AML Compliance in Philippines: Key Regulations Your Fintech Must Know

.svg)

Fintech, the innovation of technology in the financial sector, has been rapidly growing in the Philippines. With this growth, the need for regulatory compliance and Anti-Money Laundering (AML) measures has become increasingly important. Fintech companies in the Philippines are facing new challenges to ensure that they are in compliance with AML regulations to prevent illegal activities such as money laundering.

AML compliance is not just a legal requirement but it is also crucial for maintaining the reputation of fintech companies. Financial regulators such as the Philippines Securities and Exchange Commission (SEC) and the Central Bank of the Philippines (BSP) have set AML regulations to ensure that fintech companies are following best practices in preventing illegal activities and maintaining the safety of their customers' funds.

Fintech companies in the Philippines are subject to AML regulations, including customer identification and screening, transaction monitoring, and reporting of suspicious activities. These regulations ensure that fintech companies are collecting and managing user information securely and performing all necessary checks to stay compliant. Regulators like the FATF are actively observing the development of fintech to adjust regulations accordingly and to prevent vulnerabilities in new payment services.

The Role of the BSP in Ensuring AML Compliance

The BSP is the central bank of the Republic of the Philippines and is responsible for providing policy directions in the areas of money, banking, and credit. In order to ensure AML compliance, the BSP exercises regulatory powers as provided by the New Central Bank Act and other relevant laws over the operations of banks, finance companies, and non-bank financial institutions performing quasi-banking functions in the Philippines.

The BSP supervises the operations of fintech companies and exercises regulatory powers over their operations to ensure AML compliance. The BSP also ensures that the country's foreign exchange regulatory framework remains appropriate for the Philippine economy's sustained expansion through its International Operations Department.

The BSP has issued stricter rules, among the first of its kind in the ASEAN, aimed at protecting financial institutions from financial crimes including cyberattacks and cyber threats. Part Nine of the Manual of Regulations of the BSP contains AML regulations, which outline the BSP's authority to check compliance with the Anti-Money Laundering Act (AMLA), as amended. The manual lists out the following AML responsibilities:

- Conduct business in conformity with high ethical standards in order to protect its safety and soundness as well as the integrity of the national banking and financial system;

- Know sufficiently your customer at all times and ensure that the financially or socially disadvantaged are not denied access to financial services while at the same time prevent suspicious individuals or entities from opening or maintaining an account or transacting with the covered person by himself or otherwise;

- Adopt and effectively implement a sound AML and terrorist financing risk management system that identifies, assesses, monitors and controls risks associated with money laundering and terrorist financing;

- Comply fully with this Part and existing laws aimed at combating money laundering and terrorist financing by making sure that officers and employees are aware of their respective responsibilities and carry them out in accordance with superior and principled culture of compliance; and

- Fully cooperate with Anti-Money Laundering Council (AMLC) for the effective implementation and enforcement of the AMLA, as amended.

Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) Regulations

The Philippines implements AML/CTF regulations through the Anti-Money Laundering Act (AMLA) of 2001, as amended. The AMLA aims to prevent and curb money laundering and terrorism financing activities in the country by mandating financial institutions, including fintech companies, to adopt strict customer identification requirements and reporting obligations.

Some of the key provisions of the AMLA include:

- Customer Identification: Financial institutions are required to establish and record the true identity of their clients based on official documents, and to maintain a system of verifying the identity of their clients. Anonymous accounts and accounts under fictitious names are strictly prohibited.

- Record Keeping: Financial institutions must maintain records of all transactions for at least five years from the date of the transaction and preserve records on customer identification for at least five years from the date the account was closed.

- Reporting of Covered Transactions: Financial institutions must report all covered transactions to the Anti-Money Laundering Council (AMLC) within five working days, unless the Supervising Authority concerned prescribes a longer period. Reporting institutions and their employees are prohibited from communicating any information related to the report to any person or entity.

- Authority to Inquire into Deposits: The AMLC may inquire into bank deposits in cases of suspected violation of the AMLA when there is probable cause that the deposits are related to money laundering.

AML/CTF compliance is crucial for fintech companies operating in the Philippines. By adhering to the provisions of the AMLA, fintech companies can help prevent and mitigate the risks of money laundering and terrorism financing activities. Moreover, AML/CTF compliance can also enhance the reputation and credibility of fintech companies in the eyes of customers, regulatory authorities, and financial institutions. Fintech companies that fail to comply with AML/CTF regulations may face severe penalties, including fines, sanctions, and even criminal charges.

Tookitaki's Role in Fintech Compliance

Tookitaki is a leading provider of compliance solutions for the fintech industry. The company offers a suite of solutions designed to help fintech companies meet the ever-growing regulatory requirements in the area of AML/CTF. These solutions are designed to be user-friendly and flexible, allowing fintech companies to customize them to meet their specific needs.

Tookitaki's Anti-Money Laundering Suite (AMLS) is a comprehensive and end-to-end AML compliance platform designed to assist financial institutions in detecting, preventing and managing financial crimes. The platform is built on a foundation of "collective intelligence" which is operationalized to enable partner financial institutions in uncovering money trails that aren’t discoverable by today’s standards and is up-to-date with the newest risk scenarios published by the BSP. The platform uses machine learning and big data analytics to provide a comprehensive approach to detecting and preventing financial crime. This allows financial institutions to identify suspicious activity more quickly and efficiently.

The platform comprises of four modules – Transaction Monitoring, Smart Screening, Customer Risk Scoring and Case Manager – that are optimized for Intelligent Alert Detection (IAD) and Smart Alert Management (SAM). The Transaction Monitoring module helps financial institutions to identify and monitor suspicious transactions in real-time, while the Smart Screening module uses advanced algorithms to automatically screen customer credentials and transaction details for potential risks. The Customer Risk Scoring module dynamically assess a risk score to each customer based on their transaction history and additional layers of personal information, while the Case Manager module allows financial institutions to manage and investigate suspicious activity in a single, unified view.

Tookitaki's solutions offer a range of benefits to fintech companies, including:

- Automated Compliance Monitoring: Tookitaki's solutions automate the compliance monitoring process, helping companies save time and reduce the risk of human error.

- Advanced Analytics: Tookitaki's solutions use advanced analytics to identify suspicious transactions, helping companies stay ahead of money laundering and terrorism financing activities.

- Risk Management: Tookitaki's solutions help fintech companies manage their risk exposure by providing them with a comprehensive understanding of their customers' risk profiles.

- Increased Efficiency: Tookitaki's solutions streamline the compliance process, making it more efficient and reducing the time and effort required to meet regulatory requirements.

Maximize Fintech Success through AML/CTF Compliance with Tookitaki

With a deep understanding of the regulatory landscape and industry trends, Tookitaki's solutions are designed to help companies achieve compliance and mitigate risks. By utilizing Tookitaki's solutions, companies can gain a competitive advantage and ensure that their AML/CTF programs are effective, efficient, and in line with the latest regulations. If you are a fintech company looking to enhance your AML compliance, we invite you to request a demo of Tookitaki's solutions today.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

The Role of AML Software in Compliance

Talk to an Expert

Ready to Streamline Your Anti-Financial Crime Compliance?

Our Thought Leadership Guides

Best AML Software for Singapore: What MAS-Regulated Institutions Need to Evaluate

“Best” isn’t about brand—it’s about fit, foresight, and future readiness.

When compliance teams search for the “best AML software,” they often face a sea of comparisons and vendor rankings. But in reality, what defines the best tool for one institution may fall short for another. In Singapore’s dynamic financial ecosystem, the definition of “best” is evolving.

This blog explores what truly makes AML software best-in-class—not by comparing products, but by unpacking the real-world needs, risks, and expectations shaping compliance today.

The New AML Challenge: Scale, Speed, and Sophistication

Singapore’s status as a global financial hub brings increasing complexity:

- More digital payments

- More cross-border flows

- More fintech integration

- More complex money laundering typologies

Regulators like MAS are raising the bar on detection effectiveness, timeliness of reporting, and technological governance. Meanwhile, fraudsters continue to adapt faster than many internal systems.

