Suspicious Transaction Monitoring: The Backbone of Financial Crime Prevention

.svg)

Suspicious transaction monitoring is no longer a checkbox—it’s a critical line of defence in the fight against financial crime.

As criminals adopt increasingly sophisticated laundering and fraud tactics, financial institutions must evolve just as quickly. Suspicious transaction monitoring (STM) empowers banks and fintechs to identify, investigate, and report potentially illicit activities before they escalate into regulatory breaches or financial losses.

STM involves the continuous analysis of financial transactions to flag anomalies that may signal money laundering, fraud, or terrorist financing. It’s a foundational component of any effective anti-money laundering (AML) strategy, helping institutions ensure compliance and safeguard trust.

In this guide, we’ll explore:

- How suspicious transaction monitoring works in real-world environments

- Key technologies and trends transforming STM capabilities

- Actionable strategies to strengthen AML compliance through smarter monitoring

Let’s dive into how AI-powered STM tools are reshaping the future of financial crime prevention.

{{cta-first}}

Why Suspicious Transaction Monitoring is Crucial for Financial Institutions

Financial institutions serve as the first line of defense in combating financial crime. They are required to detect, assess, and report suspicious transactions to regulatory authorities like the Financial Action Task Force (FATF), FinCEN, and local AML regulators.

Failing to implement effective suspicious transaction monitoring can lead to:

- Regulatory penalties amounting to millions in fines.

- Reputational damage, leading to customer trust erosion.

- Operational risks, as undetected fraudulent activities can destabilize institutions.

What Triggers Suspicious Transaction Monitoring?

A suspicious transaction is any financial activity that deviates from a customer’s normal behavior or involves high-risk geographies, industries, or entities. Common triggers include:

- Unusually large cash deposits or withdrawals.

- Frequent transactions with offshore accounts or high-risk jurisdictions.

- Sudden changes in transaction patterns.

- Structuring transactions just below reporting thresholds.

- Multiple small transactions within a short period ("smurfing").

- Unexplained fund transfers to unknown third parties.

Detecting these red flags in real time is critical for preventing financial crime and ensuring compliance.

How AML Transaction Monitoring Systems Work

Modern AML transaction monitoring systems leverage AI-driven analytics and regulatory frameworks to detect anomalies and identify suspicious activities. These systems automate compliance efforts, helping financial institutions reduce false positives and enhance fraud detection.

Key Functionalities of a Robust Transaction Monitoring System

- Real-time and batch transaction monitoring to track illicit transactions.

- Rule-based and AI-powered anomaly detection for pattern recognition.

- Automated alerts and risk-scoring for investigative prioritization.

- Comprehensive case management & SAR filing for regulatory compliance.

- Seamless integration with AML databases and external watchlists.

An effective transaction monitoring system should evolve alongside regulatory changes and emerging financial crime tactics.

Key Features of an Effective Suspicious Transaction Monitoring System

The best transaction monitoring systems go beyond simple rule-based detection by integrating AI, machine learning, and behavioral analytics.

Essential Features for AML Compliance

- Behavioral Learning – AI-powered tools analyze historical transaction data to recognize evolving fraud patterns.

- Dynamic Risk Scoring – Assigning risk levels based on transaction complexity and customer profiles.

- Real-Time Case Management – Automating suspicious transaction reporting (STRs) and SAR filings.

- Integration with External Data Sources – Ensuring compliance by connecting with regulatory watchlists.

- User-Friendly Dashboards – Enhancing investigator efficiency with intuitive interfaces and automation.

Advanced compliance platforms like Tookitaki’s FinCense provide AI-powered suspicious transaction monitoring, reducing false positives while strengthening risk detection.

The Role of AI and Machine Learning in Suspicious Transaction Monitoring

Artificial Intelligence (AI) and Machine Learning (ML) are transforming AML compliance by:

- Reducing False Positives – AI models analyze transaction histories to differentiate between legitimate transactions and actual threats.

- Enhancing Fraud Detection – ML algorithms adapt to new fraud tactics, detecting evolving threats faster than rule-based systems.

- Automating Investigations – AI prioritizes alerts based on risk scores, reducing manual workload and increasing efficiency.

- Improving Accuracy Over Time – Machine learning models continuously refine themselves using real-world data.

AI-powered STM enhances compliance efficiency, ensuring faster fraud detection and response.

{{cta-whitepaper}}

Implementing a Risk-Based Approach to Transaction Monitoring

A risk-based approach ensures more effective fraud detection while optimizing compliance resources.

- Customer Risk Profiling – High-risk customers (e.g., cash-intensive businesses) require more stringent monitoring.

- Geographic Risk Assessment – Transactions with high-risk jurisdictions demand enhanced due diligence (EDD).

- Transaction Pattern Analysis – Identifying deviations in customer transaction behavior to flag anomalies.

- Continuous Model Optimization – Updating risk rules based on new fraud trends and regulatory changes.

Financial institutions using a risk-based approach significantly improve fraud detection while minimizing compliance costs.

Final Thoughts: Strengthening Compliance Through Smarter Monitoring

Suspicious transaction monitoring is no longer just about compliance—it is a critical pillar in safeguarding financial institutions from financial crime, fraud, and reputational risks.

With regulatory expectations rising and fraud tactics evolving, financial institutions must embrace AI-powered monitoring solutions that provide:

- Real-time fraud detection and risk-based compliance.

- Advanced AI and ML-driven suspicious transaction monitoring.

- Predictive analytics for proactive financial crime prevention.

Tookitaki’s FinCense platform offers a cutting-edge, AI-driven approach to suspicious transaction monitoring, helping financial institutions reduce false positives, enhance fraud detection, and improve overall compliance efficiency. By integrating federated learning and advanced risk intelligence, Tookitaki empowers compliance teams to stay ahead of financial criminals.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

The Role of AML Software in Compliance

Talk to an Expert

Ready to Streamline Your Anti-Financial Crime Compliance?

Our Thought Leadership Guides

KYC Requirements in Singapore: MAS CDD Rules for Banks and Payment Companies

Singapore's KYC framework is more specific — and more enforced — than most compliance teams from outside the region expect. The Monetary Authority of Singapore does not publish voluntary guidelines on customer due diligence. It issues Notices: binding legal instruments with criminal penalties for non-compliance. For banks, MAS Notice 626 sets the requirements. For payment service providers licensed under the Payment Services Act, MAS Notice PSN01 and PSN02 apply.

This guide covers what MAS requires for customer identification and verification, the three tiers of CDD Singapore institutions must apply, beneficial ownership obligations, enhanced due diligence triggers, and the recurring gaps MAS examiners find in KYC programmes.

The Regulatory Foundation: MAS Notice 626 and PSN01/PSN02

MAS Notice 626 applies to banks and merchant banks. It sets out prescriptive requirements for:

- Customer due diligence (CDD) — when to perform it, what it must cover, and how to document it

- Enhanced due diligence (EDD) — specific triggers and minimum requirements

- Simplified due diligence (SDD) — the limited circumstances where reduced CDD applies

- Ongoing monitoring of business relationships

- Record keeping

- Suspicious transaction reporting

MAS Notice PSN01 (for standard payment licensees) and MAS Notice PSN02 (for major payment institutions) under the Payment Services Act 2019 set equivalent obligations for payment companies, e-wallets, and remittance operators. The CDD framework in PSN01/PSN02 mirrors the structure of Notice 626 but calibrated to payment service business models — including specific requirements for transaction monitoring on payment flows, cross-border transfers, and digital token services.

Both Notices are regularly updated. Institutions should refer to the current MAS website versions rather than archived copies — amendments following Singapore's 2024 National Risk Assessment update guidance on beneficial ownership verification and higher-risk customer categories.

When CDD Must Be Performed

MAS Notice 626 specifies four triggers requiring CDD to be completed before proceeding:

- Establishing a business relationship — KYC must be completed before onboarding any customer into an ongoing relationship

- Occasional transactions of SGD 5,000 or more — one-off transactions at or above this threshold require CDD even without an ongoing relationship

- Wire transfers of any amount — all wire transfers require CDD, with no minimum threshold

- Suspicion of money laundering or terrorism financing — CDD is required regardless of transaction value or customer type when suspicion arises

The inability to complete CDD to the required standard is grounds for declining to onboard a customer or for terminating an existing business relationship. MAS examiners check that institutions apply this requirement in practice, not just in policy.

