Financial Fraud Solutions in Australia: How to Stay Ahead of Evolving Threats

.svg)

Fraud losses in Australia are soaring — but the right financial fraud solutions can turn the tide.

Fraud is no longer a side concern for Australian financial institutions; it’s a top-line risk. Scamwatch reports that Australians lost over AUD 3 billion in 2024, a figure that continues to rise with the expansion of digital banking, instant payments, and cross-border remittances. Criminals are innovating at breakneck speed, exploiting real-time rails and consumer vulnerabilities. The good news? Modern financial fraud solutions are evolving just as quickly, offering banks, fintechs, and remittance providers smarter ways to fight back.

This blog explores the state of financial fraud in Australia, the most effective solutions available today, and how financial institutions can leverage advanced tools to balance compliance, customer experience, and operational efficiency.

The Fraud Landscape in Australia

1. The Surge in Real-Time Payment Fraud

The New Payments Platform (NPP) has transformed how Australians transact. But its speed also makes it attractive to fraudsters, who can move stolen funds across accounts in seconds — often before detection systems can react.

2. Rise of Social Engineering Scams

Romance scams, investment schemes, and impersonation fraud are thriving. In many cases, victims are tricked into authorising transactions themselves — leaving banks and regulators scrambling to decide who bears responsibility.

3. Cross-Border Laundering

Australia’s geographic and financial ties to Southeast Asia create vulnerabilities in remittance corridors. Fraudsters exploit e-wallets, crypto exchanges, and shell companies to obscure fund flows.

4. Regulatory Expectations

AUSTRAC and ASIC expect proactive fraud controls. Institutions must demonstrate that their solutions are effective, not just present. Failures can lead to penalties in the hundreds of millions, as seen in recent enforcement cases.

What Are Financial Fraud Solutions?

Financial fraud solutions are technologies and processes designed to prevent, detect, and respond to fraudulent activities across banking and payments ecosystems.

They typically include:

- Transaction monitoring systems (real-time analysis of payment flows)

- Identity verification tools (KYC, biometrics, device fingerprinting)

- Case management platforms (workflow automation for investigations)

- AI-powered detection engines (machine learning models that spot anomalies)

- Reporting modules (for AUSTRAC and other regulators)

The best solutions work end-to-end, covering fraud across multiple channels while keeping regulators, customers, and internal teams aligned.

Key Features of Modern Financial Fraud Solutions

1. Real-Time Monitoring

Monitoring transactions as they happen — not after — is critical in an NPP world. Effective systems score and block suspicious transactions in milliseconds.

2. AI & Machine Learning

Criminals don’t stand still, and neither should your systems. AI-driven models adapt to new fraud typologies, reducing false positives while increasing accuracy.

3. Behavioural Analytics

Beyond static rules, advanced systems study user behaviour — from login habits to spending patterns — to detect unusual activity.

4. Multi-Channel Protection

Covers banking transfers, card payments, remittance corridors, crypto exchanges, and e-wallet activity.

5. Identity Verification

Integration with onboarding systems ensures fraudsters using synthetic or stolen identities are caught early.

6. Case Management & Automation

Centralised dashboards let investigators resolve cases faster, while automation handles repetitive tasks like sanctions re-checks or reporting.

7. Regulatory Alignment

Solutions must align with AUSTRAC and FATF recommendations, producing SMRs, audit trails, and explainable alerts.

Common Types of Fraud in Australia and How Solutions Respond

Account Takeover (ATO)

- How it happens: Phishing, malware, or social engineering gives criminals access to accounts.

- Solution response: Device fingerprinting, anomaly detection, and velocity monitoring.

Mule Account Networks

- How it happens: Criminals recruit individuals to move illicit funds through legitimate accounts.

- Solution response: Network analysis and entity resolution linking suspicious accounts.

Investment Scams

- How it happens: Victims are persuaded to transfer money to fraudulent schemes.

- Solution response: Real-time monitoring of unusual transfer chains and new beneficiary accounts.

Card-Not-Present Fraud

- How it happens: Stolen card details used in online transactions.

- Solution response: Behavioural biometrics, anomaly scoring, and fraud scoring models.

Crypto Laundering

- How it happens: Converting illicit fiat into crypto and back.

- Solution response: Wallet screening, blockchain analytics, and integration with crypto KYC.

Red Flags Financial Fraud Solutions Should Detect

- Sudden surge in transactions in dormant accounts

- Login from a new location/device followed by transfers

- Rapid small-value transfers (structuring/smurfing)

- Unusual hours of activity (e.g., high-value midnight transfers)

- Beneficiary details mismatched with customer history

- Transfers routed through high-risk jurisdictions

Evaluating Financial Fraud Solutions in Australia

When selecting a solution, institutions should ask:

- Does it provide real-time detection across all payment rails?

- Is it powered by AI and ML for adaptive intelligence?

- Can it reduce false positives while catching complex fraud?

- Does it integrate with existing AML systems?

- Is it regulator-approved with explainable alerts and audit trails?

- Does the vendor have local Australian expertise?

The Cost Dimension: Balancing Compliance and Efficiency

The cost of fraud prevention isn’t just about software licences — it’s also about operational workload. With false positives accounting for up to 90% of alerts in legacy systems, many Australian institutions overspend on investigations. The right fraud solution should cut costs while boosting accuracy.

Spotlight: Tookitaki’s FinCense

Among leading financial fraud solutions, FinCense by Tookitaki is redefining fraud prevention in Australia.

- Real-Time Monitoring: Detects fraud in milliseconds across NPP and cross-border corridors.

- Agentic AI: Learns from new fraud typologies with minimal false positives.

- Federated Intelligence: Shares insights from the AFC Ecosystem — a global network of AML and fraud experts.

- FinMate AI Copilot: Summarises cases, recommends actions, and generates regulator-ready narratives.

- End-to-End Coverage: From onboarding to investigation, fraud and AML are unified in one platform.

- Full AUSTRAC Compliance: SMR/TTR reporting, audit trails, and explainability baked in.

FinCense doesn’t just detect fraud — it helps compliance teams resolve it faster, cheaper, and with greater confidence.

Future Trends in Financial Fraud Solutions

- Deepfake Detection: Tools to identify manipulated audio and video scams.

- Real-Time Collaboration: Shared fraud databases across institutions to stop scams mid-flight.

- Agentic AI Assistants: Automating investigation tasks end-to-end.

- Cross-Border Intelligence: Stronger coordination with ASEAN regulators to secure remittance corridors.

Conclusion: The Smarter Path to Fraud-Free Finance

The fight against fraud in Australia is intensifying, but so are the solutions. The best financial fraud solutions are intelligent, adaptive, and regulator-aligned — empowering compliance teams to keep pace with both scammers and AUSTRAC.

Pro tip: Choose fraud solutions not just for today’s scams, but for tomorrow’s unknowns. Future-proofing your defences is the only way to stay ahead.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

The Role of AML Software in Compliance

Talk to an Expert

Ready to Streamline Your Anti-Financial Crime Compliance?

Our Thought Leadership Guides

MAS Notice 626 Transaction Monitoring Requirements: A Compliance Guide for Singapore Banks

For banks in Singapore, MAS Notice 626 remains one of the most important foundations of AML compliance. Issued by the Monetary Authority of Singapore, the Notice sets out clear expectations around customer due diligence, transaction monitoring, suspicious transaction reporting, and record-keeping.

This guide focuses on MAS transaction monitoring obligations under MAS Notice 626 and explains what they mean in practice for compliance teams navigating evolving Singapore AML requirements in 2026.

What Is MAS Notice 626?

MAS Notice 626 applies to banks licensed under Singapore’s Banking Act. It forms a core part of the country’s AML/CFT framework and reflects broader international standards, including the FATF Recommendations. It is also supported by MAS Guidelines on AML/CFT, which help banks interpret the rules in practice.

At a high level, MAS Notice 626 covers four key areas:

- customer due diligence

- ongoing monitoring

- suspicious transaction reporting

- record-keeping

For most compliance teams, the most operationally demanding areas are ongoing monitoring and transaction monitoring.