In this environment, the best AML software is not the one with the longest feature list—it’s the one that evolves with your institution’s risk.

What “Best” Really Means in AML Software

1. Local Regulatory Fit

AML software must align with MAS regulations—from risk-based assessments to STR formats and AI auditability. A tool not tuned to Singapore’s AML Notices or thematic reviews will create gaps, even if it’s globally recognised.

2. Real-World Scenario Coverage

The best solutions include coverage for real, contextual typologies such as:

- Shell company misuse

- Utility-based layering scams

- Dormant account mule networks

- Round-tripping via fintech platforms

Bonus points if these scenarios come from a network of shared intelligence.

3. AI You Can Explain

The best AML platforms use AI that’s not just powerful—but also understandable. Compliance teams should be able to explain detection decisions to auditors, regulators, and internal stakeholders.

4. Unified View Across Risk

Modern compliance risk doesn't sit in silos. The best software unifies alerts, customer profiles, transactions, device intelligence, and behavioural risk signals—across both fraud and AML workflows.

5. Automation That Actually Works

From auto-generating STRs to summarising case narratives, top AML tools reduce manual work without sacrificing oversight. Automation should support investigators, not replace them.

6. Speed to Deploy, Speed to Detect

The best tools integrate quickly, scale with your transaction volume, and adapt fast to new typologies. In a live environment like Singapore, detection lag can mean regulatory risk.

Why MAS Compliance Requirements Change the Evaluation

Singapore's AML/CFT framework is more prescriptive than most compliance teams from outside the region expect. MAS Notice 626 sets specific requirements for banks and merchant banks: risk-based transaction monitoring with documented calibration, explainable detection decisions for examination purposes, and typology coverage aligned to Singapore's specific ML threat profile. For a full breakdown of what MAS Notice 626 requires from banks and how those requirements translate to monitoring system specifications, see our MAS Notice 626 guide.

For payment service providers licensed under the Payment Services Act 2019, MAS Notice PSN01 and PSN02 set equivalent CDD, transaction monitoring, and STR filing obligations. Software that meets European or US regulatory requirements may not generate the alert documentation, investigation trails, or STR workflows that MAS examiners look for.

The practical evaluation question is not which vendor ranks highest on global analyst lists — it is which solution can demonstrate, in an MAS examination, that:

- Alert thresholds are calibrated to your customer risk profile, not vendor defaults

- Every alert has a documented investigation and disposition decision

- STR workflow meets the "as soon as practicable" filing obligation

- Detection scenarios cover Singapore-specific typologies: mule account networks, PayNow pre-settlement fraud, shell company structuring across corporate accounts

The Role of Community and Collaboration

No tool can solve financial crime alone. The best AML platforms today are:

- Collaborative: Sharing anonymised risk signals across institutions

- Community-driven: Updated with new scenarios and typologies from peers

- Connected: Integrated with ecosystems like MAS’ regulatory sandbox or industry groups

This allows banks to move faster on emerging threats like pig-butchering scams, cross-border laundering, or terror finance alerts.

Case in Point: A Smarter Approach to Typology Detection

Imagine your institution receives a surge in transactions through remittance corridors tied to high-risk jurisdictions. A traditional system may miss this if it’s below a certain threshold.

But a scenario-based system—especially one built from real cases—flags:

- Round dollar amounts at unusual intervals

- Back-to-back remittances to different names in the same region

- Senders with low prior activity suddenly transacting at volume

The “best” software is the one that catches this before damage is done.

A Checklist for Singaporean Institutions

If you’re evaluating AML tools, ask:

- Can this detect known local risks and unknown emerging ones?

- Does it support real-time and batch monitoring across channels?

- Can compliance teams tune thresholds without engineering help?

- Does the vendor offer localised support and regulatory alignment?

- How well does it integrate with fraud tools, case managers, and reporting systems?

If the answer isn’t a confident “yes” across these areas, it might not be your best choice—no matter its global rating.

For a full evaluation framework covering the criteria that matter most for AML software selection, see our Transaction Monitoring Software Buyer's Guide.

What Singapore Institutions Should Prioritise in Their Evaluation

Tookitaki’s FinCense platform embodies these principles—offering MAS-aligned features, community-driven scenarios, explainable AI, and unified fraud and AML coverage tailored to Asia’s compliance landscape.

There’s no universal best AML software.

But for institutions in Singapore, the best choice will always be one that:

- Supports your regulators

- Reflects your risk

- Grows with your customers

- Learns from your industry

- Protects your reputation

Because when it comes to financial crime, it’s not about the software that looks best on paper—it’s about the one that works best in practice.

KYC Requirements in Singapore: MAS CDD Rules for Banks and Payment Companies

Singapore's KYC framework is more specific — and more enforced — than most compliance teams from outside the region expect. The Monetary Authority of Singapore does not publish voluntary guidelines on customer due diligence. It issues Notices: binding legal instruments with criminal penalties for non-compliance. For banks, MAS Notice 626 sets the requirements. For payment service providers licensed under the Payment Services Act, MAS Notice PSN01 and PSN02 apply.

This guide covers what MAS requires for customer identification and verification, the three tiers of CDD Singapore institutions must apply, beneficial ownership obligations, enhanced due diligence triggers, and the recurring gaps MAS examiners find in KYC programmes.

The Regulatory Foundation: MAS Notice 626 and PSN01/PSN02

MAS Notice 626 applies to banks and merchant banks. It sets out prescriptive requirements for:

- Customer due diligence (CDD) — when to perform it, what it must cover, and how to document it

- Enhanced due diligence (EDD) — specific triggers and minimum requirements

- Simplified due diligence (SDD) — the limited circumstances where reduced CDD applies

- Ongoing monitoring of business relationships

- Record keeping

- Suspicious transaction reporting

MAS Notice PSN01 (for standard payment licensees) and MAS Notice PSN02 (for major payment institutions) under the Payment Services Act 2019 set equivalent obligations for payment companies, e-wallets, and remittance operators. The CDD framework in PSN01/PSN02 mirrors the structure of Notice 626 but calibrated to payment service business models — including specific requirements for transaction monitoring on payment flows, cross-border transfers, and digital token services.

Both Notices are regularly updated. Institutions should refer to the current MAS website versions rather than archived copies — amendments following Singapore's 2024 National Risk Assessment update guidance on beneficial ownership verification and higher-risk customer categories.

When CDD Must Be Performed

MAS Notice 626 specifies four triggers requiring CDD to be completed before proceeding:

- Establishing a business relationship — KYC must be completed before onboarding any customer into an ongoing relationship

- Occasional transactions of SGD 5,000 or more — one-off transactions at or above this threshold require CDD even without an ongoing relationship

- Wire transfers of any amount — all wire transfers require CDD, with no minimum threshold

- Suspicion of money laundering or terrorism financing — CDD is required regardless of transaction value or customer type when suspicion arises

The inability to complete CDD to the required standard is grounds for declining to onboard a customer or for terminating an existing business relationship. MAS examiners check that institutions apply this requirement in practice, not just in policy.

Three Tiers of CDD in Singapore

Singapore's CDD framework has three levels, applied based on the customer's assessed risk:

Simplified Due Diligence (SDD)

SDD may be applied — with documented justification — for a limited category of lower-risk customers:

- Singapore government entities and statutory boards

- Companies listed on the Singapore Exchange (SGX) or other approved exchanges

- Regulated financial institutions supervised by MAS or equivalent foreign supervisors

- Certain low-risk products (e.g., basic savings accounts with strict usage limits)

SDD does not mean no due diligence. It means reduced documentation requirements — but institutions must document why SDD applies and maintain that justification in the customer file. MAS does not permit SDD to be applied as a default for corporate customers without case-by-case assessment.