Three Tiers of CDD in Singapore

Singapore's CDD framework has three levels, applied based on the customer's assessed risk:

Simplified Due Diligence (SDD)

SDD may be applied — with documented justification — for a limited category of lower-risk customers:

- Singapore government entities and statutory boards

- Companies listed on the Singapore Exchange (SGX) or other approved exchanges

- Regulated financial institutions supervised by MAS or equivalent foreign supervisors

- Certain low-risk products (e.g., basic savings accounts with strict usage limits)

SDD does not mean no due diligence. It means reduced documentation requirements — but institutions must document why SDD applies and maintain that justification in the customer file. MAS does not permit SDD to be applied as a default for corporate customers without case-by-case assessment.

Standard CDD

Standard CDD is the baseline requirement for all other customers. It requires:

- Customer identification: Full legal name, identification document type and number, date of birth (individuals), place of incorporation (entities)

- Verification: Identity documents verified against reliable, independent sources — passports, NRIC, ACRA business registration, corporate documentation

- Beneficial owner identification: For legal entities, identify and verify the natural persons who ultimately own or control the entity (see below for the 25% threshold)

- Purpose and intended nature of the business relationship documented

- Ongoing monitoring of the relationship for consistency with the customer's profile

Enhanced Due Diligence (EDD)

EDD applies to higher-risk customers and situations. MAS Notice 626 specifies mandatory EDD triggers:

- Politically Exposed Persons (PEPs): Foreign PEPs require EDD as a minimum. Domestic PEPs are subject to risk-based assessment. PEP status extends to family members and close associates. Senior management approval is required before establishing or continuing a relationship with a PEP. EDD for PEPs must include source of wealth and source of funds verification — not just identification.

- Correspondent banking relationships: Respondent institution KYC, assessment of AML/CFT controls, and senior management approval before establishing the relationship

- High-risk jurisdictions: Customers or transaction counterparties connected to FATF grey-listed or black-listed countries require EDD and additional scrutiny

- Complex or unusual transactions: Transactions with no apparent economic or legal purpose, or that are inconsistent with the customer's known profile, require EDD investigation before proceeding

- Cross-border private banking: Non-face-to-face account opening for high-net-worth clients from outside Singapore requires additional verification steps

EDD is not satisfied by collecting more documents. MAS examiners look for evidence that the additional information gathered was actually used in the risk assessment — source of wealth narratives that are vague or unsubstantiated are treated as inadequate EDD, not as EDD completed.

Beneficial Owner Verification

Identifying and verifying beneficial owners is one of the most examined areas of Singapore's KYC framework. MAS Notice 626 requires institutions to identify the natural persons who ultimately own or control a legal entity customer.

The threshold is 25% shareholding or voting rights — any natural person who holds, directly or indirectly, 25% or more of a company's shares or voting rights must be identified and verified. Where no natural person holds 25% or more, the institution must identify the natural persons who exercise control through other means — typically senior management.

For layered corporate structures — where ownership runs through multiple holding companies across different jurisdictions — institutions must look through the structure to identify the ultimate beneficial owner. MAS examiners consistently flag beneficial ownership documentation failures as a top finding in corporate customer reviews. Accepting a company registration document without looking through the ownership chain does not satisfy this requirement.

Trusts and other non-corporate legal arrangements require identification of settlors, trustees, and beneficiaries with 25% or greater beneficial interest.

Digital Onboarding and MyInfo

Singapore's national digital identity infrastructure supports MAS-compliant digital onboarding. MyInfo, operated by the Government Technology Agency (GovTech), provides verified personal data — NRIC details, address, employment, and other government-held data — that institutions can retrieve with customer consent.

MAS has confirmed that MyInfo retrieval is acceptable for identity verification purposes, reducing the documentation burden for individual customers. Institutions using MyInfo for onboarding must document the verification method and maintain records of the MyInfo retrieval.

For corporate customers, ACRA's Bizfile registry provides business registration and officer information that can be used for entity verification. Beneficial ownership still requires independent verification — Bizfile shows registered shareholders but does not always reflect ultimate beneficial ownership through nominee structures.

Ongoing Monitoring and Periodic Review

KYC is not a one-time onboarding requirement. MAS Notice 626 requires ongoing monitoring of established business relationships to ensure that transactions remain consistent with the institution's knowledge of the customer.

This has two components:

Transaction monitoring — detecting transactions inconsistent with the customer's business profile, source of funds, or expected transaction patterns. For the transaction monitoring requirements that feed into this ongoing CDD obligation, see our MAS Notice 626 guide.

Periodic CDD review — customer records must be reviewed and updated at intervals appropriate to the customer's risk rating. High-risk customers require more frequent review. The review must check whether the customer's profile has changed, whether beneficial ownership has changed, and whether the risk rating remains appropriate.

The trigger for an out-of-cycle CDD review includes: material changes in transaction patterns, adverse media, connection to a person or entity of concern, and changes in beneficial ownership.

Record-Keeping Requirements

MAS Notice 626 requires institutions to retain CDD records for five years from the end of the business relationship, or five years from the date of the transaction for one-off customers. Records must be maintained in a form that allows reconstruction of individual transactions and can be produced promptly in response to an MAS request or court order.

The five-year clock runs from the end of the relationship — not from when the records were created. For long-term customers, this means maintaining KYC documentation, transaction records, SAR-related records, and correspondence for the full relationship period plus five years.

Suspicious Transaction Reporting

Singapore uses Suspicious Transaction Reports (STRs) filed with the Suspicious Transaction Reporting Office (STRO), administered by the Singapore Police Force. There is no minimum transaction threshold — any transaction, regardless of amount, that raises suspicion must be reported.

STRs must be filed as soon as practicable after suspicion is formed. The Act does not set a specific deadline in days, but MAS examiners and STRO guidance indicate that delays of more than a few business days without documented justification will attract scrutiny.

The tipping-off prohibition under the Corruption, Drug Trafficking and Other Serious Crimes (CDSA) Act makes it a criminal offence to disclose to a customer that an STR has been filed or is under consideration.

For cash transactions of SGD 20,000 or more, institutions must file a Cash Transaction Report (CTR) regardless of suspicion. CTRs are filed with STRO within 15 business days.

Common KYC Failures in MAS Examinations

MAS's examination findings and industry guidance consistently flag the same recurring gaps:

Beneficial ownership not traced to ultimate natural persons. Institutions stop at the first layer of corporate ownership without looking through nominee shareholders or holding company structures to identify the actual controlling individuals.

EDD documentation without substantive assessment. Files contain EDD documents — source of wealth declarations, bank statements, company accounts — but no evidence that the documents were reviewed, assessed, or used to update the risk rating.

PEP definitions applied too narrowly. Institutions identify foreign government ministers as PEPs but miss domestic senior officials, senior executives of state-owned enterprises, and immediate family members of identified PEPs.

Static customer profiles. CDD completed at onboarding is never updated. Customers whose transaction patterns have changed significantly since onboarding retain their original risk rating without periodic review.

MyInfo used as a complete KYC solution. MyInfo satisfies identity verification for individuals but does not substitute for source of funds verification, purpose of relationship documentation, or beneficial ownership checks on corporate structures.

STR delays. Suspicion forms during transaction review but is not escalated or filed for days or weeks. Case management systems without deadline tracking are the most common operational cause.

For Singapore institutions evaluating whether their current KYC and monitoring systems can meet these requirements, see our Transaction Monitoring Software Buyer's Guide for a full framework covering the capabilities MAS-regulated institutions need.

Transaction Monitoring in New Zealand: FMA, RBNZ and DIA Requirements

New Zealand sits under less external scrutiny than Singapore or Australia, but its domestic enforcement record tells a different story. Three supervisors — the Reserve Bank of New Zealand, the Financial Markets Authority, and the Department of Internal Affairs — run active examination programmes. A mandatory Section 59 audit every two years creates a hard compliance deadline. And the AML/CFT Act's risk-based approach means institutions cannot rely on vendor defaults or generic rule sets to satisfy supervisors.

For banks, payment service providers, and fintechs operating in New Zealand, transaction monitoring is the operational centre of AML/CFT compliance. This guide covers what the Act requires, how the supervisory structure affects monitoring obligations, and where institutions most commonly fail examination.

