singapore revoked the banking licences of Falcon Private Bank and BSI Bank — both in the same year. The proximate cause was their handling of 1MDB-linked funds. At the centre of that scandal stood Najib Razak, then Prime Minister of Malaysia and, by every applicable definition, a politically exposed person.

Here is what made 1MDB so instructive: those banks did not fail to identify Najib Razak as a PEP. His status was not hidden. He was the head of government of a sovereign nation. The failure was what came after identification — no meaningful source of wealth verification, no senior management scrutiny calibrated to the risk, and no ongoing monitoring that could have caught the pattern of transfers as they accumulated. USD 4.5 billion moved through the system. The problem was not that PEP screening did not exist. The problem was that PEP screening stopped at the checkbox.

That distinction between identifying a PEP and actually managing the risk that designation carries, is what this guide covers.

What Is a Politically Exposed Person (PEP)?

FATF Recommendation 12 defines a PEP as a natural person who is or has been entrusted with a prominent public function. That definition is broader than most practitioners assume.

There are three categories:

Domestic PEPs hold senior positions within their own country. Government ministers, senior legislators, senior military officers, executives of state-owned enterprises, and senior judiciary members all qualify. A sitting Malaysian minister is a domestic PEP. A Philippine senator is a domestic PEP. A member of the BSP board is a domestic PEP.

Foreign PEPs hold equivalent positions in another country. An Indonesian government official is a foreign PEP from the perspective of a Singapore bank onboarding them as a client.

International organisation PEPs are senior executives of bodies such as the UN, World Bank, and IMF.

Relatives and Close Associates

This category is where most PEP screening programmes fail quietly. FATF Recommendation 12 explicitly extends the elevated risk designation to relatives and close associates (RCAs) — family members and known business associates of a PEP.

The Indonesian government official's spouse is an RCA. A business partner who shares ownership of a company with a Philippine senator is an RCA. An account held by an RCA, with no direct PEP name on it, carries the same risk elevation as the PEP's own account. A screening programme that only looks at the account holder's name will miss this entirely.

How Long Does PEP Status Last?

FATF does not set a sunset period. A former prime minister who left office last year does not automatically cease to be a PEP risk.

MAS and BNM guidance both indicate a risk-based approach with no automatic de-listing. Many APAC jurisdictions require treating former PEPs as high-risk for at least 12 months after leaving office. In practice, the risk-based approach means continuing EDD until the institution can demonstrate — and document — that the elevated risk has materially diminished.

Why PEPs Are High-Risk: The Regulatory Rationale

PEPs have access to state resources, procurement decisions, and regulatory influence. That access creates both the opportunity and, in environments with weak governance, the structural conditions for corruption-linked money laundering.

The 1MDB case demonstrated this precisely. Najib Razak's position as Prime Minister gave him effective control over a sovereign wealth fund. Funds were extracted through a network of transactions routed through accounts at Falcon Private Bank Singapore, BSI Bank Singapore, and 1MDB-linked accounts at multiple Malaysian banks. The mechanism was not sophisticated in isolation — large transfers between entities with opaque ownership, wire patterns inconsistent with stated business purpose, and inadequate documentation of source of funds. What made it possible was the combination of PEP access and institutional failure to apply the monitoring that FATF Recommendation 12 requires.

MAS revoked Falcon's licence in October 2016. BSI's licence was revoked in May of the same year. Both had processed transactions that, under any functioning ongoing monitoring programme, should have generated alerts long before the funds were moved.

FATF Recommendation 12 requires all FATF member jurisdictions to apply enhanced due diligence to PEPs. Across APAC, every major financial regulator has implemented this through binding instruments: more rigorous identification, source of funds and wealth verification, senior management or board approval, and — critically — ongoing monitoring, not just onboarding review.

The PEP Screening Process: Step by Step

Step 1: Identification at onboarding. Screen the customer's name against PEP databases at account opening. This is the minimum. It is also, for many institutions, where the process ends — which is not compliant.