Standard CDD

Standard CDD is the baseline requirement for all other customers. It requires:

- Customer identification: Full legal name, identification document type and number, date of birth (individuals), place of incorporation (entities)

- Verification: Identity documents verified against reliable, independent sources — passports, NRIC, ACRA business registration, corporate documentation

- Beneficial owner identification: For legal entities, identify and verify the natural persons who ultimately own or control the entity (see below for the 25% threshold)

- Purpose and intended nature of the business relationship documented

- Ongoing monitoring of the relationship for consistency with the customer's profile

Enhanced Due Diligence (EDD)

EDD applies to higher-risk customers and situations. MAS Notice 626 specifies mandatory EDD triggers:

- Politically Exposed Persons (PEPs): Foreign PEPs require EDD as a minimum. Domestic PEPs are subject to risk-based assessment. PEP status extends to family members and close associates. Senior management approval is required before establishing or continuing a relationship with a PEP. EDD for PEPs must include source of wealth and source of funds verification — not just identification.

- Correspondent banking relationships: Respondent institution KYC, assessment of AML/CFT controls, and senior management approval before establishing the relationship

- High-risk jurisdictions: Customers or transaction counterparties connected to FATF grey-listed or black-listed countries require EDD and additional scrutiny

- Complex or unusual transactions: Transactions with no apparent economic or legal purpose, or that are inconsistent with the customer's known profile, require EDD investigation before proceeding

- Cross-border private banking: Non-face-to-face account opening for high-net-worth clients from outside Singapore requires additional verification steps

EDD is not satisfied by collecting more documents. MAS examiners look for evidence that the additional information gathered was actually used in the risk assessment — source of wealth narratives that are vague or unsubstantiated are treated as inadequate EDD, not as EDD completed.

Beneficial Owner Verification

Identifying and verifying beneficial owners is one of the most examined areas of Singapore's KYC framework. MAS Notice 626 requires institutions to identify the natural persons who ultimately own or control a legal entity customer.

The threshold is 25% shareholding or voting rights — any natural person who holds, directly or indirectly, 25% or more of a company's shares or voting rights must be identified and verified. Where no natural person holds 25% or more, the institution must identify the natural persons who exercise control through other means — typically senior management.

For layered corporate structures — where ownership runs through multiple holding companies across different jurisdictions — institutions must look through the structure to identify the ultimate beneficial owner. MAS examiners consistently flag beneficial ownership documentation failures as a top finding in corporate customer reviews. Accepting a company registration document without looking through the ownership chain does not satisfy this requirement.

Trusts and other non-corporate legal arrangements require identification of settlors, trustees, and beneficiaries with 25% or greater beneficial interest.

Digital Onboarding and MyInfo

Singapore's national digital identity infrastructure supports MAS-compliant digital onboarding. MyInfo, operated by the Government Technology Agency (GovTech), provides verified personal data — NRIC details, address, employment, and other government-held data — that institutions can retrieve with customer consent.

MAS has confirmed that MyInfo retrieval is acceptable for identity verification purposes, reducing the documentation burden for individual customers. Institutions using MyInfo for onboarding must document the verification method and maintain records of the MyInfo retrieval.

For corporate customers, ACRA's Bizfile registry provides business registration and officer information that can be used for entity verification. Beneficial ownership still requires independent verification — Bizfile shows registered shareholders but does not always reflect ultimate beneficial ownership through nominee structures.

Ongoing Monitoring and Periodic Review

KYC is not a one-time onboarding requirement. MAS Notice 626 requires ongoing monitoring of established business relationships to ensure that transactions remain consistent with the institution's knowledge of the customer.

This has two components:

Transaction monitoring — detecting transactions inconsistent with the customer's business profile, source of funds, or expected transaction patterns. For the transaction monitoring requirements that feed into this ongoing CDD obligation, see our MAS Notice 626 guide.

Periodic CDD review — customer records must be reviewed and updated at intervals appropriate to the customer's risk rating. High-risk customers require more frequent review. The review must check whether the customer's profile has changed, whether beneficial ownership has changed, and whether the risk rating remains appropriate.

The trigger for an out-of-cycle CDD review includes: material changes in transaction patterns, adverse media, connection to a person or entity of concern, and changes in beneficial ownership.

Record-Keeping Requirements

MAS Notice 626 requires institutions to retain CDD records for five years from the end of the business relationship, or five years from the date of the transaction for one-off customers. Records must be maintained in a form that allows reconstruction of individual transactions and can be produced promptly in response to an MAS request or court order.

The five-year clock runs from the end of the relationship — not from when the records were created. For long-term customers, this means maintaining KYC documentation, transaction records, SAR-related records, and correspondence for the full relationship period plus five years.

Suspicious Transaction Reporting

Singapore uses Suspicious Transaction Reports (STRs) filed with the Suspicious Transaction Reporting Office (STRO), administered by the Singapore Police Force. There is no minimum transaction threshold — any transaction, regardless of amount, that raises suspicion must be reported.

STRs must be filed as soon as practicable after suspicion is formed. The Act does not set a specific deadline in days, but MAS examiners and STRO guidance indicate that delays of more than a few business days without documented justification will attract scrutiny.

The tipping-off prohibition under the Corruption, Drug Trafficking and Other Serious Crimes (CDSA) Act makes it a criminal offence to disclose to a customer that an STR has been filed or is under consideration.

For cash transactions of SGD 20,000 or more, institutions must file a Cash Transaction Report (CTR) regardless of suspicion. CTRs are filed with STRO within 15 business days.

Common KYC Failures in MAS Examinations

MAS's examination findings and industry guidance consistently flag the same recurring gaps:

Beneficial ownership not traced to ultimate natural persons. Institutions stop at the first layer of corporate ownership without looking through nominee shareholders or holding company structures to identify the actual controlling individuals.

EDD documentation without substantive assessment. Files contain EDD documents — source of wealth declarations, bank statements, company accounts — but no evidence that the documents were reviewed, assessed, or used to update the risk rating.

PEP definitions applied too narrowly. Institutions identify foreign government ministers as PEPs but miss domestic senior officials, senior executives of state-owned enterprises, and immediate family members of identified PEPs.

Static customer profiles. CDD completed at onboarding is never updated. Customers whose transaction patterns have changed significantly since onboarding retain their original risk rating without periodic review.

MyInfo used as a complete KYC solution. MyInfo satisfies identity verification for individuals but does not substitute for source of funds verification, purpose of relationship documentation, or beneficial ownership checks on corporate structures.

STR delays. Suspicion forms during transaction review but is not escalated or filed for days or weeks. Case management systems without deadline tracking are the most common operational cause.

For Singapore institutions evaluating whether their current KYC and monitoring systems can meet these requirements, see our Transaction Monitoring Software Buyer's Guide for a full framework covering the capabilities MAS-regulated institutions need.

Transaction Monitoring in New Zealand: FMA, RBNZ and DIA Requirements

New Zealand sits under less external scrutiny than Singapore or Australia, but its domestic enforcement record tells a different story. Three supervisors — the Reserve Bank of New Zealand, the Financial Markets Authority, and the Department of Internal Affairs — run active examination programmes. A mandatory Section 59 audit every two years creates a hard compliance deadline. And the AML/CFT Act's risk-based approach means institutions cannot rely on vendor defaults or generic rule sets to satisfy supervisors.

For banks, payment service providers, and fintechs operating in New Zealand, transaction monitoring is the operational centre of AML/CFT compliance. This guide covers what the Act requires, how the supervisory structure affects monitoring obligations, and where institutions most commonly fail examination.

The AML/CFT Act 2009: New Zealand's Core Framework

New Zealand's AML/CFT framework is governed by the Anti-Money Laundering and Countering Financing of Terrorism Act 2009. Phase 1 entities — banks, non-bank deposit takers, and most financial institutions — came into scope in June 2013. Phase 2 extended obligations to lawyers, accountants, real estate agents, and other designated businesses in stages from 2018 to 2019.