The AML/CFT Act 2009: New Zealand's Core Framework

New Zealand's AML/CFT framework is governed by the Anti-Money Laundering and Countering Financing of Terrorism Act 2009. Phase 1 entities — banks, non-bank deposit takers, and most financial institutions — came into scope in June 2013. Phase 2 extended obligations to lawyers, accountants, real estate agents, and other designated businesses in stages from 2018 to 2019.

The Act operates on a risk-based model. There is no prescriptive list of transaction monitoring rules an institution must run. Instead, institutions must:

- Conduct a written risk assessment that identifies their specific ML/FT risks based on customer type, product set, and delivery channels

- Implement a compliance programme derived from that assessment, including monitoring and detection controls designed to address identified risks

- Review and update the risk assessment whenever material changes occur — new products, new customer segments, new channels

This principle-based approach gives institutions flexibility but removes the ability to claim compliance by pointing to a vendor's default configuration. If your monitoring is not designed around your assessed risks, supervisors will find the gap.

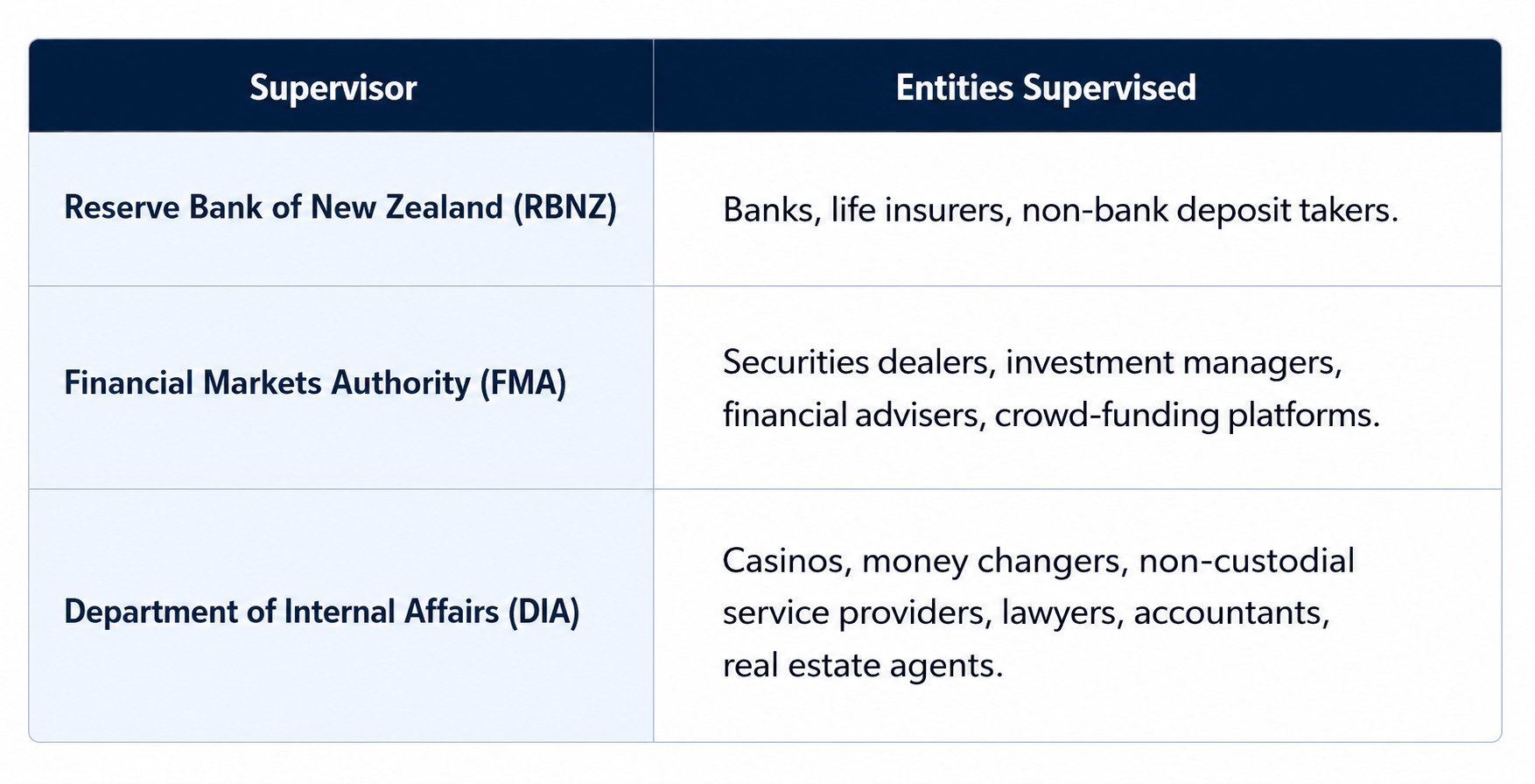

Three Supervisors: FMA, RBNZ and DIA

New Zealand's supervisory structure is unusual among APAC jurisdictions. While Australia has AUSTRAC and Singapore has MAS, New Zealand has three supervisors, each with jurisdiction over distinct entity types:

Each supervisor publishes its own guidance and runs its own examination priorities. The practical implication: guidance from AUSTRAC or MAS does not map directly onto New Zealand's framework. Institutions need to engage with their specific supervisor's published materials and annual risk focus areas.

For most banks and payment companies, RBNZ is the relevant supervisor. For digital asset businesses and VASPs, DIA is the supervisor following the 2021 amendments.

Who Must Comply

The Act applies to "reporting entities" — a defined category covering most financial businesses operating in New Zealand:

- Banks (including branches of foreign banks)

- Non-bank deposit takers: credit unions, building societies, finance companies

- Money remittance operators and foreign exchange dealers

- Life insurance companies

- Securities dealers, brokers, and investment managers

- Trustee companies

- Virtual asset service providers (VASPs) — brought in scope June 2021

The VASP inclusion is significant. The AML/CFT (Amendment) Act 2021 extended reporting entity obligations to crypto exchanges, digital asset custodians, and related businesses. DIA supervises most VASPs, with specific guidance on digital asset typologies.

Transaction Monitoring Obligations

The AML/CFT Act does not use "transaction monitoring" as a defined technical term the way MAS Notice 626 does. What it requires is that institutions implement systems and controls within their compliance programme to detect unusual and suspicious activity.

In practice, a compliant transaction monitoring function requires:

Documented risk-based detection scenarios. Monitoring rules or behavioural detection scenarios must be designed to detect the specific ML/FT risks identified in your risk assessment. A retail bank serving Pacific Island remittance customers needs different scenarios than a corporate securities dealer. Supervisors check the alignment between the risk assessment and the monitoring controls — generic vendor defaults that have not been configured to your institution's risk profile will not satisfy this requirement.

Alert investigation records. Every alert generated must be investigated, and the investigation and disposition decision must be documented. An alert closed as a false positive requires documentation of why. An alert that escalates to a SAR requires the full investigation trail. Alert backlogs — alerts generated but not reviewed — are among the most common examination findings.

Annual programme review with board sign-off. The Act requires the compliance programme, including monitoring controls, to be reviewed annually. The compliance officer must report to senior management and the board. Evidence of this reporting chain is a standard examination request.

Calibration and effectiveness review. Supervisors look for evidence that monitoring scenarios are reviewed for effectiveness — whether they are generating useful alerts or producing excessive false positives without adjustment. A monitoring programme that has not been reviewed or calibrated since deployment will attract scrutiny.

Reporting Requirements: PTRs and SARs

Transaction monitoring outputs feed two mandatory reporting obligations:

Prescribed Transaction Reports (PTRs) are threshold-based and mandatory — they do not require suspicion. PTRs must be filed with the New Zealand Police Financial Intelligence Unit (FIU) via the goAML platform for:

- Cash transactions of NZD 10,000 or more

- International wire transfers of NZD 1,000 or more (in or out)

The filing deadline is within 10 working days of the transaction. PTR monitoring requires specific detection for transactions at and around these thresholds, including structuring patterns where customers conduct multiple sub-threshold transactions to avoid PTR obligations.

Suspicious Activity Reports (SARs) — New Zealand uses "SAR" rather than "STR" (Suspicious Transaction Report). SARs must be filed as soon as practicable, and no later than three working days after forming a suspicion. The threshold for suspicion is lower than many teams assume: reasonable grounds to suspect money laundering or financing of terrorism are sufficient — certainty is not required.