Why MAS Notice 626 Matters for Singapore Banks

Regulators in Singapore have made it clear that AML controls must be more than procedural. MAS has taken enforcement action against banks where weaknesses in monitoring, customer oversight, or investigation processes created gaps in AML/CFT controls.

That is why MAS AML compliance is not simply about maintaining policies. Banks must be able to show that their controls work in practice, especially when it comes to identifying unusual or suspicious activity. In this context, MAS transaction monitoring is one of the most important operational pillars of a bank’s AML framework.

Ongoing Monitoring Requirements Under MAS Notice 626

Paragraph 11 of MAS Notice 626 requires banks to perform ongoing monitoring of customer relationships. In practice, this includes two connected obligations: monitoring transactions and keeping customer information current.

Transaction Monitoring Under MAS Notice 626

Banks must monitor transactions to ensure they are consistent with what the bank knows about the customer, the customer’s business, and the customer’s risk profile.

In practice, this means banks should be able to:

- understand the customer’s expected transaction behaviour

- detect activity that does not align with that expected pattern

- scrutinise the source and destination of unusual funds

- apply enhanced monitoring to high-risk customers and PEPs

This is central to MAS transaction monitoring. The expectation is not only to detect unusual activity, but to assess it in the context of customer risk, expected behaviour, and potential financial crime exposure.

Keeping Customer Due Diligence Information Up to Date

Ongoing monitoring under MAS Notice 626 is not limited to transaction review. Banks must also ensure that customer due diligence information remains accurate and up to date, particularly for higher-risk customers.

If transaction monitoring reveals a meaningful shift in customer behaviour, that should trigger a CDD review. This is an important part of meeting broader Singapore AML requirements, where customer knowledge and transaction behaviour are expected to remain aligned.

What MAS Expects From Transaction Monitoring Systems

MAS has clarified over time what effective monitoring should look like in practice. Several expectations are particularly relevant for banks strengthening their MAS AML compliance frameworks.

1. A Risk-Based Monitoring Approach

A core principle of MAS Notice 626 is that monitoring should be risk-based. Not all customers present the same level of AML/CFT risk, and transaction monitoring should reflect that.

Higher-risk customers, including PEPs, customers linked to high-risk jurisdictions, and customers with complex ownership structures, should be subject to more intensive monitoring. A one-size-fits-all model is unlikely to meet regulatory expectations under modern Singapore AML requirements.

2. Typology Coverage That Reflects Real Risk

MAS expects banks to monitor for the money laundering typologies most relevant to Singapore’s financial system.

These include risks such as:

- trade-based money laundering

- misuse of shell companies and nominees

- placement through casino-linked activity

- abuse of digital payment channels

This means MAS transaction monitoring systems should reflect the real typologies facing Singapore banks, rather than relying on generic scenario libraries that may not match local risk.

3. Alert Quality Over Alert Volume

MAS has also emphasised that more alerts do not automatically mean better monitoring. A system generating high volumes of low-value alerts can create operational noise rather than real control strength.

Banks should be able to demonstrate that thresholds are producing alerts that are relevant, actionable, and properly investigated. Strong MAS AML compliance depends not just on detection, but on the quality of the monitoring outcomes.

4. Documentation and Audit Trail

All monitoring activity should be documented clearly. That includes how alerts are generated, how they are investigated, what decisions are made, and whether escalation to suspicious transaction reporting is necessary.

MAS examiners are likely to review:

- alert workflows

- investigation records

- disposition decisions

- STR-related documentation

For banks in Singapore, this is a critical part of meeting Singapore AML requirements and showing that the monitoring framework is working as intended.

MAS Notice 626 and Correspondent Banking

Banks with correspondent banking relationships face additional monitoring expectations under MAS Notice 626.

MAS requires enhanced scrutiny of these relationships, including:

- understanding the nature and expected volume of activity

- monitoring for patterns inconsistent with the correspondent’s profile

- applying payable-through account controls where relevant

- periodically reviewing whether the relationship remains appropriate

This reflects the higher risks often associated with cross-border flows and nested financial relationships.

Suspicious Transaction Reporting Under MAS Notice 626

Transaction monitoring is often the first stage in identifying conduct that may require a suspicious transaction report. Under MAS Notice 626, banks are expected to file STRs with the Suspicious Transaction Reporting Office within a reasonable timeframe once suspicion is formed.

Key obligations include:

- file an STR as soon as suspicion arises

- do not wait for a minimum threshold, as none applies

- avoid tipping off the subject of the report

- retain the monitoring alert and investigation records that led to the STR

- ensure the STR contains enough information for STRO to act on it

This is where MAS transaction monitoring connects directly with reporting obligations. A bank’s monitoring system must support not only detection, but also sound investigation and reporting processes.

Tipping Off Risk and MAS AML Compliance

One of the most sensitive legal areas within MAS AML compliance is the prohibition on tipping off. Under Singapore law, tipping off is a criminal offence.

That means transaction monitoring and case management systems must be designed carefully so staff do not inadvertently alert a customer whose account or activity is under review.

MAS Notice 626 in the Context of Singapore AML Requirements

MAS Notice 626 should also be viewed in the wider context of Singapore’s broader AML priorities. Singapore’s National Anti-Money Laundering Strategy, published in 2023, signals how the country is thinking about the future of financial crime prevention.

Several themes are especially relevant.

Digital Payment Monitoring

With PayNow and other digital payment channels widely used in Singapore, monitoring frameworks can no longer focus only on traditional wire transfers. Instant payment flows also need to be covered effectively.

This makes real-time monitoring increasingly important within MAS transaction monitoring programmes.

Data Collaboration and Shared Intelligence

The launch of initiatives such as COSMIC suggests that regulators increasingly expect financial institutions to benefit from intelligence sharing, not just internal monitoring signals.

This points to a more connected model of AML detection, where external intelligence can strengthen how banks respond to evolving risks under Singapore AML requirements.

Technology and Innovation

MAS has consistently encouraged financial institutions to adopt RegTech and advanced analytics where these improve AML effectiveness. AI and machine learning-based systems that identify layered, fast-moving, or complex suspicious patterns are increasingly aligned with supervisory expectations.

How Tookitaki Supports MAS Notice 626 Compliance

Tookitaki’s FinCense platform is designed to support the practical demands of MAS Notice 626, especially in areas tied to MAS transaction monitoring and broader MAS AML compliance.

This includes:

- a federated typology network covering Singapore-relevant risks such as trade-based money laundering and PEP monitoring

- risk-based alert scoring that supports differentiated monitoring by customer risk

- full audit trails across alert investigation workflows

- real-time monitoring for PayNow and other digital payment activity

- support for STRO reporting workflows

- explainable AI outputs that help investigators understand and document alert rationale

For banks looking to modernise their AML stack, these capabilities align closely with current Singapore AML requirements and MAS’s technology-forward direction.

Why Effective MAS Transaction Monitoring Matters

The message from regulators is clear. Banks are expected not only to maintain transaction monitoring controls, but to prove that those controls are risk-based, well-calibrated, and effective in practice.

That means banks should be able to:

- monitor customer behaviour against expected patterns

- detect Singapore-relevant AML typologies

- generate alerts that investigators can act on

- maintain clear investigation and audit records

- connect monitoring outcomes to STR and CDD review workflows

In short, MAS transaction monitoring is one of the clearest tests of whether a bank’s AML programme is truly working.

MAS Notice 626 Transaction Monitoring: Key Takeaways

For banks reviewing their transaction monitoring capabilities, the priorities are clear:

- risk-based monitoring linked to customer risk ratings

- typology coverage that reflects Singapore-specific ML/TF risks

- stronger alert quality supported by documented investigations

- real-time monitoring across digital payment channels

- STR workflows that meet regulatory expectations and reduce tipping off risk

- regular threshold review and calibration

- documentation that supports supervisory review and audit readiness

MAS Notice 626 is not just a regulatory framework to reference. It is a practical benchmark for how banks should approach monitoring, investigation, and reporting.