The Act operates on a risk-based model. There is no prescriptive list of transaction monitoring rules an institution must run. Instead, institutions must:

- Conduct a written risk assessment that identifies their specific ML/FT risks based on customer type, product set, and delivery channels

- Implement a compliance programme derived from that assessment, including monitoring and detection controls designed to address identified risks

- Review and update the risk assessment whenever material changes occur — new products, new customer segments, new channels

This principle-based approach gives institutions flexibility but removes the ability to claim compliance by pointing to a vendor's default configuration. If your monitoring is not designed around your assessed risks, supervisors will find the gap.

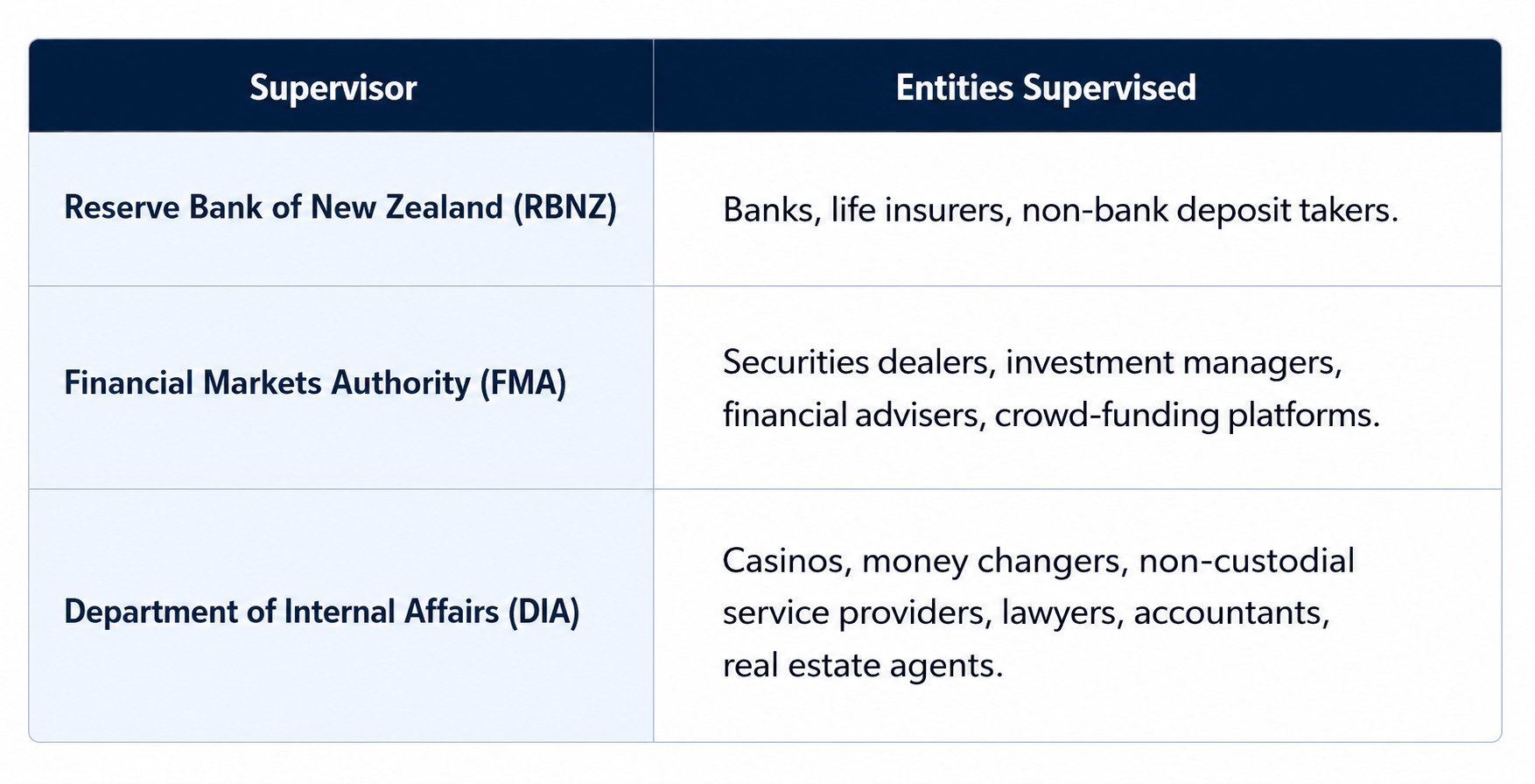

Three Supervisors: FMA, RBNZ and DIA

New Zealand's supervisory structure is unusual among APAC jurisdictions. While Australia has AUSTRAC and Singapore has MAS, New Zealand has three supervisors, each with jurisdiction over distinct entity types:

Each supervisor publishes its own guidance and runs its own examination priorities. The practical implication: guidance from AUSTRAC or MAS does not map directly onto New Zealand's framework. Institutions need to engage with their specific supervisor's published materials and annual risk focus areas.

For most banks and payment companies, RBNZ is the relevant supervisor. For digital asset businesses and VASPs, DIA is the supervisor following the 2021 amendments.

Who Must Comply

The Act applies to "reporting entities" — a defined category covering most financial businesses operating in New Zealand:

- Banks (including branches of foreign banks)

- Non-bank deposit takers: credit unions, building societies, finance companies

- Money remittance operators and foreign exchange dealers

- Life insurance companies

- Securities dealers, brokers, and investment managers

- Trustee companies

- Virtual asset service providers (VASPs) — brought in scope June 2021

The VASP inclusion is significant. The AML/CFT (Amendment) Act 2021 extended reporting entity obligations to crypto exchanges, digital asset custodians, and related businesses. DIA supervises most VASPs, with specific guidance on digital asset typologies.

Transaction Monitoring Obligations

The AML/CFT Act does not use "transaction monitoring" as a defined technical term the way MAS Notice 626 does. What it requires is that institutions implement systems and controls within their compliance programme to detect unusual and suspicious activity.

In practice, a compliant transaction monitoring function requires:

Documented risk-based detection scenarios. Monitoring rules or behavioural detection scenarios must be designed to detect the specific ML/FT risks identified in your risk assessment. A retail bank serving Pacific Island remittance customers needs different scenarios than a corporate securities dealer. Supervisors check the alignment between the risk assessment and the monitoring controls — generic vendor defaults that have not been configured to your institution's risk profile will not satisfy this requirement.

Alert investigation records. Every alert generated must be investigated, and the investigation and disposition decision must be documented. An alert closed as a false positive requires documentation of why. An alert that escalates to a SAR requires the full investigation trail. Alert backlogs — alerts generated but not reviewed — are among the most common examination findings.

Annual programme review with board sign-off. The Act requires the compliance programme, including monitoring controls, to be reviewed annually. The compliance officer must report to senior management and the board. Evidence of this reporting chain is a standard examination request.

Calibration and effectiveness review. Supervisors look for evidence that monitoring scenarios are reviewed for effectiveness — whether they are generating useful alerts or producing excessive false positives without adjustment. A monitoring programme that has not been reviewed or calibrated since deployment will attract scrutiny.

Reporting Requirements: PTRs and SARs

Transaction monitoring outputs feed two mandatory reporting obligations:

Prescribed Transaction Reports (PTRs) are threshold-based and mandatory — they do not require suspicion. PTRs must be filed with the New Zealand Police Financial Intelligence Unit (FIU) via the goAML platform for:

- Cash transactions of NZD 10,000 or more

- International wire transfers of NZD 1,000 or more (in or out)

The filing deadline is within 10 working days of the transaction. PTR monitoring requires specific detection for transactions at and around these thresholds, including structuring patterns where customers conduct multiple sub-threshold transactions to avoid PTR obligations.

Suspicious Activity Reports (SARs) — New Zealand uses "SAR" rather than "STR" (Suspicious Transaction Report). SARs must be filed as soon as practicable, and no later than three working days after forming a suspicion. The threshold for suspicion is lower than many teams assume: reasonable grounds to suspect money laundering or financing of terrorism are sufficient — certainty is not required.