SARs are filed with the NZ Police FIU via goAML. The tipping-off prohibition under the Act makes it a criminal offence to disclose to a customer that a SAR has been filed or is under consideration.

The Section 59 Audit Requirement

The most operationally distinctive element of New Zealand's framework is the Section 59 audit. Every reporting entity must arrange for an independent audit of its AML/CFT programme at intervals of no more than two years.

The auditor must assess whether:

- The risk assessment accurately reflects the entity's current ML/FT risk profile

- The compliance programme is adequate to manage those risks

- Transaction monitoring controls are functioning as designed and generating appropriate outputs

- PTR and SAR reporting is accurate, complete, and timely

- Staff training is adequate

The two-year cycle creates a hard deadline. Institutions with monitoring gaps, stale risk assessments, or unresolved findings from the previous audit cycle will face those issues again. The audit is also a forcing function for calibration: institutions that have not reviewed their detection scenarios or addressed alert backlogs before the audit will have those gaps documented in the audit report — which supervisors can and do request.

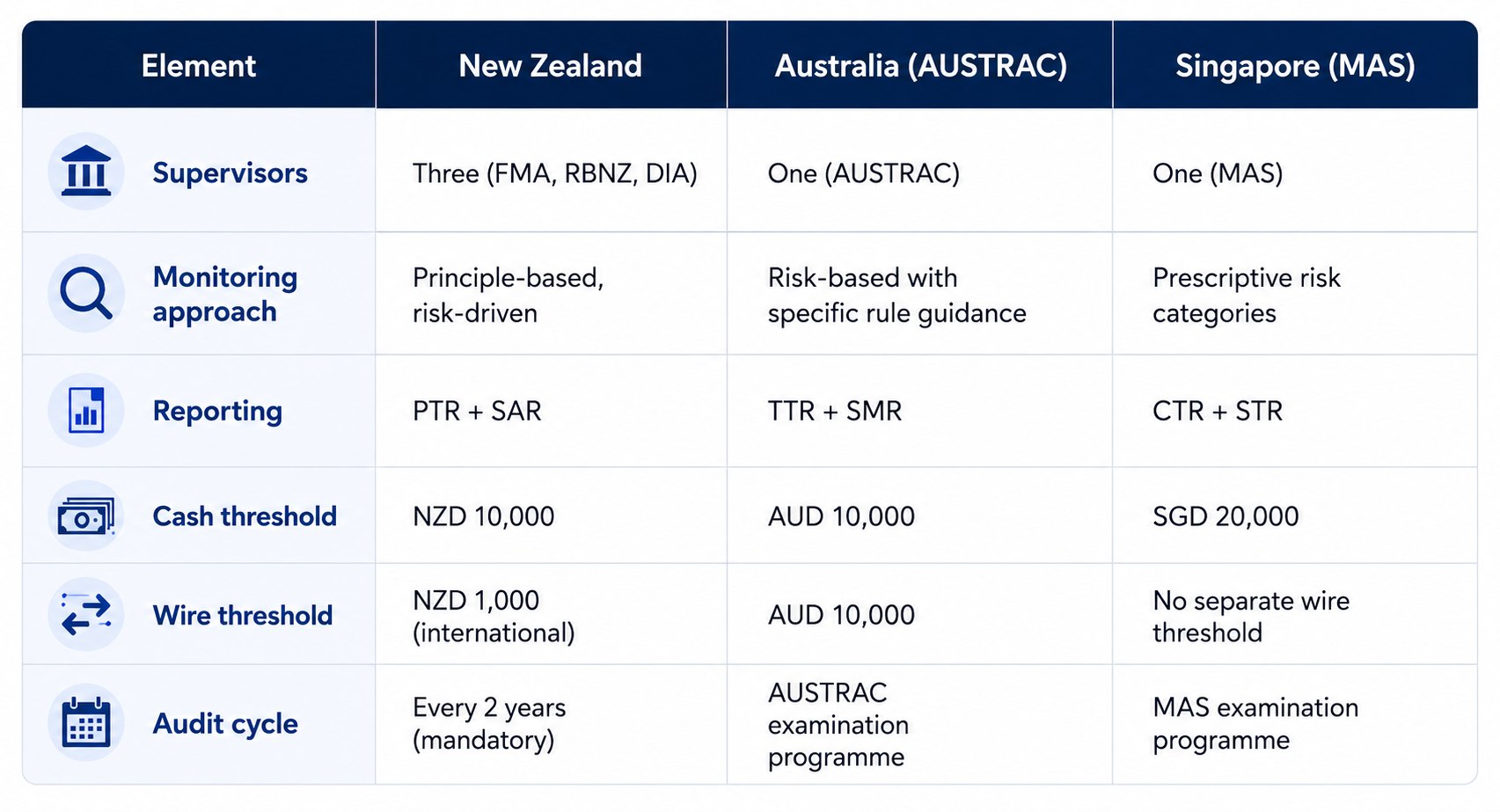

How NZ Compares to Australia and Singapore

For compliance teams managing obligations across multiple APAC jurisdictions, the structural differences matter:

The wire transfer threshold is the most operationally significant difference. New Zealand's NZD 1,000 threshold for international wires generates substantially more PTR volume than Australian or Singapore equivalents. Institutions managing cross-border payment flows into or out of New Zealand need PTR-specific monitoring that can handle this volume.

Common Transaction Monitoring Gaps in NZ Examinations

Supervisors across all three agencies have documented recurring compliance failures. The most common transaction monitoring gaps are:

Risk assessment not driving monitoring design. The risk assessment identifies high-risk customer segments or products, but the monitoring system runs generic rules that do not target those specific risks. Supervisors treat this as a material failure — the Act requires the programme to be derived from the risk assessment, not run alongside it.

PTR monitoring gaps. Institutions with strong SAR-based monitoring often have inadequate controls for PTR-triggering transactions. Structuring below the NZD 10,000 cash threshold requires specific detection scenarios that standard bank rule sets do not include.

Alert backlogs. Alerts generated but not reviewed within a reasonable timeframe are a consistent finding. Unlike some jurisdictions with prescribed investigation timelines, the Act does not specify deadlines — but supervisors expect evidence of timely review, and large backlogs indicate the monitoring system is generating more output than the team can process.

Stale risk assessments. The Act requires risk assessments to be updated when material changes occur. Institutions that have launched new products, added new customer segments, or changed delivery channels without updating their risk assessment are out of compliance with this requirement.

VASP-specific coverage gaps. For DIA-supervised VASPs, standard bank-oriented monitoring rule sets do not address digital asset typologies: wallet clustering, rapid conversion between asset types, cross-chain transfers, and structuring patterns in low-value token transactions. VASPs need detection scenarios specific to their product and customer risk profile.

What a Compliant NZ Transaction Monitoring Programme Requires

For institutions operating under the AML/CFT Act, a compliant monitoring programme requires:

- A current, documented risk assessment aligned to your actual customer base and product set

- Monitoring scenarios designed to detect the specific risks in that assessment, not vendor defaults

- Alert investigation workflows with documented disposition for every alert

- PTR-specific detection for cash and wire transactions at and around the NZD 10,000 and NZD 1,000 thresholds

- SAR workflow with a three-working-day filing deadline built into case management

- Annual programme review with board sign-off documentation

- Section 59 audit preparation: calibration review, rule effectiveness documentation, and remediation of any open findings before the audit cycle closes

For institutions evaluating whether their current monitoring system can support these requirements across New Zealand and other APAC markets, see our Transaction Monitoring Software Buyer's Guide.

The Gambling Empire: Inside Thailand’s Billion-Baht Online Betting and Money Laundering Network

In April 2026, a Thai court sentenced the son of a former senator to more than 130 years in prison in connection with a major online gambling and money laundering operation that authorities say moved billions of baht through an extensive criminal network.

At the centre of the case was not merely illegal gambling activity, but a sophisticated financial ecosystem allegedly built to process, distribute, and disguise illicit proceeds at scale.

Authorities said the operation involved online betting platforms, nominee accounts, layered fund transfers, and interconnected financial flows designed to move gambling proceeds through the financial system while obscuring the origin of funds.

For banks, fintechs, payment providers, and compliance teams, this is far more than a gambling enforcement story.