For compliance teams working under evolving Singapore AML requirements, strong transaction monitoring is both a regulatory necessity and an operational advantage. It is what turns AML compliance from a static control framework into a working system that can detect risk in real time.

The QR Code Trap: Why a Simple Scan Is Becoming a Serious Fraud Risk in the Philippines

The most dangerous payment scams do not always look suspicious. Sometimes, they look efficient.

A customer scans a QR code at a shop counter, enters the amount, and completes the payment in seconds. There is no failed transaction, no login alert, no obvious red flag. Everything works exactly as it should. Except the money does not go to the merchant. It goes somewhere else. That is the core risk behind the BSP’s recent warning on “quishing,” including cases where a legitimate merchant QR code may be altered, tampered with, or placed over by another code so payments are redirected to a scammer’s account.

At one level, this sounds like a classic consumer-awareness issue. Check the code. Verify the source. Be careful what you scan. All of that is true. But stopping there misses the bigger point. In the Philippines, QR payments are no longer a novelty. They are part of a broader digital payments ecosystem that has scaled quickly, with digital retail payments accounting for 57.4 percent of monthly retail transaction volume, while QR Ph continues to serve as the national interoperable QR standard for participating banks and non-bank e-money issuers.

That changes the conversation.

Because once QR payments become normal, QR fraud stops being a side story. It becomes a payment-risk issue, a merchant-risk issue, and increasingly, a fraud-and-AML issue wrapped into one.

Why this scam matters more than it first appears

What makes QR code scams so effective is not technical sophistication. It is behavioural precision.

Fraudsters do not need to break into a banking app or compromise a device. They simply exploit trust at the point of payment. A sticker placed over a legitimate merchant code can do what phishing links, fake websites, and spoofed calls often try much harder to achieve: redirect money through a transaction the customer willingly authorises. The BSP warning itself highlights the practical advice consumers should follow, including checking whether a QR code appears altered, tampered with, or placed over another code before scanning. That guidance is telling in itself. It signals that physical manipulation of QR payment points is now a live concern.

For professionals in compliance and fraud, that should immediately raise a harder question. If the payment is customer-authorised and the beneficiary account is valid, what exactly is the institution supposed to detect?

The answer is not always the payment instruction itself. It is the pattern surrounding it.

A scam built for a real-time world

The Philippines has spent years building a more interoperable and inclusive digital payments landscape. QR Ph was developed so a common QR code could be scanned and interpreted by any participating bank or non-bank EMI, making person-to-person and person-to-merchant payments easier across providers. That is good infrastructure. It reduces friction, supports adoption, and brings more merchants into the formal digital economy.

But reduced friction has a downside. It also reduces hesitation.

In older payment settings, there were often natural pauses. A card terminal, a manual account check, a branch interaction, a payment slip. QR payments compress that journey. The customer sees the code, scans it, and moves on. That is the whole point of the experience. It is also why this scam is so well suited to modern payment habits.

Criminals have understood something simple: if a system is built around speed and convenience, the easiest place to attack is the moment when people stop expecting to verify anything.

How the QR code scam typically unfolds

The mechanics are almost painfully straightforward.

A fraudster identifies a merchant that relies on a visible static QR code. That could be a stall, a café, a small retail counter, a delivery collection point, or any setup where the code is printed and left on display. The original code is then covered or replaced with another one linked to a scammer-controlled account or a mule account.

Customers continue paying as usual. They do not think they are sending money to an individual or a different beneficiary. They think they are paying the merchant. The merchant, meanwhile, may not realise anything is wrong until expected payments fail to reconcile.

At that point, the payment journey has already begun.

Funds start landing in the receiving account, often in the form of multiple low-value payments from unrelated senders. In isolation, these do not necessarily look suspicious. In fact, they may resemble ordinary merchant collections. That is what makes this scam harder than it sounds. It can create merchant-like inflows in an account that should not really be behaving like a merchant account at all.

Then comes the real risk. The funds are moved quickly. Split across other accounts. Sent to wallets. Withdrawn in cash. Layered through secondary recipients. The initial fraud is simple. The downstream movement can be much more organised.

That is where the scam begins to overlap with laundering behaviour.

Why fraud teams and AML teams should both care

It is easy to classify QR code payment scams as retail fraud and leave it there. That would be too narrow.

From a fraud perspective, the problem is payment diversion. A customer intends to pay a merchant but sends funds elsewhere.

From an AML perspective, the problem is what happens next. Once diverted funds begin flowing into accounts that collect, move, split, and exit value quickly, institutions are no longer looking at a single fraudulent payment. They are looking at a potential collection-and-layering mechanism hidden inside legitimate payment rails.

This matters because the scam does not need large values to become meaningful. A QR fraud ring does not need one massive transfer. It can rely on volume, repetition, and velocity. Small payments from many victims can create a steady stream of illicit funds that looks unremarkable at transaction level but far more suspicious in aggregate.

That is why the typology deserves more serious treatment. It lives in the overlap between fast payments, mule-account behaviour, and low-friction laundering.

The detection challenge is not the scan. It is the behaviour after the scan.

Most legacy controls were not built for this.

Traditional monitoring logic often performs best when something is clearly out of character: an unusually large transaction, a high-risk jurisdiction, a sanctions hit, a known suspicious counterparty, or a classic account takeover pattern. QR scams may present none of those signals at the front end. The customer has not necessarily been hacked. The payment amount may be ordinary. The transfer rail is legitimate. The receiving account may not yet be watchlisted.

So the wrong question is: how do we detect every suspicious QR payment?

The better question is: how do we detect an account whose behaviour no longer matches its expected role?

That is a much more useful lens.

If a newly opened or low-activity account suddenly begins receiving merchant-like inbound payments from many unrelated individuals, that should matter. If those credits are followed by rapid outbound transfers or repeated cash-out behaviour, that should matter more. If the account sits inside a broader network of linked beneficiaries, shared devices, repeated onward transfers, or mule-like activity patterns, then the case becomes stronger still.

In other words, the problem is behavioural inconsistency, not just transactional abnormality.

Why this is becoming a real-time monitoring problem

This scam is particularly uncomfortable because it plays out at the speed of modern payments.

The BSP’s own digital payments reporting shows how mainstream digital retail payments have become in the Philippines. When money moves that quickly through interoperable rails, institutions lose the luxury of treating suspicious patterns as something to review after the fact. By the time a merchant notices missing collections, an operations team reviews exceptions, or a customer dispute is logged, the funds may already have been transferred onward.

That shifts the burden from retrospective review to timely pattern recognition.

This is not about flagging every small QR payment. That would be unworkable and noisy. It is about identifying where a stream of seemingly routine payments is being routed into an account that starts exhibiting the wrong kind of velocity, concentration, or onward movement.

The intervention window is narrow. That is what makes this a real-time problem, even when the scam itself is physically low-tech.

The merchant ecosystem is an exposed surface

There is also a more uncomfortable operational truth here.

QR-based payment growth often depends on simplicity. Merchants, especially smaller ones, benefit from static printed codes that are cheap, easy to display, and easy for customers to use. But static codes are also easier to tamper with. In some environments, a fraudster does not need cyber capability. A printed overlay is enough.

That does not mean QR adoption is flawed. It means the ecosystem carries a visible attack surface.

The BSP and related QR Ph materials have consistently framed QR Ph as a way to make digital payments interoperable and more convenient for merchants and consumers, including smaller businesses and users beyond traditional card acceptance footprints. That inclusion benefit is real. It is also why institutions need to think carefully about what fraud controls look like when convenience extends to low-cost, visible, physically accessible payment instruments.

In plain terms, if the front-end payment instrument can be tampered with in the real world, then the back-end monitoring has to be smarter.

What better monitoring looks like in practice

The right response to this typology is not a flood of rules. It is a better sense of account behaviour, role, and connected movement.

Institutions should be asking whether they can tell the difference between a genuine merchant collection profile and a personal or mule account trying to imitate one. They should be able to examine how quickly inbound funds are moved onward, whether those patterns are sudden or sustained, whether counterparties are unusually diverse, and whether linked accounts show signs of coordinated activity.