SARs are filed with the NZ Police FIU via goAML. The tipping-off prohibition under the Act makes it a criminal offence to disclose to a customer that a SAR has been filed or is under consideration.

The Section 59 Audit Requirement

The most operationally distinctive element of New Zealand's framework is the Section 59 audit. Every reporting entity must arrange for an independent audit of its AML/CFT programme at intervals of no more than two years.

The auditor must assess whether:

- The risk assessment accurately reflects the entity's current ML/FT risk profile

- The compliance programme is adequate to manage those risks

- Transaction monitoring controls are functioning as designed and generating appropriate outputs

- PTR and SAR reporting is accurate, complete, and timely

- Staff training is adequate

The two-year cycle creates a hard deadline. Institutions with monitoring gaps, stale risk assessments, or unresolved findings from the previous audit cycle will face those issues again. The audit is also a forcing function for calibration: institutions that have not reviewed their detection scenarios or addressed alert backlogs before the audit will have those gaps documented in the audit report — which supervisors can and do request.

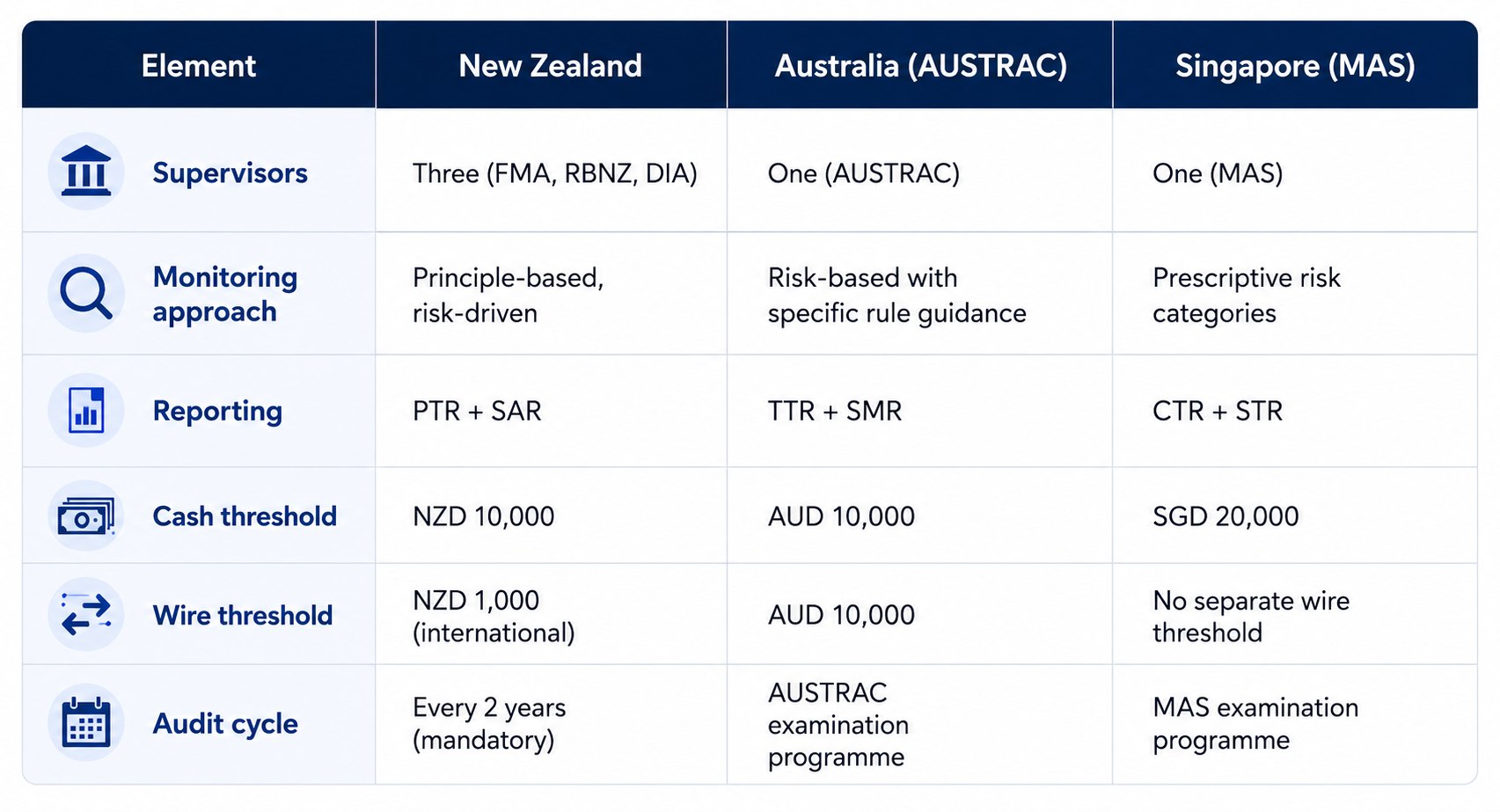

How NZ Compares to Australia and Singapore

For compliance teams managing obligations across multiple APAC jurisdictions, the structural differences matter:

The wire transfer threshold is the most operationally significant difference. New Zealand's NZD 1,000 threshold for international wires generates substantially more PTR volume than Australian or Singapore equivalents. Institutions managing cross-border payment flows into or out of New Zealand need PTR-specific monitoring that can handle this volume.

Common Transaction Monitoring Gaps in NZ Examinations

Supervisors across all three agencies have documented recurring compliance failures. The most common transaction monitoring gaps are:

Risk assessment not driving monitoring design. The risk assessment identifies high-risk customer segments or products, but the monitoring system runs generic rules that do not target those specific risks. Supervisors treat this as a material failure — the Act requires the programme to be derived from the risk assessment, not run alongside it.

PTR monitoring gaps. Institutions with strong SAR-based monitoring often have inadequate controls for PTR-triggering transactions. Structuring below the NZD 10,000 cash threshold requires specific detection scenarios that standard bank rule sets do not include.

Alert backlogs. Alerts generated but not reviewed within a reasonable timeframe are a consistent finding. Unlike some jurisdictions with prescribed investigation timelines, the Act does not specify deadlines — but supervisors expect evidence of timely review, and large backlogs indicate the monitoring system is generating more output than the team can process.

Stale risk assessments. The Act requires risk assessments to be updated when material changes occur. Institutions that have launched new products, added new customer segments, or changed delivery channels without updating their risk assessment are out of compliance with this requirement.

VASP-specific coverage gaps. For DIA-supervised VASPs, standard bank-oriented monitoring rule sets do not address digital asset typologies: wallet clustering, rapid conversion between asset types, cross-chain transfers, and structuring patterns in low-value token transactions. VASPs need detection scenarios specific to their product and customer risk profile.

What a Compliant NZ Transaction Monitoring Programme Requires

For institutions operating under the AML/CFT Act, a compliant monitoring programme requires:

- A current, documented risk assessment aligned to your actual customer base and product set

- Monitoring scenarios designed to detect the specific risks in that assessment, not vendor defaults

- Alert investigation workflows with documented disposition for every alert

- PTR-specific detection for cash and wire transactions at and around the NZD 10,000 and NZD 1,000 thresholds

- SAR workflow with a three-working-day filing deadline built into case management

- Annual programme review with board sign-off documentation

- Section 59 audit preparation: calibration review, rule effectiveness documentation, and remediation of any open findings before the audit cycle closes

For institutions evaluating whether their current monitoring system can support these requirements across New Zealand and other APAC markets, see our Transaction Monitoring Software Buyer's Guide.

Best AML Software for Singapore: What MAS-Regulated Institutions Need to Evaluate

“Best” isn’t about brand—it’s about fit, foresight, and future readiness.

When compliance teams search for the “best AML software,” they often face a sea of comparisons and vendor rankings. But in reality, what defines the best tool for one institution may fall short for another. In Singapore’s dynamic financial ecosystem, the definition of “best” is evolving.

This blog explores what truly makes AML software best-in-class—not by comparing products, but by unpacking the real-world needs, risks, and expectations shaping compliance today.