Step 2: Selecting list sources. No single global PEP register exists. Governments do not publish a unified, machine-readable list of their own officials. Commercial PEP databases — World-Check, Dow Jones Risk & Compliance, ComplyAdvantage, and others — aggregate from public sources: government gazettes, parliament records, regulatory filings, and adverse media. The quality of the database determines the quality of the screening. Not all databases are equal on APAC coverage.

Step 3: Fuzzy and phonetic matching. PEP names in APAC are routinely transliterated from Arabic, Mandarin, Malay, Tagalog, or Bahasa Indonesia into Latin script. "Muhammad" has over 30 common English transliterations documented in screening literature. A system doing exact string matching will miss a match on "Mohamed" when the database entry reads "Muhammad." The minimum standard is fuzzy matching with configurable similarity thresholds — the compliance team sets the sensitivity, trading off false positives against false negatives based on the institution's risk appetite.

Step 4: Alias and AKA coverage. A single PEP entry in a quality commercial database may carry 10 to 30 aliases — formal name, preferred name, name in original script, transliterations, common abbreviations. Screening must cover all aliases, not only the primary entry.

Step 5: RCA screening. The institution must screen known family members and business associates in addition to the PEP themselves. This requires a database that explicitly links RCA relationships to PEP entries, and screening logic that applies that linkage at the match stage.

Step 6: Risk scoring. A binary PEP flag — PEP or not PEP — is not sufficient for a risk-based programme. A senior minister in a country with a Corruption Perceptions Index score in the bottom quartile presents materially different risk than a local government official in a high-CPI jurisdiction. Screening output should produce a risk score based on the PEP's role, the jurisdiction's CPI, and the nature of the relationship (direct PEP or RCA) — not just a match indicator.