They should also be able to connect fraud signals and AML signals instead of treating them as separate universes. In a QR diversion case, the initial trigger may sit with payment fraud, but the onward flow often sits closer to mule detection and suspicious movement analysis. If those two views are not connected, the institution sees only fragments of the story.

That is where stronger case management, behavioural scoring, and scenario-led monitoring become important.

And this is exactly why Tookitaki’s positioning matters in a case like this. A typology such as QR payment diversion does not demand more noise. It demands better signal. It demands the ability to recognise when an account is behaving outside its expected role, when transaction velocity starts to look inconsistent with ordinary retail activity, and when scattered data points across fraud and AML should really be read as one emerging pattern. For banks and fintechs dealing with increasingly adaptive scams, that shift from isolated alerting to connected intelligence is not a nice-to-have. It is the difference between seeing the payment and seeing the scheme.

A small scam can still reveal a much bigger shift

There is a tendency in financial crime writing to chase the dramatic case. The million-dollar fraud. The cross-border syndicate. The major arrest. Those stories matter, but smaller scams often tell you more about where the system is becoming vulnerable.

This one does exactly that.

A QR code replacement scam is not flashy. It is not technically grand. It may even look mundane compared with deepfakes, synthetic identities, or complex APP fraud chains. But it tells us something important about the current payments environment: fraudsters are increasingly happy to exploit trust, convenience, and physical access instead of sophisticated intrusion. That is not backward. It is efficient.

And for institutions, efficiency is exactly what makes it dangerous.

Because if a criminal can redirect funds without stealing credentials, without breaching an app, and without triggering an obvious failure in the payment experience, then the burden of defence shifts downstream. It shifts to monitoring, behavioural intelligence, and the institution’s ability to recognise when a legitimate payment journey has produced an illegitimate result.

Conclusion: the payment worked, but the control failed

That is the real sting in this typology.

The payment works. The rails work. The customer experience works. What fails is the assumption underneath it.

The BSP’s recent warning on quishing should be read as more than a consumer caution. It is a signal that as digital payments deepen in the Philippines, some of the next fraud risks will come not from breaking the payment system, but from quietly misdirecting trust within it.

For compliance teams, fraud leaders, and risk professionals, the lesson is clear. The problem is no longer limited to whether a transaction was authorised. The harder question is whether the institution can recognise, early enough, when a transaction that looks routine is actually the first step in a scam-and-laundering chain.

That is what makes this worth paying attention to.

Not because it is dramatic.

Because it is plausible, scalable, and built for the exact kind of payment environment the industry has worked so hard to create.

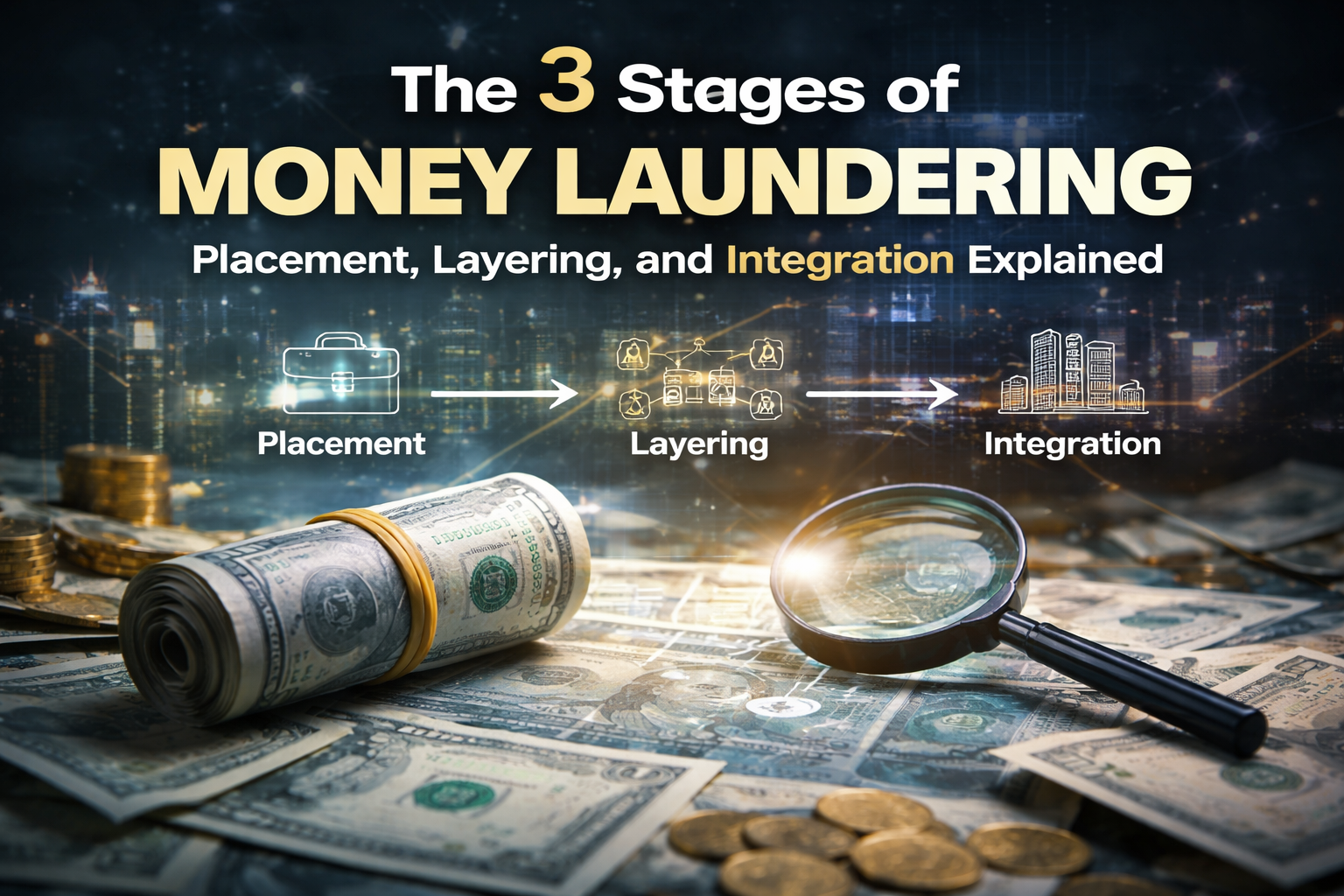

The 3 Stages of Money Laundering: Placement, Layering, and Integration Explained

Dirty money does not become clean overnight. It moves through a process. Funds are introduced into the financial system, shuffled across accounts and jurisdictions, and eventually reappear as seemingly legitimate income or investment. By the time the cycle is complete, the link to the original crime is often buried beneath layers of transactions.

This is why most money laundering schemes, no matter how sophisticated, follow a familiar pattern. Criminal proceeds typically move through three stages: placement, layering, and integration. Each stage serves a different purpose. Placement gets the money into the system. Layering obscures the trail. Integration makes the funds appear legitimate.

For compliance teams, these stages are more than theoretical concepts. They shape how suspicious activity is detected, how alerts are generated, and how investigations are prioritised. Missing one stage can allow illicit funds to slip through even the most advanced monitoring systems.

This is particularly relevant across APAC. Large remittance flows, cross-border trade, digital payment growth, and high-value asset markets create multiple entry points for laundering activity. Understanding how money moves across placement, layering, and integration helps institutions detect risks earlier and connect seemingly unrelated transactions.

{{cta-first}}

What Is Money Laundering?

Money laundering is the process of disguising the origin of illicit funds so they can be used without attracting attention. The proceeds may come from fraud, corruption, organised crime, cybercrime, or other predicate offences. Regardless of the source, the challenge for criminals is the same: they must make illegal money appear legitimate.

Holding large amounts of cash is risky. Spending it directly can trigger scrutiny. Moving funds through the financial system without explanation raises red flags. Laundering solves this problem by gradually distancing the money from its criminal origin.