The New AML Challenge: Scale, Speed, and Sophistication

Singapore’s status as a global financial hub brings increasing complexity:

- More digital payments

- More cross-border flows

- More fintech integration

- More complex money laundering typologies

Regulators like MAS are raising the bar on detection effectiveness, timeliness of reporting, and technological governance. Meanwhile, fraudsters continue to adapt faster than many internal systems.

In this environment, the best AML software is not the one with the longest feature list—it’s the one that evolves with your institution’s risk.

What “Best” Really Means in AML Software

1. Local Regulatory Fit

AML software must align with MAS regulations—from risk-based assessments to STR formats and AI auditability. A tool not tuned to Singapore’s AML Notices or thematic reviews will create gaps, even if it’s globally recognised.

2. Real-World Scenario Coverage

The best solutions include coverage for real, contextual typologies such as:

- Shell company misuse

- Utility-based layering scams

- Dormant account mule networks

- Round-tripping via fintech platforms

Bonus points if these scenarios come from a network of shared intelligence.

3. AI You Can Explain

The best AML platforms use AI that’s not just powerful—but also understandable. Compliance teams should be able to explain detection decisions to auditors, regulators, and internal stakeholders.

4. Unified View Across Risk

Modern compliance risk doesn't sit in silos. The best software unifies alerts, customer profiles, transactions, device intelligence, and behavioural risk signals—across both fraud and AML workflows.

5. Automation That Actually Works

From auto-generating STRs to summarising case narratives, top AML tools reduce manual work without sacrificing oversight. Automation should support investigators, not replace them.

6. Speed to Deploy, Speed to Detect

The best tools integrate quickly, scale with your transaction volume, and adapt fast to new typologies. In a live environment like Singapore, detection lag can mean regulatory risk.

Why MAS Compliance Requirements Change the Evaluation

Singapore's AML/CFT framework is more prescriptive than most compliance teams from outside the region expect. MAS Notice 626 sets specific requirements for banks and merchant banks: risk-based transaction monitoring with documented calibration, explainable detection decisions for examination purposes, and typology coverage aligned to Singapore's specific ML threat profile. For a full breakdown of what MAS Notice 626 requires from banks and how those requirements translate to monitoring system specifications, see our MAS Notice 626 guide.

For payment service providers licensed under the Payment Services Act 2019, MAS Notice PSN01 and PSN02 set equivalent CDD, transaction monitoring, and STR filing obligations. Software that meets European or US regulatory requirements may not generate the alert documentation, investigation trails, or STR workflows that MAS examiners look for.

The practical evaluation question is not which vendor ranks highest on global analyst lists — it is which solution can demonstrate, in an MAS examination, that:

- Alert thresholds are calibrated to your customer risk profile, not vendor defaults

- Every alert has a documented investigation and disposition decision

- STR workflow meets the "as soon as practicable" filing obligation

- Detection scenarios cover Singapore-specific typologies: mule account networks, PayNow pre-settlement fraud, shell company structuring across corporate accounts

The Role of Community and Collaboration

No tool can solve financial crime alone. The best AML platforms today are:

- Collaborative: Sharing anonymised risk signals across institutions

- Community-driven: Updated with new scenarios and typologies from peers

- Connected: Integrated with ecosystems like MAS’ regulatory sandbox or industry groups

This allows banks to move faster on emerging threats like pig-butchering scams, cross-border laundering, or terror finance alerts.

Case in Point: A Smarter Approach to Typology Detection

Imagine your institution receives a surge in transactions through remittance corridors tied to high-risk jurisdictions. A traditional system may miss this if it’s below a certain threshold.

But a scenario-based system—especially one built from real cases—flags:

- Round dollar amounts at unusual intervals

- Back-to-back remittances to different names in the same region

- Senders with low prior activity suddenly transacting at volume

The “best” software is the one that catches this before damage is done.

A Checklist for Singaporean Institutions

If you’re evaluating AML tools, ask:

- Can this detect known local risks and unknown emerging ones?

- Does it support real-time and batch monitoring across channels?

- Can compliance teams tune thresholds without engineering help?

- Does the vendor offer localised support and regulatory alignment?

- How well does it integrate with fraud tools, case managers, and reporting systems?

If the answer isn’t a confident “yes” across these areas, it might not be your best choice—no matter its global rating.

For a full evaluation framework covering the criteria that matter most for AML software selection, see our Transaction Monitoring Software Buyer's Guide.

What Singapore Institutions Should Prioritise in Their Evaluation

Tookitaki’s FinCense platform embodies these principles—offering MAS-aligned features, community-driven scenarios, explainable AI, and unified fraud and AML coverage tailored to Asia’s compliance landscape.

There’s no universal best AML software.

But for institutions in Singapore, the best choice will always be one that:

- Supports your regulators

- Reflects your risk

- Grows with your customers

- Learns from your industry

- Protects your reputation

Because when it comes to financial crime, it’s not about the software that looks best on paper—it’s about the one that works best in practice.

KYC Requirements in Singapore: MAS CDD Rules for Banks and Payment Companies

Singapore's KYC framework is more specific — and more enforced — than most compliance teams from outside the region expect. The Monetary Authority of Singapore does not publish voluntary guidelines on customer due diligence. It issues Notices: binding legal instruments with criminal penalties for non-compliance. For banks, MAS Notice 626 sets the requirements. For payment service providers licensed under the Payment Services Act, MAS Notice PSN01 and PSN02 apply.

This guide covers what MAS requires for customer identification and verification, the three tiers of CDD Singapore institutions must apply, beneficial ownership obligations, enhanced due diligence triggers, and the recurring gaps MAS examiners find in KYC programmes.

The Regulatory Foundation: MAS Notice 626 and PSN01/PSN02

MAS Notice 626 applies to banks and merchant banks. It sets out prescriptive requirements for:

- Customer due diligence (CDD) — when to perform it, what it must cover, and how to document it

- Enhanced due diligence (EDD) — specific triggers and minimum requirements

- Simplified due diligence (SDD) — the limited circumstances where reduced CDD applies

- Ongoing monitoring of business relationships

- Record keeping

- Suspicious transaction reporting

MAS Notice PSN01 (for standard payment licensees) and MAS Notice PSN02 (for major payment institutions) under the Payment Services Act 2019 set equivalent obligations for payment companies, e-wallets, and remittance operators. The CDD framework in PSN01/PSN02 mirrors the structure of Notice 626 but calibrated to payment service business models — including specific requirements for transaction monitoring on payment flows, cross-border transfers, and digital token services.

Both Notices are regularly updated. Institutions should refer to the current MAS website versions rather than archived copies — amendments following Singapore's 2024 National Risk Assessment update guidance on beneficial ownership verification and higher-risk customer categories.

When CDD Must Be Performed

MAS Notice 626 specifies four triggers requiring CDD to be completed before proceeding:

- Establishing a business relationship — KYC must be completed before onboarding any customer into an ongoing relationship

- Occasional transactions of SGD 5,000 or more — one-off transactions at or above this threshold require CDD even without an ongoing relationship

- Wire transfers of any amount — all wire transfers require CDD, with no minimum threshold

- Suspicion of money laundering or terrorism financing — CDD is required regardless of transaction value or customer type when suspicion arises

The inability to complete CDD to the required standard is grounds for declining to onboard a customer or for terminating an existing business relationship. MAS examiners check that institutions apply this requirement in practice, not just in policy.

Three Tiers of CDD in Singapore

Singapore's CDD framework has three levels, applied based on the customer's assessed risk:

Simplified Due Diligence (SDD)

SDD may be applied — with documented justification — for a limited category of lower-risk customers:

- Singapore government entities and statutory boards

- Companies listed on the Singapore Exchange (SGX) or other approved exchanges

- Regulated financial institutions supervised by MAS or equivalent foreign supervisors

- Certain low-risk products (e.g., basic savings accounts with strict usage limits)

SDD does not mean no due diligence. It means reduced documentation requirements — but institutions must document why SDD applies and maintain that justification in the customer file. MAS does not permit SDD to be applied as a default for corporate customers without case-by-case assessment.