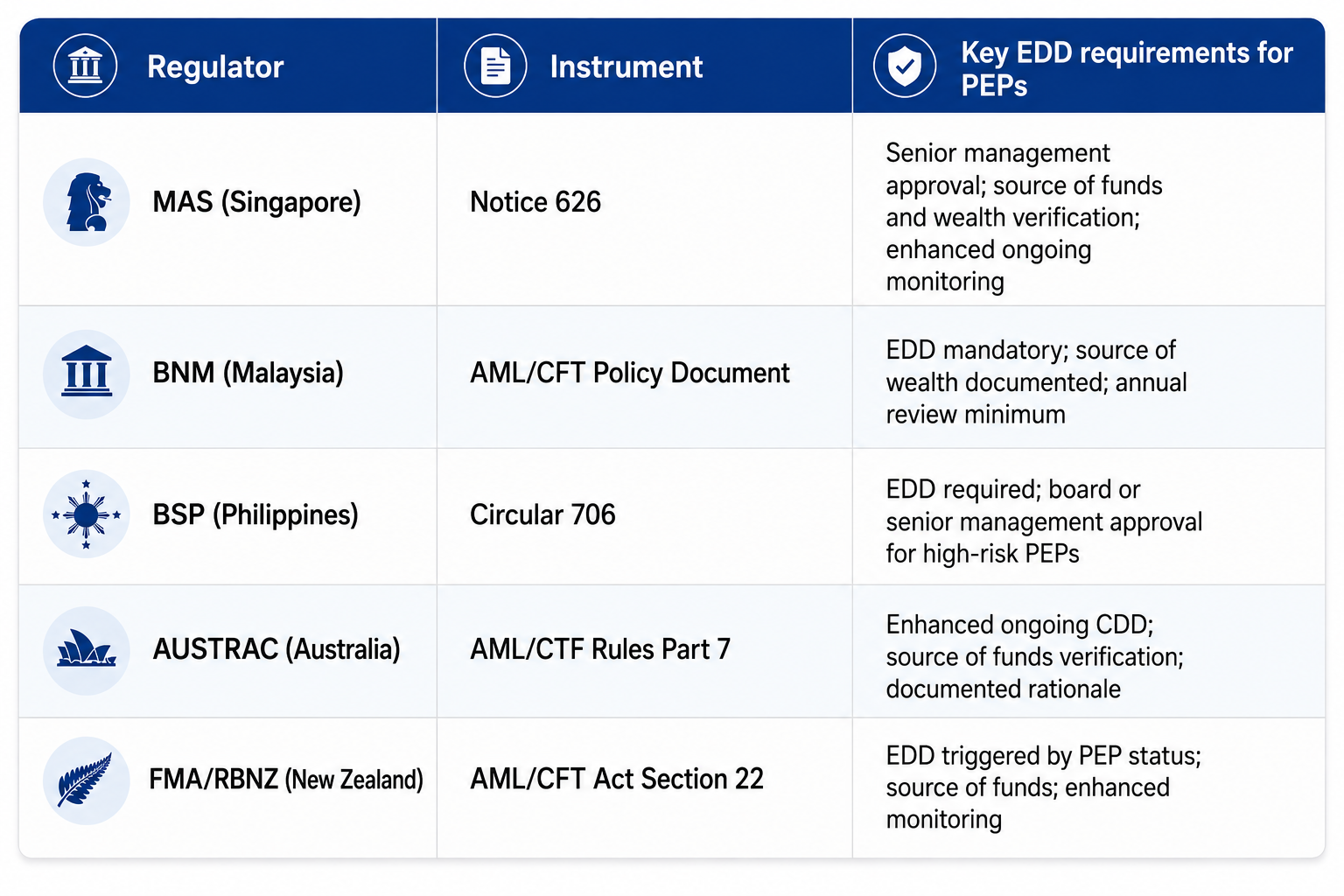

Enhanced Due Diligence for PEPs: What Regulators Require

The table below summarises EDD requirements for PEPs across the five APAC jurisdictions where Tookitaki clients operate most frequently.

The common thread across all five: source of funds and wealth documentation, senior management or board approval, and enhanced ongoing monitoring. Not just enhanced onboarding. The onboarding review and the ongoing monitoring obligation are distinct requirements, and both are mandatory.

For institutions operating in the Philippines specifically, BSP Circular 706 sits alongside the country's AMLA framework. The sanctions screening obligations in the Philippines carry their own separate requirements that must be addressed in parallel with PEP screening — the two programmes are related but not interchangeable.

Ongoing Monitoring of PEPs: Where Most Programmes Break Down

PEP status is not static. A politician loses office. A state enterprise executive is newly appointed to a board. A businessman is awarded a government contract, making him an RCA of a minister. A company linked to a PEP is nationalised. Every one of those events changes the risk profile of an account, sometimes immediately.

The ongoing monitoring obligation means the institution must catch those changes — not only at annual review, but as close to real-time as the database update frequency permits.

List update frequency matters. Commercial PEP databases update continuously, adding new entries and modifying existing ones as source information changes. A batch re-screening process running on a 30-day cycle will miss PEP status changes that occurred in the intervening period. The institution that processes a transaction for a newly appointed government minister in week two of the month, having last screened at the start of the month, has a gap it cannot explain to an examiner.

Transaction monitoring is the second layer. PEP account status should be an input into the transaction monitoring system, not a separate silo. PEP accounts need calibrated scenarios — elevated sensitivity thresholds for large cash transactions, unusual international wire patterns, structuring activity. Identifying a customer as a PEP at onboarding, then running standard monitoring scenarios against their account, defeats much of the purpose of the classification. For an overview of how transaction monitoring and customer risk profiles interact, see our complete guide to transaction monitoring.

Adverse media screening is mandatory, not optional. MAS and BNM guidance both require ongoing adverse media monitoring as a component of the EDD programme for PEPs. News coverage linking a PEP to corruption allegations, enforcement action, or financial crime investigations is material information that changes the risk assessment — and must be picked up between formal review cycles, not only when the annual review is triggered.

Common Failures in PEP Screening Programmes

Six patterns appear consistently in examiner findings and enforcement actions across APAC.

Screening only at onboarding. The institution ran the check when the account was opened. Nobody re-screened when the PEP database was updated, when the customer's circumstances changed, or at any subsequent interval. This is the most common finding.

No RCA screening. The PEP's spouse holds an account. The PEP's business partner is a beneficial owner of a corporate client. Neither was linked to the PEP entry in the screening logic. The RCA relationship was not in the database configuration or was not applied consistently.