Regulatory frameworks are designed to disrupt this process. Transaction monitoring, customer due diligence, sanctions screening, and ongoing monitoring all aim to identify activity that fits the laundering lifecycle. Understanding the three stages helps explain why these controls exist and how they work together.

Stage 1: Placement — Getting Dirty Money into the Financial System

Placement is the entry point. Illicit funds must first be introduced into the financial system before they can be moved or disguised. This is often the riskiest stage for criminals because the money is closest to its source.

Large cash deposits, sudden inflows, or unexplained funds are more likely to attract attention. As a result, criminals try to minimise visibility when placing funds.

How Placement Works

One of the most common methods is structuring, sometimes referred to as smurfing. Instead of depositing a large amount at once, funds are broken into smaller transactions below reporting thresholds. These deposits may be spread across multiple branches, accounts, or individuals to avoid detection.

Cash-intensive businesses are another frequently used channel. Illicit funds are mixed with legitimate business revenue, making it difficult to distinguish between legal and illegal income. Restaurants, retail outlets, and service businesses are commonly used for this purpose.

Currency exchanges and monetary instruments also play a role. Cash may be converted into cashier’s cheques, money orders, or foreign currency before being deposited. This adds an additional step between the funds and their origin.

Digital wallets and prepaid instruments have introduced new placement avenues. Funds can be loaded into e-money platforms and then moved digitally, reducing reliance on traditional cash deposits. This is particularly relevant in markets with high adoption of digital payments.

AML Red Flags at the Placement Stage

Compliance teams typically look for patterns such as:

- Multiple deposits just below reporting thresholds

- Cash activity inconsistent with customer profile

- Sudden increases in cash deposits for low-risk customers

- Rapid conversion of cash into monetary instruments

- High cash volume in accounts not expected to handle cash

Placement activity often appears fragmented. Individual transactions may look harmless, but the pattern across accounts reveals the risk.

Stage 2: Layering — Obscuring the Paper Trail

Once funds are inside the financial system, the focus shifts to layering. The goal is to make tracing the origin of money as difficult as possible. This is done by moving funds repeatedly, often across jurisdictions, entities, and financial products.

Layering is typically the most complex stage. It is also where criminals take advantage of the interconnected global financial system.

How Layering Works

International transfers are frequently used. Funds move between multiple accounts in different jurisdictions, sometimes within short timeframes. Each transfer adds distance between the money and its source.

Shell companies and nominee structures are another common tool. Funds are routed through corporate entities where beneficial ownership is difficult to determine. This creates the appearance of legitimate business transactions.

Real estate transactions can also serve layering purposes. Properties may be purchased, transferred, and resold, often through corporate structures. These movements obscure the original funding source.

Cryptocurrency transactions have introduced additional complexity. Mixing services and privacy-focused assets can break the traceability of funds, particularly when combined with traditional banking channels.

Loan-back schemes are also used. Funds are transferred to an entity and then returned as a loan or investment. This creates documentation that appears legitimate, even though the source remains illicit.

AML Red Flags at the Layering Stage

Typical indicators include:

- Rapid movement of funds across multiple accounts

- Transactions with no clear business purpose

- Transfers involving multiple jurisdictions

- Complex ownership structures with unclear beneficiaries

- Circular transaction flows between related entities

- Sudden spikes in cross-border activity

Layering activity often looks like normal financial movement when viewed in isolation. The risk becomes clearer when transactions are analysed as a network rather than individually.

Stage 3: Integration — Entering the Legitimate Economy

Integration is the final stage. By this point, funds have been sufficiently distanced from their origin. The money can now be used with reduced suspicion.

This is where illicit proceeds re-enter the economy as apparently legitimate wealth.

How Integration Works

High-value asset purchases are common. Luxury vehicles, art, jewellery, and other assets can be acquired and later sold, creating legitimate-looking proceeds.

Real estate investments also play a major role. Rental income, resale profits, or property-backed loans provide a credible explanation for funds.

Business investments offer another integration pathway. Laundered money is injected into legitimate businesses, generating revenue that appears lawful.

False invoicing schemes are also used. Payments to shell companies are recorded as business expenses, and the receiving entity reports the funds as legitimate income.

AML Red Flags at the Integration Stage

Compliance teams may observe:

- Asset purchases inconsistent with customer income

- Large investments without clear source of wealth

- Transactions involving offshore entities

- Sudden wealth accumulation without explanation

- Unusual business income patterns

At this stage, the activity often appears legitimate on the surface. Detecting integration requires strong customer risk profiling and ongoing monitoring.

How AML Systems Detect the Three Stages

Modern transaction monitoring does not focus on individual transactions alone. It looks for patterns across the entire lifecycle of funds.

At the placement stage, systems identify structuring behaviour, unusual cash activity, and customer behaviour inconsistent with risk profiles.

At the layering stage, network analytics and behavioural models detect unusual fund flows, circular transactions, and cross-border patterns.

At the integration stage, monitoring shifts toward changes in customer wealth, asset purchases, and unexplained income streams.

When these capabilities are combined, institutions can detect laundering activity even when individual transactions appear normal.

Why All Three Stages Matter for APAC Compliance Teams

Each APAC market presents different exposure points. Large remittance corridors increase placement risk. Cross-border trade creates layering opportunities. High-value asset markets enable integration.

This means effective AML programmes cannot focus on just one stage. Detecting placement without analysing layering flows leaves gaps. Monitoring integration without understanding earlier activity limits context.

Understanding the full lifecycle helps compliance teams connect the dots. Transactions that appear unrelated may form part of a single laundering chain when viewed together.

Ultimately, placement introduces risk. Layering hides it. Integration legitimises it. Effective AML detection requires visibility across all three.

See how Tookitaki FinCense detects money laundering typologies across all three stages here.

MAS Notice 626 Transaction Monitoring Requirements: A Compliance Guide for Singapore Banks

For banks in Singapore, MAS Notice 626 remains one of the most important foundations of AML compliance. Issued by the Monetary Authority of Singapore, the Notice sets out clear expectations around customer due diligence, transaction monitoring, suspicious transaction reporting, and record-keeping.

This guide focuses on MAS transaction monitoring obligations under MAS Notice 626 and explains what they mean in practice for compliance teams navigating evolving Singapore AML requirements in 2026.

What Is MAS Notice 626?

MAS Notice 626 applies to banks licensed under Singapore’s Banking Act. It forms a core part of the country’s AML/CFT framework and reflects broader international standards, including the FATF Recommendations. It is also supported by MAS Guidelines on AML/CFT, which help banks interpret the rules in practice.

At a high level, MAS Notice 626 covers four key areas:

- customer due diligence

- ongoing monitoring

- suspicious transaction reporting

- record-keeping

For most compliance teams, the most operationally demanding areas are ongoing monitoring and transaction monitoring.

Why MAS Notice 626 Matters for Singapore Banks

Regulators in Singapore have made it clear that AML controls must be more than procedural. MAS has taken enforcement action against banks where weaknesses in monitoring, customer oversight, or investigation processes created gaps in AML/CFT controls.

That is why MAS AML compliance is not simply about maintaining policies. Banks must be able to show that their controls work in practice, especially when it comes to identifying unusual or suspicious activity. In this context, MAS transaction monitoring is one of the most important operational pillars of a bank’s AML framework.

Ongoing Monitoring Requirements Under MAS Notice 626

Paragraph 11 of MAS Notice 626 requires banks to perform ongoing monitoring of customer relationships. In practice, this includes two connected obligations: monitoring transactions and keeping customer information current.

Transaction Monitoring Under MAS Notice 626

Banks must monitor transactions to ensure they are consistent with what the bank knows about the customer, the customer’s business, and the customer’s risk profile.

In practice, this means banks should be able to:

- understand the customer’s expected transaction behaviour

- detect activity that does not align with that expected pattern

- scrutinise the source and destination of unusual funds

- apply enhanced monitoring to high-risk customers and PEPs

This is central to MAS transaction monitoring. The expectation is not only to detect unusual activity, but to assess it in the context of customer risk, expected behaviour, and potential financial crime exposure.