Standard CDD

Standard CDD is the baseline requirement for all other customers. It requires:

- Customer identification: Full legal name, identification document type and number, date of birth (individuals), place of incorporation (entities)

- Verification: Identity documents verified against reliable, independent sources — passports, NRIC, ACRA business registration, corporate documentation

- Beneficial owner identification: For legal entities, identify and verify the natural persons who ultimately own or control the entity (see below for the 25% threshold)

- Purpose and intended nature of the business relationship documented

- Ongoing monitoring of the relationship for consistency with the customer's profile

Enhanced Due Diligence (EDD)

EDD applies to higher-risk customers and situations. MAS Notice 626 specifies mandatory EDD triggers:

- Politically Exposed Persons (PEPs): Foreign PEPs require EDD as a minimum. Domestic PEPs are subject to risk-based assessment. PEP status extends to family members and close associates. Senior management approval is required before establishing or continuing a relationship with a PEP. EDD for PEPs must include source of wealth and source of funds verification — not just identification.

- Correspondent banking relationships: Respondent institution KYC, assessment of AML/CFT controls, and senior management approval before establishing the relationship

- High-risk jurisdictions: Customers or transaction counterparties connected to FATF grey-listed or black-listed countries require EDD and additional scrutiny

- Complex or unusual transactions: Transactions with no apparent economic or legal purpose, or that are inconsistent with the customer's known profile, require EDD investigation before proceeding

- Cross-border private banking: Non-face-to-face account opening for high-net-worth clients from outside Singapore requires additional verification steps

EDD is not satisfied by collecting more documents. MAS examiners look for evidence that the additional information gathered was actually used in the risk assessment — source of wealth narratives that are vague or unsubstantiated are treated as inadequate EDD, not as EDD completed.

Beneficial Owner Verification

Identifying and verifying beneficial owners is one of the most examined areas of Singapore's KYC framework. MAS Notice 626 requires institutions to identify the natural persons who ultimately own or control a legal entity customer.

The threshold is 25% shareholding or voting rights — any natural person who holds, directly or indirectly, 25% or more of a company's shares or voting rights must be identified and verified. Where no natural person holds 25% or more, the institution must identify the natural persons who exercise control through other means — typically senior management.

For layered corporate structures — where ownership runs through multiple holding companies across different jurisdictions — institutions must look through the structure to identify the ultimate beneficial owner. MAS examiners consistently flag beneficial ownership documentation failures as a top finding in corporate customer reviews. Accepting a company registration document without looking through the ownership chain does not satisfy this requirement.

Trusts and other non-corporate legal arrangements require identification of settlors, trustees, and beneficiaries with 25% or greater beneficial interest.

Digital Onboarding and MyInfo

Singapore's national digital identity infrastructure supports MAS-compliant digital onboarding. MyInfo, operated by the Government Technology Agency (GovTech), provides verified personal data — NRIC details, address, employment, and other government-held data — that institutions can retrieve with customer consent.

MAS has confirmed that MyInfo retrieval is acceptable for identity verification purposes, reducing the documentation burden for individual customers. Institutions using MyInfo for onboarding must document the verification method and maintain records of the MyInfo retrieval.

For corporate customers, ACRA's Bizfile registry provides business registration and officer information that can be used for entity verification. Beneficial ownership still requires independent verification — Bizfile shows registered shareholders but does not always reflect ultimate beneficial ownership through nominee structures.

Ongoing Monitoring and Periodic Review

KYC is not a one-time onboarding requirement. MAS Notice 626 requires ongoing monitoring of established business relationships to ensure that transactions remain consistent with the institution's knowledge of the customer.

This has two components:

Transaction monitoring — detecting transactions inconsistent with the customer's business profile, source of funds, or expected transaction patterns. For the transaction monitoring requirements that feed into this ongoing CDD obligation, see our MAS Notice 626 guide.

Periodic CDD review — customer records must be reviewed and updated at intervals appropriate to the customer's risk rating. High-risk customers require more frequent review. The review must check whether the customer's profile has changed, whether beneficial ownership has changed, and whether the risk rating remains appropriate.

The trigger for an out-of-cycle CDD review includes: material changes in transaction patterns, adverse media, connection to a person or entity of concern, and changes in beneficial ownership.

Record-Keeping Requirements

MAS Notice 626 requires institutions to retain CDD records for five years from the end of the business relationship, or five years from the date of the transaction for one-off customers. Records must be maintained in a form that allows reconstruction of individual transactions and can be produced promptly in response to an MAS request or court order.

The five-year clock runs from the end of the relationship — not from when the records were created. For long-term customers, this means maintaining KYC documentation, transaction records, SAR-related records, and correspondence for the full relationship period plus five years.

Suspicious Transaction Reporting

Singapore uses Suspicious Transaction Reports (STRs) filed with the Suspicious Transaction Reporting Office (STRO), administered by the Singapore Police Force. There is no minimum transaction threshold — any transaction, regardless of amount, that raises suspicion must be reported.

STRs must be filed as soon as practicable after suspicion is formed. The Act does not set a specific deadline in days, but MAS examiners and STRO guidance indicate that delays of more than a few business days without documented justification will attract scrutiny.

The tipping-off prohibition under the Corruption, Drug Trafficking and Other Serious Crimes (CDSA) Act makes it a criminal offence to disclose to a customer that an STR has been filed or is under consideration.

For cash transactions of SGD 20,000 or more, institutions must file a Cash Transaction Report (CTR) regardless of suspicion. CTRs are filed with STRO within 15 business days.

Common KYC Failures in MAS Examinations

MAS's examination findings and industry guidance consistently flag the same recurring gaps:

Beneficial ownership not traced to ultimate natural persons. Institutions stop at the first layer of corporate ownership without looking through nominee shareholders or holding company structures to identify the actual controlling individuals.

EDD documentation without substantive assessment. Files contain EDD documents — source of wealth declarations, bank statements, company accounts — but no evidence that the documents were reviewed, assessed, or used to update the risk rating.

PEP definitions applied too narrowly. Institutions identify foreign government ministers as PEPs but miss domestic senior officials, senior executives of state-owned enterprises, and immediate family members of identified PEPs.

Static customer profiles. CDD completed at onboarding is never updated. Customers whose transaction patterns have changed significantly since onboarding retain their original risk rating without periodic review.

MyInfo used as a complete KYC solution. MyInfo satisfies identity verification for individuals but does not substitute for source of funds verification, purpose of relationship documentation, or beneficial ownership checks on corporate structures.

STR delays. Suspicion forms during transaction review but is not escalated or filed for days or weeks. Case management systems without deadline tracking are the most common operational cause.

For Singapore institutions evaluating whether their current KYC and monitoring systems can meet these requirements, see our Transaction Monitoring Software Buyer's Guide for a full framework covering the capabilities MAS-regulated institutions need.

Transaction Monitoring in New Zealand: FMA, RBNZ and DIA Requirements

New Zealand sits under less external scrutiny than Singapore or Australia, but its domestic enforcement record tells a different story. Three supervisors — the Reserve Bank of New Zealand, the Financial Markets Authority, and the Department of Internal Affairs — run active examination programmes. A mandatory Section 59 audit every two years creates a hard compliance deadline. And the AML/CFT Act's risk-based approach means institutions cannot rely on vendor defaults or generic rule sets to satisfy supervisors.

For banks, payment service providers, and fintechs operating in New Zealand, transaction monitoring is the operational centre of AML/CFT compliance. This guide covers what the Act requires, how the supervisory structure affects monitoring obligations, and where institutions most commonly fail examination.

The AML/CFT Act 2009: New Zealand's Core Framework

New Zealand's AML/CFT framework is governed by the Anti-Money Laundering and Countering Financing of Terrorism Act 2009. Phase 1 entities — banks, non-bank deposit takers, and most financial institutions — came into scope in June 2013. Phase 2 extended obligations to lawyers, accountants, real estate agents, and other designated businesses in stages from 2018 to 2019.