It is another example of how organised financial crime increasingly operates through structured digital ecosystems that combine:

- illicit platforms,

- mule-account networks,

- layered payments,

- and coordinated laundering infrastructure.

And increasingly, these operations are beginning to resemble legitimate digital businesses in both scale and operational sophistication.

Inside Thailand’s Alleged Online Gambling Network

According to Thai authorities, the investigation centred around an online gambling syndicate accused of operating illegal betting platforms and laundering significant volumes of illicit proceeds through interconnected financial channels.

Reports linked to the case suggest the network allegedly relied on:

- multiple bank accounts,

- nominee structures,

- rapid movement of funds,

- and layered transaction activity designed to complicate tracing efforts.

That structure matters.

Modern online gambling networks no longer function as isolated betting operations.

Instead, many operate as financially engineered ecosystems where:

- payment collection,

- account rotation,

- fund layering,

- customer acquisition,

- and laundering mechanisms

are all tightly coordinated.

The gambling platform itself often becomes only the front-facing layer of a much larger financial infrastructure.

Why Online Gambling Remains a Major AML Risk

Online gambling presents a unique challenge for financial institutions because the underlying financial activity can initially appear commercially legitimate.

High transaction volumes, rapid fund movement, and frequent customer transfers are often normal within betting environments.

That creates operational complexity for AML and fraud teams attempting to distinguish:

- legitimate gaming behaviour,

- from structured laundering activity.

Criminal networks exploit this ambiguity.

Funds can be:

- deposited,

- redistributed across multiple accounts,

- cycled through betting activity,

- withdrawn,

- and transferred again across payment rails

within relatively short periods of time.

This creates an ideal environment for:

- layering,

- transaction fragmentation,

- and obscuring beneficial ownership.

And increasingly, digital payment ecosystems allow this movement to happen at scale.

The Role of Mule Accounts and Nominee Structures

No large-scale online gambling operation can effectively move illicit proceeds without access to account infrastructure.

The Thailand case highlights the critical role of:

- mule accounts,

- nominee account holders,

- and intermediary payment channels.

Authorities allege the network used multiple accounts to receive and redistribute gambling proceeds, helping distance the organisers from the underlying transactions.

These accounts may belong to:

- recruited individuals,

- account renters,

- synthetic identities,

- or nominees acting on behalf of criminal operators.

Their role is operationally simple but strategically important:

receive funds, move them rapidly, and reduce visibility into the true controllers behind the network.

For financial institutions, this creates a major detection challenge because individual transactions may appear ordinary when viewed in isolation.

But collectively, the patterns may indicate coordinated laundering behaviour.

The Industrialisation of Gambling-Linked Financial Crime

One of the most important lessons from this case is that organised online gambling is becoming increasingly industrialised.

This is no longer simply a matter of illegal betting websites collecting wagers.

Modern gambling-linked financial crime networks increasingly resemble structured digital enterprises with:

- payment workflows,

- operational hierarchies,

- customer acquisition systems,

- layered account ecosystems,

- and dedicated laundering mechanisms.

That evolution changes the scale of risk.

Instead of isolated illicit transactions, financial institutions are now confronting criminal systems capable of processing large volumes of funds through interconnected digital channels.

And because many of these flows occur through legitimate banking infrastructure, detection becomes significantly more difficult.

Why Traditional Detection Models Struggle

One of the biggest operational problems in gambling-linked laundering is that many suspicious activities closely resemble normal transactional behaviour.

For example:

- rapid deposits and withdrawals,

- frequent transfers between accounts,

- high transaction velocity,

- and fragmented payments

may all occur legitimately within digital gaming environments.

This creates substantial noise for compliance teams.

Traditional rules-based monitoring systems often struggle because:

- thresholds may not be breached,

- transaction values may appear routine,

- and individual accounts may initially show limited risk indicators.

The suspicious behaviour often becomes visible only when viewed collectively across:

- multiple accounts,

- devices,

- counterparties,

- transaction patterns,

- and behavioural relationships.

Increasingly, organised financial crime detection is becoming less about isolated alerts and more about understanding networks.

The Convergence of Gambling, Fraud, and Money Laundering

The Thailand case also reinforces a broader regional trend:

the convergence of multiple financial crime categories within the same ecosystem.

Online gambling networks today may overlap with:

- mule-account recruitment,

- cyber-enabled scams,

- organised fraud,

- illicit payment processing,

- and cross-border laundering activity.

This convergence matters because criminal organisations rarely specialise narrowly anymore.

The same infrastructure used to process gambling proceeds may also support:

- scam-related fund movement,

- account abuse,

- identity fraud,

- or broader organised criminal activity.

For financial institutions, separating these risks into isolated categories can create dangerous blind spots.

The financial flows are increasingly interconnected.

Detection strategies must evolve accordingly.

What Financial Institutions Should Monitor

Cases like this highlight several important behavioural and transactional indicators institutions should monitor more closely.

Rapid pass-through activity

Accounts receiving and quickly redistributing funds across multiple beneficiaries.

Clusters of interconnected accounts

Multiple accounts sharing behavioural similarities, counterparties, devices, or transaction structures.

High-volume low-value transfers

Repeated fragmented payments designed to avoid scrutiny while moving significant aggregate value.

Frequent account rotation

Beneficiary accounts changing rapidly within short timeframes.

Unusual payment velocity

Transaction behaviour inconsistent with expected customer profiles.

Links between gambling-related transactions and broader suspicious activity

Connections between betting-related flows and potential scam, fraud, or mule-account indicators.

Individually, these signals may appear weak.

Together, they can reveal coordinated laundering ecosystems.

Why Financial Institutions Need More Connected Intelligence

The Thailand gambling case highlights why static AML controls are increasingly insufficient against organised digital financial crime.

Modern criminal ecosystems evolve quickly:

- payment channels change,

- laundering routes shift,

- mule structures rotate,

- and digital platforms adapt constantly.

This creates operational pressure on institutions still relying heavily on:

- isolated transaction monitoring,

- static rules,

- manual investigations,

- and fragmented fraud-AML workflows.

What institutions increasingly need is:

- behavioural intelligence,

- network visibility,

- typology-driven monitoring,

- and the ability to connect signals across fraud and AML environments simultaneously.

That is especially important in gambling-linked laundering because the suspicious behaviour often emerges gradually through relationships and coordinated movement rather than single anomalous transactions.

How Technology Can Help Detect Organised Gambling Networks

Advanced AML and fraud platforms are becoming increasingly important in identifying complex laundering ecosystems linked to online gambling.

Modern detection approaches combine:

- behavioural analytics,

- network intelligence,

- entity resolution,

- and typology-driven detection models

to uncover hidden relationships within financial activity.

Platforms such as Tookitaki’s FinCense help institutions move beyond isolated transaction monitoring by combining:

- AML and fraud convergence,

- behavioural monitoring,

- collaborative intelligence through the AFC Ecosystem,

- and network-based detection approaches.

In scenarios involving gambling-linked laundering, this allows institutions to identify:

- mule-account behaviour,

- suspicious account clusters,

- layered payment structures,

- and coordinated fund movement patterns

earlier and with greater operational context.

That visibility becomes critical when criminal ecosystems are specifically designed to appear operationally normal on the surface.

How Tookitaki Helps Institutions Detect Gambling-Linked Laundering Networks

Cases like the Thailand gambling investigation demonstrate why financial institutions increasingly need a more connected and intelligence-driven approach to financial crime detection.

Traditional monitoring systems are often designed to review transactions in isolation. But organised gambling-linked laundering networks operate across:

- multiple accounts,

- payment rails,

- beneficiary relationships,

- mule structures,

- and layered transaction ecosystems simultaneously.

This makes fragmented detection increasingly ineffective.

Tookitaki’s FinCense platform helps financial institutions strengthen detection capabilities by combining:

- AML and fraud convergence,

- behavioural intelligence,

- network-based risk detection,

- and collaborative typology insights through the AFC Ecosystem.

In gambling-linked laundering scenarios, this allows institutions to identify:

- suspicious account clusters,

- rapid pass-through activity,

- mule-account behaviour,

- layered payment movement,

- and hidden relationships across customers and counterparties

more effectively and earlier in the risk lifecycle.

The AFC Ecosystem further strengthens this approach by enabling institutions to leverage continuously evolving typologies and real-world financial crime intelligence contributed by compliance and AML experts globally.