Keeping Customer Due Diligence Information Up to Date

Ongoing monitoring under MAS Notice 626 is not limited to transaction review. Banks must also ensure that customer due diligence information remains accurate and up to date, particularly for higher-risk customers.

If transaction monitoring reveals a meaningful shift in customer behaviour, that should trigger a CDD review. This is an important part of meeting broader Singapore AML requirements, where customer knowledge and transaction behaviour are expected to remain aligned.

What MAS Expects From Transaction Monitoring Systems

MAS has clarified over time what effective monitoring should look like in practice. Several expectations are particularly relevant for banks strengthening their MAS AML compliance frameworks.

1. A Risk-Based Monitoring Approach

A core principle of MAS Notice 626 is that monitoring should be risk-based. Not all customers present the same level of AML/CFT risk, and transaction monitoring should reflect that.

Higher-risk customers, including PEPs, customers linked to high-risk jurisdictions, and customers with complex ownership structures, should be subject to more intensive monitoring. A one-size-fits-all model is unlikely to meet regulatory expectations under modern Singapore AML requirements.

2. Typology Coverage That Reflects Real Risk

MAS expects banks to monitor for the money laundering typologies most relevant to Singapore’s financial system.

These include risks such as:

- trade-based money laundering

- misuse of shell companies and nominees

- placement through casino-linked activity

- abuse of digital payment channels

This means MAS transaction monitoring systems should reflect the real typologies facing Singapore banks, rather than relying on generic scenario libraries that may not match local risk.

3. Alert Quality Over Alert Volume

MAS has also emphasised that more alerts do not automatically mean better monitoring. A system generating high volumes of low-value alerts can create operational noise rather than real control strength.

Banks should be able to demonstrate that thresholds are producing alerts that are relevant, actionable, and properly investigated. Strong MAS AML compliance depends not just on detection, but on the quality of the monitoring outcomes.

4. Documentation and Audit Trail

All monitoring activity should be documented clearly. That includes how alerts are generated, how they are investigated, what decisions are made, and whether escalation to suspicious transaction reporting is necessary.

MAS examiners are likely to review:

- alert workflows

- investigation records

- disposition decisions

- STR-related documentation

For banks in Singapore, this is a critical part of meeting Singapore AML requirements and showing that the monitoring framework is working as intended.

MAS Notice 626 and Correspondent Banking

Banks with correspondent banking relationships face additional monitoring expectations under MAS Notice 626.

MAS requires enhanced scrutiny of these relationships, including:

- understanding the nature and expected volume of activity

- monitoring for patterns inconsistent with the correspondent’s profile

- applying payable-through account controls where relevant

- periodically reviewing whether the relationship remains appropriate

This reflects the higher risks often associated with cross-border flows and nested financial relationships.

Suspicious Transaction Reporting Under MAS Notice 626

Transaction monitoring is often the first stage in identifying conduct that may require a suspicious transaction report. Under MAS Notice 626, banks are expected to file STRs with the Suspicious Transaction Reporting Office within a reasonable timeframe once suspicion is formed.

Key obligations include:

- file an STR as soon as suspicion arises

- do not wait for a minimum threshold, as none applies

- avoid tipping off the subject of the report

- retain the monitoring alert and investigation records that led to the STR

- ensure the STR contains enough information for STRO to act on it

This is where MAS transaction monitoring connects directly with reporting obligations. A bank’s monitoring system must support not only detection, but also sound investigation and reporting processes.

Tipping Off Risk and MAS AML Compliance

One of the most sensitive legal areas within MAS AML compliance is the prohibition on tipping off. Under Singapore law, tipping off is a criminal offence.

That means transaction monitoring and case management systems must be designed carefully so staff do not inadvertently alert a customer whose account or activity is under review.

MAS Notice 626 in the Context of Singapore AML Requirements

MAS Notice 626 should also be viewed in the wider context of Singapore’s broader AML priorities. Singapore’s National Anti-Money Laundering Strategy, published in 2023, signals how the country is thinking about the future of financial crime prevention.

Several themes are especially relevant.

Digital Payment Monitoring

With PayNow and other digital payment channels widely used in Singapore, monitoring frameworks can no longer focus only on traditional wire transfers. Instant payment flows also need to be covered effectively.

This makes real-time monitoring increasingly important within MAS transaction monitoring programmes.

Data Collaboration and Shared Intelligence

The launch of initiatives such as COSMIC suggests that regulators increasingly expect financial institutions to benefit from intelligence sharing, not just internal monitoring signals.

This points to a more connected model of AML detection, where external intelligence can strengthen how banks respond to evolving risks under Singapore AML requirements.

Technology and Innovation

MAS has consistently encouraged financial institutions to adopt RegTech and advanced analytics where these improve AML effectiveness. AI and machine learning-based systems that identify layered, fast-moving, or complex suspicious patterns are increasingly aligned with supervisory expectations.

How Tookitaki Supports MAS Notice 626 Compliance

Tookitaki’s FinCense platform is designed to support the practical demands of MAS Notice 626, especially in areas tied to MAS transaction monitoring and broader MAS AML compliance.

This includes:

- a federated typology network covering Singapore-relevant risks such as trade-based money laundering and PEP monitoring

- risk-based alert scoring that supports differentiated monitoring by customer risk

- full audit trails across alert investigation workflows

- real-time monitoring for PayNow and other digital payment activity

- support for STRO reporting workflows

- explainable AI outputs that help investigators understand and document alert rationale

For banks looking to modernise their AML stack, these capabilities align closely with current Singapore AML requirements and MAS’s technology-forward direction.

Why Effective MAS Transaction Monitoring Matters

The message from regulators is clear. Banks are expected not only to maintain transaction monitoring controls, but to prove that those controls are risk-based, well-calibrated, and effective in practice.

That means banks should be able to:

- monitor customer behaviour against expected patterns

- detect Singapore-relevant AML typologies

- generate alerts that investigators can act on

- maintain clear investigation and audit records

- connect monitoring outcomes to STR and CDD review workflows

In short, MAS transaction monitoring is one of the clearest tests of whether a bank’s AML programme is truly working.

MAS Notice 626 Transaction Monitoring: Key Takeaways

For banks reviewing their transaction monitoring capabilities, the priorities are clear:

- risk-based monitoring linked to customer risk ratings

- typology coverage that reflects Singapore-specific ML/TF risks

- stronger alert quality supported by documented investigations

- real-time monitoring across digital payment channels

- STR workflows that meet regulatory expectations and reduce tipping off risk

- regular threshold review and calibration

- documentation that supports supervisory review and audit readiness

MAS Notice 626 is not just a regulatory framework to reference. It is a practical benchmark for how banks should approach monitoring, investigation, and reporting.

For compliance teams working under evolving Singapore AML requirements, strong transaction monitoring is both a regulatory necessity and an operational advantage. It is what turns AML compliance from a static control framework into a working system that can detect risk in real time.

The QR Code Trap: Why a Simple Scan Is Becoming a Serious Fraud Risk in the Philippines

The most dangerous payment scams do not always look suspicious. Sometimes, they look efficient.

A customer scans a QR code at a shop counter, enters the amount, and completes the payment in seconds. There is no failed transaction, no login alert, no obvious red flag. Everything works exactly as it should. Except the money does not go to the merchant. It goes somewhere else. That is the core risk behind the BSP’s recent warning on “quishing,” including cases where a legitimate merchant QR code may be altered, tampered with, or placed over by another code so payments are redirected to a scammer’s account.

At one level, this sounds like a classic consumer-awareness issue. Check the code. Verify the source. Be careful what you scan. All of that is true. But stopping there misses the bigger point. In the Philippines, QR payments are no longer a novelty. They are part of a broader digital payments ecosystem that has scaled quickly, with digital retail payments accounting for 57.4 percent of monthly retail transaction volume, while QR Ph continues to serve as the national interoperable QR standard for participating banks and non-bank e-money issuers.

That changes the conversation.