The Act operates on a risk-based model. There is no prescriptive list of transaction monitoring rules an institution must run. Instead, institutions must:

- Conduct a written risk assessment that identifies their specific ML/FT risks based on customer type, product set, and delivery channels

- Implement a compliance programme derived from that assessment, including monitoring and detection controls designed to address identified risks

- Review and update the risk assessment whenever material changes occur — new products, new customer segments, new channels

This principle-based approach gives institutions flexibility but removes the ability to claim compliance by pointing to a vendor's default configuration. If your monitoring is not designed around your assessed risks, supervisors will find the gap.

Three Supervisors: FMA, RBNZ and DIA

New Zealand's supervisory structure is unusual among APAC jurisdictions. While Australia has AUSTRAC and Singapore has MAS, New Zealand has three supervisors, each with jurisdiction over distinct entity types:

Each supervisor publishes its own guidance and runs its own examination priorities. The practical implication: guidance from AUSTRAC or MAS does not map directly onto New Zealand's framework. Institutions need to engage with their specific supervisor's published materials and annual risk focus areas.

For most banks and payment companies, RBNZ is the relevant supervisor. For digital asset businesses and VASPs, DIA is the supervisor following the 2021 amendments.

Who Must Comply

The Act applies to "reporting entities" — a defined category covering most financial businesses operating in New Zealand:

- Banks (including branches of foreign banks)

- Non-bank deposit takers: credit unions, building societies, finance companies

- Money remittance operators and foreign exchange dealers

- Life insurance companies

- Securities dealers, brokers, and investment managers

- Trustee companies

- Virtual asset service providers (VASPs) — brought in scope June 2021

The VASP inclusion is significant. The AML/CFT (Amendment) Act 2021 extended reporting entity obligations to crypto exchanges, digital asset custodians, and related businesses. DIA supervises most VASPs, with specific guidance on digital asset typologies.

Transaction Monitoring Obligations

The AML/CFT Act does not use "transaction monitoring" as a defined technical term the way MAS Notice 626 does. What it requires is that institutions implement systems and controls within their compliance programme to detect unusual and suspicious activity.

In practice, a compliant transaction monitoring function requires:

Documented risk-based detection scenarios. Monitoring rules or behavioural detection scenarios must be designed to detect the specific ML/FT risks identified in your risk assessment. A retail bank serving Pacific Island remittance customers needs different scenarios than a corporate securities dealer. Supervisors check the alignment between the risk assessment and the monitoring controls — generic vendor defaults that have not been configured to your institution's risk profile will not satisfy this requirement.

Alert investigation records. Every alert generated must be investigated, and the investigation and disposition decision must be documented. An alert closed as a false positive requires documentation of why. An alert that escalates to a SAR requires the full investigation trail. Alert backlogs — alerts generated but not reviewed — are among the most common examination findings.

Annual programme review with board sign-off. The Act requires the compliance programme, including monitoring controls, to be reviewed annually. The compliance officer must report to senior management and the board. Evidence of this reporting chain is a standard examination request.

Calibration and effectiveness review. Supervisors look for evidence that monitoring scenarios are reviewed for effectiveness — whether they are generating useful alerts or producing excessive false positives without adjustment. A monitoring programme that has not been reviewed or calibrated since deployment will attract scrutiny.

Reporting Requirements: PTRs and SARs

Transaction monitoring outputs feed two mandatory reporting obligations:

Prescribed Transaction Reports (PTRs) are threshold-based and mandatory — they do not require suspicion. PTRs must be filed with the New Zealand Police Financial Intelligence Unit (FIU) via the goAML platform for:

- Cash transactions of NZD 10,000 or more

- International wire transfers of NZD 1,000 or more (in or out)

The filing deadline is within 10 working days of the transaction. PTR monitoring requires specific detection for transactions at and around these thresholds, including structuring patterns where customers conduct multiple sub-threshold transactions to avoid PTR obligations.

Suspicious Activity Reports (SARs) — New Zealand uses "SAR" rather than "STR" (Suspicious Transaction Report). SARs must be filed as soon as practicable, and no later than three working days after forming a suspicion. The threshold for suspicion is lower than many teams assume: reasonable grounds to suspect money laundering or financing of terrorism are sufficient — certainty is not required.

SARs are filed with the NZ Police FIU via goAML. The tipping-off prohibition under the Act makes it a criminal offence to disclose to a customer that a SAR has been filed or is under consideration.

The Section 59 Audit Requirement

The most operationally distinctive element of New Zealand's framework is the Section 59 audit. Every reporting entity must arrange for an independent audit of its AML/CFT programme at intervals of no more than two years.

The auditor must assess whether:

- The risk assessment accurately reflects the entity's current ML/FT risk profile

- The compliance programme is adequate to manage those risks

- Transaction monitoring controls are functioning as designed and generating appropriate outputs

- PTR and SAR reporting is accurate, complete, and timely

- Staff training is adequate

The two-year cycle creates a hard deadline. Institutions with monitoring gaps, stale risk assessments, or unresolved findings from the previous audit cycle will face those issues again. The audit is also a forcing function for calibration: institutions that have not reviewed their detection scenarios or addressed alert backlogs before the audit will have those gaps documented in the audit report — which supervisors can and do request.

How NZ Compares to Australia and Singapore

For compliance teams managing obligations across multiple APAC jurisdictions, the structural differences matter:

The wire transfer threshold is the most operationally significant difference. New Zealand's NZD 1,000 threshold for international wires generates substantially more PTR volume than Australian or Singapore equivalents. Institutions managing cross-border payment flows into or out of New Zealand need PTR-specific monitoring that can handle this volume.

Common Transaction Monitoring Gaps in NZ Examinations

Supervisors across all three agencies have documented recurring compliance failures. The most common transaction monitoring gaps are:

Risk assessment not driving monitoring design. The risk assessment identifies high-risk customer segments or products, but the monitoring system runs generic rules that do not target those specific risks. Supervisors treat this as a material failure — the Act requires the programme to be derived from the risk assessment, not run alongside it.

PTR monitoring gaps. Institutions with strong SAR-based monitoring often have inadequate controls for PTR-triggering transactions. Structuring below the NZD 10,000 cash threshold requires specific detection scenarios that standard bank rule sets do not include.

Alert backlogs. Alerts generated but not reviewed within a reasonable timeframe are a consistent finding. Unlike some jurisdictions with prescribed investigation timelines, the Act does not specify deadlines — but supervisors expect evidence of timely review, and large backlogs indicate the monitoring system is generating more output than the team can process.

Stale risk assessments. The Act requires risk assessments to be updated when material changes occur. Institutions that have launched new products, added new customer segments, or changed delivery channels without updating their risk assessment are out of compliance with this requirement.

VASP-specific coverage gaps. For DIA-supervised VASPs, standard bank-oriented monitoring rule sets do not address digital asset typologies: wallet clustering, rapid conversion between asset types, cross-chain transfers, and structuring patterns in low-value token transactions. VASPs need detection scenarios specific to their product and customer risk profile.

What a Compliant NZ Transaction Monitoring Programme Requires

For institutions operating under the AML/CFT Act, a compliant monitoring programme requires:

- A current, documented risk assessment aligned to your actual customer base and product set

- Monitoring scenarios designed to detect the specific risks in that assessment, not vendor defaults

- Alert investigation workflows with documented disposition for every alert

- PTR-specific detection for cash and wire transactions at and around the NZD 10,000 and NZD 1,000 thresholds

- SAR workflow with a three-working-day filing deadline built into case management

- Annual programme review with board sign-off documentation

- Section 59 audit preparation: calibration review, rule effectiveness documentation, and remediation of any open findings before the audit cycle closes

For institutions evaluating whether their current monitoring system can support these requirements across New Zealand and other APAC markets, see our Transaction Monitoring Software Buyer's Guide.