As organised financial crime becomes more interconnected and operationally sophisticated, institutions increasingly need detection systems capable of understanding not just transactions, but the broader ecosystems operating behind them.

The Bigger Picture: Online Gambling as Financial Infrastructure Abuse

The Thailand case reflects a broader regional and global shift in how organised crime uses digital infrastructure.

Online gambling platforms are increasingly functioning not merely as illicit entertainment channels, but as financial movement ecosystems capable of:

- processing large transaction volumes,

- redistributing illicit funds,

- and integrating criminal proceeds into the legitimate economy.

That distinction matters.

Because the challenge for financial institutions is no longer simply identifying illegal gambling transactions.

It is understanding how legitimate financial systems can be systematically exploited to support broader criminal operations.

And increasingly, those operations are designed to blend into normal digital financial activity.

Final Thoughts

The massive online gambling and money laundering case uncovered in Thailand offers another clear reminder that organised financial crime is becoming more digital, more structured, and more operationally sophisticated.

What appears outwardly as illegal betting activity may actually involve:

- coordinated laundering infrastructure,

- mule-account ecosystems,

- layered financial movement,

- nominee structures,

- and highly organised criminal coordination operating behind the scenes.

For financial institutions, this creates a difficult but increasingly important challenge.

The future of financial crime prevention will depend less on identifying isolated suspicious transactions and more on understanding hidden financial relationships, behavioural coordination, and evolving laundering typologies across interconnected payment ecosystems.

Because increasingly, organised financial crime does not look chaotic.

It looks operationally efficient.

KYC Requirements in Singapore: MAS CDD Rules for Banks and Payment Companies

Singapore's KYC framework is more specific — and more enforced — than most compliance teams from outside the region expect. The Monetary Authority of Singapore does not publish voluntary guidelines on customer due diligence. It issues Notices: binding legal instruments with criminal penalties for non-compliance. For banks, MAS Notice 626 sets the requirements. For payment service providers licensed under the Payment Services Act, MAS Notice PSN01 and PSN02 apply.

This guide covers what MAS requires for customer identification and verification, the three tiers of CDD Singapore institutions must apply, beneficial ownership obligations, enhanced due diligence triggers, and the recurring gaps MAS examiners find in KYC programmes.

The Regulatory Foundation: MAS Notice 626 and PSN01/PSN02

MAS Notice 626 applies to banks and merchant banks. It sets out prescriptive requirements for:

- Customer due diligence (CDD) — when to perform it, what it must cover, and how to document it

- Enhanced due diligence (EDD) — specific triggers and minimum requirements

- Simplified due diligence (SDD) — the limited circumstances where reduced CDD applies

- Ongoing monitoring of business relationships

- Record keeping

- Suspicious transaction reporting

MAS Notice PSN01 (for standard payment licensees) and MAS Notice PSN02 (for major payment institutions) under the Payment Services Act 2019 set equivalent obligations for payment companies, e-wallets, and remittance operators. The CDD framework in PSN01/PSN02 mirrors the structure of Notice 626 but calibrated to payment service business models — including specific requirements for transaction monitoring on payment flows, cross-border transfers, and digital token services.

Both Notices are regularly updated. Institutions should refer to the current MAS website versions rather than archived copies — amendments following Singapore's 2024 National Risk Assessment update guidance on beneficial ownership verification and higher-risk customer categories.

When CDD Must Be Performed

MAS Notice 626 specifies four triggers requiring CDD to be completed before proceeding:

- Establishing a business relationship — KYC must be completed before onboarding any customer into an ongoing relationship

- Occasional transactions of SGD 5,000 or more — one-off transactions at or above this threshold require CDD even without an ongoing relationship

- Wire transfers of any amount — all wire transfers require CDD, with no minimum threshold

- Suspicion of money laundering or terrorism financing — CDD is required regardless of transaction value or customer type when suspicion arises

The inability to complete CDD to the required standard is grounds for declining to onboard a customer or for terminating an existing business relationship. MAS examiners check that institutions apply this requirement in practice, not just in policy.

Three Tiers of CDD in Singapore

Singapore's CDD framework has three levels, applied based on the customer's assessed risk:

Simplified Due Diligence (SDD)

SDD may be applied — with documented justification — for a limited category of lower-risk customers:

- Singapore government entities and statutory boards

- Companies listed on the Singapore Exchange (SGX) or other approved exchanges

- Regulated financial institutions supervised by MAS or equivalent foreign supervisors

- Certain low-risk products (e.g., basic savings accounts with strict usage limits)

SDD does not mean no due diligence. It means reduced documentation requirements — but institutions must document why SDD applies and maintain that justification in the customer file. MAS does not permit SDD to be applied as a default for corporate customers without case-by-case assessment.

Standard CDD

Standard CDD is the baseline requirement for all other customers. It requires:

- Customer identification: Full legal name, identification document type and number, date of birth (individuals), place of incorporation (entities)

- Verification: Identity documents verified against reliable, independent sources — passports, NRIC, ACRA business registration, corporate documentation

- Beneficial owner identification: For legal entities, identify and verify the natural persons who ultimately own or control the entity (see below for the 25% threshold)

- Purpose and intended nature of the business relationship documented

- Ongoing monitoring of the relationship for consistency with the customer's profile

Enhanced Due Diligence (EDD)

EDD applies to higher-risk customers and situations. MAS Notice 626 specifies mandatory EDD triggers:

- Politically Exposed Persons (PEPs): Foreign PEPs require EDD as a minimum. Domestic PEPs are subject to risk-based assessment. PEP status extends to family members and close associates. Senior management approval is required before establishing or continuing a relationship with a PEP. EDD for PEPs must include source of wealth and source of funds verification — not just identification.

- Correspondent banking relationships: Respondent institution KYC, assessment of AML/CFT controls, and senior management approval before establishing the relationship

- High-risk jurisdictions: Customers or transaction counterparties connected to FATF grey-listed or black-listed countries require EDD and additional scrutiny

- Complex or unusual transactions: Transactions with no apparent economic or legal purpose, or that are inconsistent with the customer's known profile, require EDD investigation before proceeding

- Cross-border private banking: Non-face-to-face account opening for high-net-worth clients from outside Singapore requires additional verification steps

EDD is not satisfied by collecting more documents. MAS examiners look for evidence that the additional information gathered was actually used in the risk assessment — source of wealth narratives that are vague or unsubstantiated are treated as inadequate EDD, not as EDD completed.

Beneficial Owner Verification

Identifying and verifying beneficial owners is one of the most examined areas of Singapore's KYC framework. MAS Notice 626 requires institutions to identify the natural persons who ultimately own or control a legal entity customer.

The threshold is 25% shareholding or voting rights — any natural person who holds, directly or indirectly, 25% or more of a company's shares or voting rights must be identified and verified. Where no natural person holds 25% or more, the institution must identify the natural persons who exercise control through other means — typically senior management.

For layered corporate structures — where ownership runs through multiple holding companies across different jurisdictions — institutions must look through the structure to identify the ultimate beneficial owner. MAS examiners consistently flag beneficial ownership documentation failures as a top finding in corporate customer reviews. Accepting a company registration document without looking through the ownership chain does not satisfy this requirement.

Trusts and other non-corporate legal arrangements require identification of settlors, trustees, and beneficiaries with 25% or greater beneficial interest.

Digital Onboarding and MyInfo

Singapore's national digital identity infrastructure supports MAS-compliant digital onboarding. MyInfo, operated by the Government Technology Agency (GovTech), provides verified personal data — NRIC details, address, employment, and other government-held data — that institutions can retrieve with customer consent.

MAS has confirmed that MyInfo retrieval is acceptable for identity verification purposes, reducing the documentation burden for individual customers. Institutions using MyInfo for onboarding must document the verification method and maintain records of the MyInfo retrieval.

For corporate customers, ACRA's Bizfile registry provides business registration and officer information that can be used for entity verification. Beneficial ownership still requires independent verification — Bizfile shows registered shareholders but does not always reflect ultimate beneficial ownership through nominee structures.

Ongoing Monitoring and Periodic Review

KYC is not a one-time onboarding requirement. MAS Notice 626 requires ongoing monitoring of established business relationships to ensure that transactions remain consistent with the institution's knowledge of the customer.