Because once QR payments become normal, QR fraud stops being a side story. It becomes a payment-risk issue, a merchant-risk issue, and increasingly, a fraud-and-AML issue wrapped into one.

Why this scam matters more than it first appears

What makes QR code scams so effective is not technical sophistication. It is behavioural precision.

Fraudsters do not need to break into a banking app or compromise a device. They simply exploit trust at the point of payment. A sticker placed over a legitimate merchant code can do what phishing links, fake websites, and spoofed calls often try much harder to achieve: redirect money through a transaction the customer willingly authorises. The BSP warning itself highlights the practical advice consumers should follow, including checking whether a QR code appears altered, tampered with, or placed over another code before scanning. That guidance is telling in itself. It signals that physical manipulation of QR payment points is now a live concern.

For professionals in compliance and fraud, that should immediately raise a harder question. If the payment is customer-authorised and the beneficiary account is valid, what exactly is the institution supposed to detect?

The answer is not always the payment instruction itself. It is the pattern surrounding it.

A scam built for a real-time world

The Philippines has spent years building a more interoperable and inclusive digital payments landscape. QR Ph was developed so a common QR code could be scanned and interpreted by any participating bank or non-bank EMI, making person-to-person and person-to-merchant payments easier across providers. That is good infrastructure. It reduces friction, supports adoption, and brings more merchants into the formal digital economy.

But reduced friction has a downside. It also reduces hesitation.

In older payment settings, there were often natural pauses. A card terminal, a manual account check, a branch interaction, a payment slip. QR payments compress that journey. The customer sees the code, scans it, and moves on. That is the whole point of the experience. It is also why this scam is so well suited to modern payment habits.

Criminals have understood something simple: if a system is built around speed and convenience, the easiest place to attack is the moment when people stop expecting to verify anything.

How the QR code scam typically unfolds

The mechanics are almost painfully straightforward.

A fraudster identifies a merchant that relies on a visible static QR code. That could be a stall, a café, a small retail counter, a delivery collection point, or any setup where the code is printed and left on display. The original code is then covered or replaced with another one linked to a scammer-controlled account or a mule account.

Customers continue paying as usual. They do not think they are sending money to an individual or a different beneficiary. They think they are paying the merchant. The merchant, meanwhile, may not realise anything is wrong until expected payments fail to reconcile.

At that point, the payment journey has already begun.

Funds start landing in the receiving account, often in the form of multiple low-value payments from unrelated senders. In isolation, these do not necessarily look suspicious. In fact, they may resemble ordinary merchant collections. That is what makes this scam harder than it sounds. It can create merchant-like inflows in an account that should not really be behaving like a merchant account at all.

Then comes the real risk. The funds are moved quickly. Split across other accounts. Sent to wallets. Withdrawn in cash. Layered through secondary recipients. The initial fraud is simple. The downstream movement can be much more organised.

That is where the scam begins to overlap with laundering behaviour.

Why fraud teams and AML teams should both care

It is easy to classify QR code payment scams as retail fraud and leave it there. That would be too narrow.

From a fraud perspective, the problem is payment diversion. A customer intends to pay a merchant but sends funds elsewhere.

From an AML perspective, the problem is what happens next. Once diverted funds begin flowing into accounts that collect, move, split, and exit value quickly, institutions are no longer looking at a single fraudulent payment. They are looking at a potential collection-and-layering mechanism hidden inside legitimate payment rails.

This matters because the scam does not need large values to become meaningful. A QR fraud ring does not need one massive transfer. It can rely on volume, repetition, and velocity. Small payments from many victims can create a steady stream of illicit funds that looks unremarkable at transaction level but far more suspicious in aggregate.

That is why the typology deserves more serious treatment. It lives in the overlap between fast payments, mule-account behaviour, and low-friction laundering.

The detection challenge is not the scan. It is the behaviour after the scan.

Most legacy controls were not built for this.

Traditional monitoring logic often performs best when something is clearly out of character: an unusually large transaction, a high-risk jurisdiction, a sanctions hit, a known suspicious counterparty, or a classic account takeover pattern. QR scams may present none of those signals at the front end. The customer has not necessarily been hacked. The payment amount may be ordinary. The transfer rail is legitimate. The receiving account may not yet be watchlisted.

So the wrong question is: how do we detect every suspicious QR payment?

The better question is: how do we detect an account whose behaviour no longer matches its expected role?

That is a much more useful lens.

If a newly opened or low-activity account suddenly begins receiving merchant-like inbound payments from many unrelated individuals, that should matter. If those credits are followed by rapid outbound transfers or repeated cash-out behaviour, that should matter more. If the account sits inside a broader network of linked beneficiaries, shared devices, repeated onward transfers, or mule-like activity patterns, then the case becomes stronger still.

In other words, the problem is behavioural inconsistency, not just transactional abnormality.

Why this is becoming a real-time monitoring problem

This scam is particularly uncomfortable because it plays out at the speed of modern payments.

The BSP’s own digital payments reporting shows how mainstream digital retail payments have become in the Philippines. When money moves that quickly through interoperable rails, institutions lose the luxury of treating suspicious patterns as something to review after the fact. By the time a merchant notices missing collections, an operations team reviews exceptions, or a customer dispute is logged, the funds may already have been transferred onward.

That shifts the burden from retrospective review to timely pattern recognition.

This is not about flagging every small QR payment. That would be unworkable and noisy. It is about identifying where a stream of seemingly routine payments is being routed into an account that starts exhibiting the wrong kind of velocity, concentration, or onward movement.

The intervention window is narrow. That is what makes this a real-time problem, even when the scam itself is physically low-tech.

The merchant ecosystem is an exposed surface

There is also a more uncomfortable operational truth here.

QR-based payment growth often depends on simplicity. Merchants, especially smaller ones, benefit from static printed codes that are cheap, easy to display, and easy for customers to use. But static codes are also easier to tamper with. In some environments, a fraudster does not need cyber capability. A printed overlay is enough.

That does not mean QR adoption is flawed. It means the ecosystem carries a visible attack surface.

The BSP and related QR Ph materials have consistently framed QR Ph as a way to make digital payments interoperable and more convenient for merchants and consumers, including smaller businesses and users beyond traditional card acceptance footprints. That inclusion benefit is real. It is also why institutions need to think carefully about what fraud controls look like when convenience extends to low-cost, visible, physically accessible payment instruments.

In plain terms, if the front-end payment instrument can be tampered with in the real world, then the back-end monitoring has to be smarter.

What better monitoring looks like in practice

The right response to this typology is not a flood of rules. It is a better sense of account behaviour, role, and connected movement.

Institutions should be asking whether they can tell the difference between a genuine merchant collection profile and a personal or mule account trying to imitate one. They should be able to examine how quickly inbound funds are moved onward, whether those patterns are sudden or sustained, whether counterparties are unusually diverse, and whether linked accounts show signs of coordinated activity.

They should also be able to connect fraud signals and AML signals instead of treating them as separate universes. In a QR diversion case, the initial trigger may sit with payment fraud, but the onward flow often sits closer to mule detection and suspicious movement analysis. If those two views are not connected, the institution sees only fragments of the story.

That is where stronger case management, behavioural scoring, and scenario-led monitoring become important.

And this is exactly why Tookitaki’s positioning matters in a case like this. A typology such as QR payment diversion does not demand more noise. It demands better signal. It demands the ability to recognise when an account is behaving outside its expected role, when transaction velocity starts to look inconsistent with ordinary retail activity, and when scattered data points across fraud and AML should really be read as one emerging pattern. For banks and fintechs dealing with increasingly adaptive scams, that shift from isolated alerting to connected intelligence is not a nice-to-have. It is the difference between seeing the payment and seeing the scheme.

A small scam can still reveal a much bigger shift

There is a tendency in financial crime writing to chase the dramatic case. The million-dollar fraud. The cross-border syndicate. The major arrest. Those stories matter, but smaller scams often tell you more about where the system is becoming vulnerable.

This one does exactly that.