Binary flag without risk scoring. Every PEP received the same treatment — a flag, a notation, and no differentiated response based on role, jurisdiction, or exposure level. A senior minister in a country rated 20 on the CPI was processed the same way as a retired local councillor from a G7 country.

Manual re-screening processes. Someone downloaded the updated database, manually ran names against it, and filed the results in a spreadsheet. At scale, this cannot keep pace with the update frequency of commercial databases and creates an audit trail that examiners will question.

No audit trail. Examiners want to see that every customer was screened, when the screening occurred, against which version of the database, what matches were returned, and what the analyst's disposition decision was for each match. Institutions that cannot produce this log face significant difficulties in examination.

Treating identification as the endpoint. The purpose of identifying a PEP is not to decide whether to accept or reject the relationship — although that is one possible outcome. The purpose is to apply EDD and ongoing monitoring calibrated to the risk. Refusing a relationship without applying the EDD process, or accepting it without doing so, both represent programme failures.

Technology Requirements for Effective PEP Screening

A manual or partially manual PEP screening programme cannot meet the operational requirements of FATF Recommendation 12 at scale. The technology stack must address each component of the process.

Automated database ingestion. The system pulls updated PEP data directly from commercial database providers. No manual upload, no batch delay beyond what the provider's feed supports.

Fuzzy and phonetic matching with configurable thresholds. The compliance team sets the similarity threshold — not a fixed value baked into the system by the vendor. Institutions serving APAC clients need matching logic calibrated for Southeast Asian name transliterations, which present different challenges than Western name matching.

RCA relationship mapping. The match logic applies RCA linkages from the database to customers who are not themselves PEPs, flagging accounts where a beneficial owner, signatory, or counterparty is an RCA of a listed PEP.

Risk scoring output. The screening event produces a risk score, not just a match indicator. The score reflects the PEP's role, the jurisdiction's CPI ranking, and the relationship type (direct PEP, family member, or business associate).

Full audit trail. Every screening event is logged with a timestamp, the database version used, the match score, the analyst's decision, and the rationale documented in the system. This log is the institution's primary defence in an examination or enforcement inquiry.

Integration with transaction monitoring. PEP status feeds into the transaction monitoring configuration. A match on a counterparty in an international wire transfer triggers both a screening alert and a monitoring review. PEP account flags elevate the sensitivity of transaction monitoring scenarios. The two systems operate as components of a single risk management programme, not independent tools producing separate outputs. The Transaction Monitoring Software Buyer's Guide covers the evaluation criteria for the broader platform, including how screening and monitoring integration should be assessed.

PEP Screening in FinCense

FinCense covers PEP screening as part of its integrated AML platform. It is not a standalone screening module bolted to a separate transaction monitoring system — the PEP identification, risk scoring, and monitoring inputs operate together within the same platform.

The system comes pre-configured with APAC-relevant PEP databases, with fuzzy matching calibrated for the transliteration patterns common in Southeast Asian names. Every screening event is logged in a format that MAS, BNM, BSP, and AUSTRAC examiners can follow — timestamp, database version, match score, disposition, rationale.

When a customer's PEP status changes — a new appointment, a newly documented RCA relationship, an adverse media hit — the platform reflects that change in the monitoring configuration, not only in the customer record.

Book a demo to see FinCense's PEP screening running against APAC-specific scenarios.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

The Role of AML Software in Compliance

Talk to an Expert

Our Thought Leadership Guides

AML Compliance in Singapore: Meeting MAS Requirements with Tookitaki's FinCense

Singapore's MAS sets some of the most demanding AML/CFT standards in Asia-Pacific. Here is how Tookitaki's FinCense helps financial institutions meet MAS Notice 626, the 2024 NRA findings, and ongoing monitoring requirements.

AML Compliance in Singapore: Meeting MAS Requirements with Tookitaki's FinCense

Singapore's MAS sets some of the most demanding AML/CFT standards in Asia-Pacific. Here is how Tookitaki's FinCense helps financial institutions meet MAS Notice 626, the 2024 NRA findings, and ongoing monitoring requirements.