This has two components:

Transaction monitoring — detecting transactions inconsistent with the customer's business profile, source of funds, or expected transaction patterns. For the transaction monitoring requirements that feed into this ongoing CDD obligation, see our MAS Notice 626 guide.

Periodic CDD review — customer records must be reviewed and updated at intervals appropriate to the customer's risk rating. High-risk customers require more frequent review. The review must check whether the customer's profile has changed, whether beneficial ownership has changed, and whether the risk rating remains appropriate.

The trigger for an out-of-cycle CDD review includes: material changes in transaction patterns, adverse media, connection to a person or entity of concern, and changes in beneficial ownership.

Record-Keeping Requirements

MAS Notice 626 requires institutions to retain CDD records for five years from the end of the business relationship, or five years from the date of the transaction for one-off customers. Records must be maintained in a form that allows reconstruction of individual transactions and can be produced promptly in response to an MAS request or court order.

The five-year clock runs from the end of the relationship — not from when the records were created. For long-term customers, this means maintaining KYC documentation, transaction records, SAR-related records, and correspondence for the full relationship period plus five years.

Suspicious Transaction Reporting

Singapore uses Suspicious Transaction Reports (STRs) filed with the Suspicious Transaction Reporting Office (STRO), administered by the Singapore Police Force. There is no minimum transaction threshold — any transaction, regardless of amount, that raises suspicion must be reported.

STRs must be filed as soon as practicable after suspicion is formed. The Act does not set a specific deadline in days, but MAS examiners and STRO guidance indicate that delays of more than a few business days without documented justification will attract scrutiny.

The tipping-off prohibition under the Corruption, Drug Trafficking and Other Serious Crimes (CDSA) Act makes it a criminal offence to disclose to a customer that an STR has been filed or is under consideration.

For cash transactions of SGD 20,000 or more, institutions must file a Cash Transaction Report (CTR) regardless of suspicion. CTRs are filed with STRO within 15 business days.

Common KYC Failures in MAS Examinations

MAS's examination findings and industry guidance consistently flag the same recurring gaps:

Beneficial ownership not traced to ultimate natural persons. Institutions stop at the first layer of corporate ownership without looking through nominee shareholders or holding company structures to identify the actual controlling individuals.

EDD documentation without substantive assessment. Files contain EDD documents — source of wealth declarations, bank statements, company accounts — but no evidence that the documents were reviewed, assessed, or used to update the risk rating.

PEP definitions applied too narrowly. Institutions identify foreign government ministers as PEPs but miss domestic senior officials, senior executives of state-owned enterprises, and immediate family members of identified PEPs.

Static customer profiles. CDD completed at onboarding is never updated. Customers whose transaction patterns have changed significantly since onboarding retain their original risk rating without periodic review.

MyInfo used as a complete KYC solution. MyInfo satisfies identity verification for individuals but does not substitute for source of funds verification, purpose of relationship documentation, or beneficial ownership checks on corporate structures.

STR delays. Suspicion forms during transaction review but is not escalated or filed for days or weeks. Case management systems without deadline tracking are the most common operational cause.

For Singapore institutions evaluating whether their current KYC and monitoring systems can meet these requirements, see our Transaction Monitoring Software Buyer's Guide for a full framework covering the capabilities MAS-regulated institutions need.

Transaction Monitoring in New Zealand: FMA, RBNZ and DIA Requirements

New Zealand sits under less external scrutiny than Singapore or Australia, but its domestic enforcement record tells a different story. Three supervisors — the Reserve Bank of New Zealand, the Financial Markets Authority, and the Department of Internal Affairs — run active examination programmes. A mandatory Section 59 audit every two years creates a hard compliance deadline. And the AML/CFT Act's risk-based approach means institutions cannot rely on vendor defaults or generic rule sets to satisfy supervisors.

For banks, payment service providers, and fintechs operating in New Zealand, transaction monitoring is the operational centre of AML/CFT compliance. This guide covers what the Act requires, how the supervisory structure affects monitoring obligations, and where institutions most commonly fail examination.

The AML/CFT Act 2009: New Zealand's Core Framework

New Zealand's AML/CFT framework is governed by the Anti-Money Laundering and Countering Financing of Terrorism Act 2009. Phase 1 entities — banks, non-bank deposit takers, and most financial institutions — came into scope in June 2013. Phase 2 extended obligations to lawyers, accountants, real estate agents, and other designated businesses in stages from 2018 to 2019.

The Act operates on a risk-based model. There is no prescriptive list of transaction monitoring rules an institution must run. Instead, institutions must:

- Conduct a written risk assessment that identifies their specific ML/FT risks based on customer type, product set, and delivery channels

- Implement a compliance programme derived from that assessment, including monitoring and detection controls designed to address identified risks

- Review and update the risk assessment whenever material changes occur — new products, new customer segments, new channels

This principle-based approach gives institutions flexibility but removes the ability to claim compliance by pointing to a vendor's default configuration. If your monitoring is not designed around your assessed risks, supervisors will find the gap.

Three Supervisors: FMA, RBNZ and DIA

New Zealand's supervisory structure is unusual among APAC jurisdictions. While Australia has AUSTRAC and Singapore has MAS, New Zealand has three supervisors, each with jurisdiction over distinct entity types:

Each supervisor publishes its own guidance and runs its own examination priorities. The practical implication: guidance from AUSTRAC or MAS does not map directly onto New Zealand's framework. Institutions need to engage with their specific supervisor's published materials and annual risk focus areas.

For most banks and payment companies, RBNZ is the relevant supervisor. For digital asset businesses and VASPs, DIA is the supervisor following the 2021 amendments.

Who Must Comply

The Act applies to "reporting entities" — a defined category covering most financial businesses operating in New Zealand:

- Banks (including branches of foreign banks)

- Non-bank deposit takers: credit unions, building societies, finance companies

- Money remittance operators and foreign exchange dealers

- Life insurance companies

- Securities dealers, brokers, and investment managers

- Trustee companies

- Virtual asset service providers (VASPs) — brought in scope June 2021

The VASP inclusion is significant. The AML/CFT (Amendment) Act 2021 extended reporting entity obligations to crypto exchanges, digital asset custodians, and related businesses. DIA supervises most VASPs, with specific guidance on digital asset typologies.

Transaction Monitoring Obligations

The AML/CFT Act does not use "transaction monitoring" as a defined technical term the way MAS Notice 626 does. What it requires is that institutions implement systems and controls within their compliance programme to detect unusual and suspicious activity.

In practice, a compliant transaction monitoring function requires:

Documented risk-based detection scenarios. Monitoring rules or behavioural detection scenarios must be designed to detect the specific ML/FT risks identified in your risk assessment. A retail bank serving Pacific Island remittance customers needs different scenarios than a corporate securities dealer. Supervisors check the alignment between the risk assessment and the monitoring controls — generic vendor defaults that have not been configured to your institution's risk profile will not satisfy this requirement.

Alert investigation records. Every alert generated must be investigated, and the investigation and disposition decision must be documented. An alert closed as a false positive requires documentation of why. An alert that escalates to a SAR requires the full investigation trail. Alert backlogs — alerts generated but not reviewed — are among the most common examination findings.

Annual programme review with board sign-off. The Act requires the compliance programme, including monitoring controls, to be reviewed annually. The compliance officer must report to senior management and the board. Evidence of this reporting chain is a standard examination request.

Calibration and effectiveness review. Supervisors look for evidence that monitoring scenarios are reviewed for effectiveness — whether they are generating useful alerts or producing excessive false positives without adjustment. A monitoring programme that has not been reviewed or calibrated since deployment will attract scrutiny.

Reporting Requirements: PTRs and SARs

Transaction monitoring outputs feed two mandatory reporting obligations:

Prescribed Transaction Reports (PTRs) are threshold-based and mandatory — they do not require suspicion. PTRs must be filed with the New Zealand Police Financial Intelligence Unit (FIU) via the goAML platform for:

- Cash transactions of NZD 10,000 or more

- International wire transfers of NZD 1,000 or more (in or out)

The filing deadline is within 10 working days of the transaction. PTR monitoring requires specific detection for transactions at and around these thresholds, including structuring patterns where customers conduct multiple sub-threshold transactions to avoid PTR obligations.