A QR code replacement scam is not flashy. It is not technically grand. It may even look mundane compared with deepfakes, synthetic identities, or complex APP fraud chains. But it tells us something important about the current payments environment: fraudsters are increasingly happy to exploit trust, convenience, and physical access instead of sophisticated intrusion. That is not backward. It is efficient.

And for institutions, efficiency is exactly what makes it dangerous.

Because if a criminal can redirect funds without stealing credentials, without breaching an app, and without triggering an obvious failure in the payment experience, then the burden of defence shifts downstream. It shifts to monitoring, behavioural intelligence, and the institution’s ability to recognise when a legitimate payment journey has produced an illegitimate result.

Conclusion: the payment worked, but the control failed

That is the real sting in this typology.

The payment works. The rails work. The customer experience works. What fails is the assumption underneath it.

The BSP’s recent warning on quishing should be read as more than a consumer caution. It is a signal that as digital payments deepen in the Philippines, some of the next fraud risks will come not from breaking the payment system, but from quietly misdirecting trust within it.

For compliance teams, fraud leaders, and risk professionals, the lesson is clear. The problem is no longer limited to whether a transaction was authorised. The harder question is whether the institution can recognise, early enough, when a transaction that looks routine is actually the first step in a scam-and-laundering chain.

That is what makes this worth paying attention to.

Not because it is dramatic.

Because it is plausible, scalable, and built for the exact kind of payment environment the industry has worked so hard to create.

The 3 Stages of Money Laundering: Placement, Layering, and Integration Explained

Dirty money does not become clean overnight. It moves through a process. Funds are introduced into the financial system, shuffled across accounts and jurisdictions, and eventually reappear as seemingly legitimate income or investment. By the time the cycle is complete, the link to the original crime is often buried beneath layers of transactions.

This is why most money laundering schemes, no matter how sophisticated, follow a familiar pattern. Criminal proceeds typically move through three stages: placement, layering, and integration. Each stage serves a different purpose. Placement gets the money into the system. Layering obscures the trail. Integration makes the funds appear legitimate.

For compliance teams, these stages are more than theoretical concepts. They shape how suspicious activity is detected, how alerts are generated, and how investigations are prioritised. Missing one stage can allow illicit funds to slip through even the most advanced monitoring systems.

This is particularly relevant across APAC. Large remittance flows, cross-border trade, digital payment growth, and high-value asset markets create multiple entry points for laundering activity. Understanding how money moves across placement, layering, and integration helps institutions detect risks earlier and connect seemingly unrelated transactions.

{{cta-first}}

What Is Money Laundering?

Money laundering is the process of disguising the origin of illicit funds so they can be used without attracting attention. The proceeds may come from fraud, corruption, organised crime, cybercrime, or other predicate offences. Regardless of the source, the challenge for criminals is the same: they must make illegal money appear legitimate.

Holding large amounts of cash is risky. Spending it directly can trigger scrutiny. Moving funds through the financial system without explanation raises red flags. Laundering solves this problem by gradually distancing the money from its criminal origin.

Regulatory frameworks are designed to disrupt this process. Transaction monitoring, customer due diligence, sanctions screening, and ongoing monitoring all aim to identify activity that fits the laundering lifecycle. Understanding the three stages helps explain why these controls exist and how they work together.

Stage 1: Placement — Getting Dirty Money into the Financial System

Placement is the entry point. Illicit funds must first be introduced into the financial system before they can be moved or disguised. This is often the riskiest stage for criminals because the money is closest to its source.

Large cash deposits, sudden inflows, or unexplained funds are more likely to attract attention. As a result, criminals try to minimise visibility when placing funds.

How Placement Works

One of the most common methods is structuring, sometimes referred to as smurfing. Instead of depositing a large amount at once, funds are broken into smaller transactions below reporting thresholds. These deposits may be spread across multiple branches, accounts, or individuals to avoid detection.

Cash-intensive businesses are another frequently used channel. Illicit funds are mixed with legitimate business revenue, making it difficult to distinguish between legal and illegal income. Restaurants, retail outlets, and service businesses are commonly used for this purpose.

Currency exchanges and monetary instruments also play a role. Cash may be converted into cashier’s cheques, money orders, or foreign currency before being deposited. This adds an additional step between the funds and their origin.

Digital wallets and prepaid instruments have introduced new placement avenues. Funds can be loaded into e-money platforms and then moved digitally, reducing reliance on traditional cash deposits. This is particularly relevant in markets with high adoption of digital payments.

AML Red Flags at the Placement Stage

Compliance teams typically look for patterns such as:

- Multiple deposits just below reporting thresholds

- Cash activity inconsistent with customer profile

- Sudden increases in cash deposits for low-risk customers

- Rapid conversion of cash into monetary instruments

- High cash volume in accounts not expected to handle cash

Placement activity often appears fragmented. Individual transactions may look harmless, but the pattern across accounts reveals the risk.

Stage 2: Layering — Obscuring the Paper Trail

Once funds are inside the financial system, the focus shifts to layering. The goal is to make tracing the origin of money as difficult as possible. This is done by moving funds repeatedly, often across jurisdictions, entities, and financial products.

Layering is typically the most complex stage. It is also where criminals take advantage of the interconnected global financial system.

How Layering Works

International transfers are frequently used. Funds move between multiple accounts in different jurisdictions, sometimes within short timeframes. Each transfer adds distance between the money and its source.

Shell companies and nominee structures are another common tool. Funds are routed through corporate entities where beneficial ownership is difficult to determine. This creates the appearance of legitimate business transactions.

Real estate transactions can also serve layering purposes. Properties may be purchased, transferred, and resold, often through corporate structures. These movements obscure the original funding source.

Cryptocurrency transactions have introduced additional complexity. Mixing services and privacy-focused assets can break the traceability of funds, particularly when combined with traditional banking channels.

Loan-back schemes are also used. Funds are transferred to an entity and then returned as a loan or investment. This creates documentation that appears legitimate, even though the source remains illicit.

AML Red Flags at the Layering Stage

Typical indicators include:

- Rapid movement of funds across multiple accounts

- Transactions with no clear business purpose

- Transfers involving multiple jurisdictions

- Complex ownership structures with unclear beneficiaries

- Circular transaction flows between related entities

- Sudden spikes in cross-border activity

Layering activity often looks like normal financial movement when viewed in isolation. The risk becomes clearer when transactions are analysed as a network rather than individually.

Stage 3: Integration — Entering the Legitimate Economy

Integration is the final stage. By this point, funds have been sufficiently distanced from their origin. The money can now be used with reduced suspicion.

This is where illicit proceeds re-enter the economy as apparently legitimate wealth.

How Integration Works

High-value asset purchases are common. Luxury vehicles, art, jewellery, and other assets can be acquired and later sold, creating legitimate-looking proceeds.

Real estate investments also play a major role. Rental income, resale profits, or property-backed loans provide a credible explanation for funds.

Business investments offer another integration pathway. Laundered money is injected into legitimate businesses, generating revenue that appears lawful.

False invoicing schemes are also used. Payments to shell companies are recorded as business expenses, and the receiving entity reports the funds as legitimate income.

AML Red Flags at the Integration Stage

Compliance teams may observe:

- Asset purchases inconsistent with customer income

- Large investments without clear source of wealth

- Transactions involving offshore entities

- Sudden wealth accumulation without explanation

- Unusual business income patterns

At this stage, the activity often appears legitimate on the surface. Detecting integration requires strong customer risk profiling and ongoing monitoring.

How AML Systems Detect the Three Stages

Modern transaction monitoring does not focus on individual transactions alone. It looks for patterns across the entire lifecycle of funds.

At the placement stage, systems identify structuring behaviour, unusual cash activity, and customer behaviour inconsistent with risk profiles.

At the layering stage, network analytics and behavioural models detect unusual fund flows, circular transactions, and cross-border patterns.

At the integration stage, monitoring shifts toward changes in customer wealth, asset purchases, and unexplained income streams.

When these capabilities are combined, institutions can detect laundering activity even when individual transactions appear normal.

Why All Three Stages Matter for APAC Compliance Teams