Suspicious Activity Reports (SARs) — New Zealand uses "SAR" rather than "STR" (Suspicious Transaction Report). SARs must be filed as soon as practicable, and no later than three working days after forming a suspicion. The threshold for suspicion is lower than many teams assume: reasonable grounds to suspect money laundering or financing of terrorism are sufficient — certainty is not required.

SARs are filed with the NZ Police FIU via goAML. The tipping-off prohibition under the Act makes it a criminal offence to disclose to a customer that a SAR has been filed or is under consideration.

The Section 59 Audit Requirement

The most operationally distinctive element of New Zealand's framework is the Section 59 audit. Every reporting entity must arrange for an independent audit of its AML/CFT programme at intervals of no more than two years.

The auditor must assess whether:

- The risk assessment accurately reflects the entity's current ML/FT risk profile

- The compliance programme is adequate to manage those risks

- Transaction monitoring controls are functioning as designed and generating appropriate outputs

- PTR and SAR reporting is accurate, complete, and timely

- Staff training is adequate

The two-year cycle creates a hard deadline. Institutions with monitoring gaps, stale risk assessments, or unresolved findings from the previous audit cycle will face those issues again. The audit is also a forcing function for calibration: institutions that have not reviewed their detection scenarios or addressed alert backlogs before the audit will have those gaps documented in the audit report — which supervisors can and do request.

How NZ Compares to Australia and Singapore

For compliance teams managing obligations across multiple APAC jurisdictions, the structural differences matter:

The wire transfer threshold is the most operationally significant difference. New Zealand's NZD 1,000 threshold for international wires generates substantially more PTR volume than Australian or Singapore equivalents. Institutions managing cross-border payment flows into or out of New Zealand need PTR-specific monitoring that can handle this volume.

Common Transaction Monitoring Gaps in NZ Examinations

Supervisors across all three agencies have documented recurring compliance failures. The most common transaction monitoring gaps are:

Risk assessment not driving monitoring design. The risk assessment identifies high-risk customer segments or products, but the monitoring system runs generic rules that do not target those specific risks. Supervisors treat this as a material failure — the Act requires the programme to be derived from the risk assessment, not run alongside it.

PTR monitoring gaps. Institutions with strong SAR-based monitoring often have inadequate controls for PTR-triggering transactions. Structuring below the NZD 10,000 cash threshold requires specific detection scenarios that standard bank rule sets do not include.

Alert backlogs. Alerts generated but not reviewed within a reasonable timeframe are a consistent finding. Unlike some jurisdictions with prescribed investigation timelines, the Act does not specify deadlines — but supervisors expect evidence of timely review, and large backlogs indicate the monitoring system is generating more output than the team can process.

Stale risk assessments. The Act requires risk assessments to be updated when material changes occur. Institutions that have launched new products, added new customer segments, or changed delivery channels without updating their risk assessment are out of compliance with this requirement.

VASP-specific coverage gaps. For DIA-supervised VASPs, standard bank-oriented monitoring rule sets do not address digital asset typologies: wallet clustering, rapid conversion between asset types, cross-chain transfers, and structuring patterns in low-value token transactions. VASPs need detection scenarios specific to their product and customer risk profile.

What a Compliant NZ Transaction Monitoring Programme Requires

For institutions operating under the AML/CFT Act, a compliant monitoring programme requires:

- A current, documented risk assessment aligned to your actual customer base and product set

- Monitoring scenarios designed to detect the specific risks in that assessment, not vendor defaults

- Alert investigation workflows with documented disposition for every alert

- PTR-specific detection for cash and wire transactions at and around the NZD 10,000 and NZD 1,000 thresholds

- SAR workflow with a three-working-day filing deadline built into case management

- Annual programme review with board sign-off documentation

- Section 59 audit preparation: calibration review, rule effectiveness documentation, and remediation of any open findings before the audit cycle closes

For institutions evaluating whether their current monitoring system can support these requirements across New Zealand and other APAC markets, see our Transaction Monitoring Software Buyer's Guide.

The Gambling Empire: Inside Thailand’s Billion-Baht Online Betting and Money Laundering Network

In April 2026, a Thai court sentenced the son of a former senator to more than 130 years in prison in connection with a major online gambling and money laundering operation that authorities say moved billions of baht through an extensive criminal network.

At the centre of the case was not merely illegal gambling activity, but a sophisticated financial ecosystem allegedly built to process, distribute, and disguise illicit proceeds at scale.

Authorities said the operation involved online betting platforms, nominee accounts, layered fund transfers, and interconnected financial flows designed to move gambling proceeds through the financial system while obscuring the origin of funds.

For banks, fintechs, payment providers, and compliance teams, this is far more than a gambling enforcement story.

It is another example of how organised financial crime increasingly operates through structured digital ecosystems that combine:

- illicit platforms,

- mule-account networks,

- layered payments,

- and coordinated laundering infrastructure.

And increasingly, these operations are beginning to resemble legitimate digital businesses in both scale and operational sophistication.

Inside Thailand’s Alleged Online Gambling Network

According to Thai authorities, the investigation centred around an online gambling syndicate accused of operating illegal betting platforms and laundering significant volumes of illicit proceeds through interconnected financial channels.

Reports linked to the case suggest the network allegedly relied on:

- multiple bank accounts,

- nominee structures,

- rapid movement of funds,

- and layered transaction activity designed to complicate tracing efforts.

That structure matters.

Modern online gambling networks no longer function as isolated betting operations.

Instead, many operate as financially engineered ecosystems where:

- payment collection,

- account rotation,

- fund layering,

- customer acquisition,

- and laundering mechanisms

are all tightly coordinated.

The gambling platform itself often becomes only the front-facing layer of a much larger financial infrastructure.

Why Online Gambling Remains a Major AML Risk

Online gambling presents a unique challenge for financial institutions because the underlying financial activity can initially appear commercially legitimate.

High transaction volumes, rapid fund movement, and frequent customer transfers are often normal within betting environments.

That creates operational complexity for AML and fraud teams attempting to distinguish:

- legitimate gaming behaviour,

- from structured laundering activity.

Criminal networks exploit this ambiguity.

Funds can be:

- deposited,

- redistributed across multiple accounts,

- cycled through betting activity,

- withdrawn,

- and transferred again across payment rails

within relatively short periods of time.

This creates an ideal environment for:

- layering,

- transaction fragmentation,

- and obscuring beneficial ownership.

And increasingly, digital payment ecosystems allow this movement to happen at scale.

The Role of Mule Accounts and Nominee Structures

No large-scale online gambling operation can effectively move illicit proceeds without access to account infrastructure.

The Thailand case highlights the critical role of:

- mule accounts,

- nominee account holders,

- and intermediary payment channels.

Authorities allege the network used multiple accounts to receive and redistribute gambling proceeds, helping distance the organisers from the underlying transactions.

These accounts may belong to:

- recruited individuals,

- account renters,

- synthetic identities,

- or nominees acting on behalf of criminal operators.

Their role is operationally simple but strategically important:

receive funds, move them rapidly, and reduce visibility into the true controllers behind the network.

For financial institutions, this creates a major detection challenge because individual transactions may appear ordinary when viewed in isolation.

But collectively, the patterns may indicate coordinated laundering behaviour.

The Industrialisation of Gambling-Linked Financial Crime

One of the most important lessons from this case is that organised online gambling is becoming increasingly industrialised.

This is no longer simply a matter of illegal betting websites collecting wagers.

Modern gambling-linked financial crime networks increasingly resemble structured digital enterprises with:

- payment workflows,

- operational hierarchies,

- customer acquisition systems,

- layered account ecosystems,

- and dedicated laundering mechanisms.

That evolution changes the scale of risk.

Instead of isolated illicit transactions, financial institutions are now confronting criminal systems capable of processing large volumes of funds through interconnected digital channels.

And because many of these flows occur through legitimate banking infrastructure, detection becomes significantly more difficult.

Why Traditional Detection Models Struggle

One of the biggest operational problems in gambling-linked laundering is that many suspicious activities closely resemble normal transactional behaviour.

For example:

- rapid deposits and withdrawals,

- frequent transfers between accounts,

- high transaction velocity,

- and fragmented payments

may all occur legitimately within digital gaming environments.

This creates substantial noise for compliance teams.

Traditional rules-based monitoring systems often struggle because:

- thresholds may not be breached,

- transaction values may appear routine,

- and individual accounts may initially show limited risk indicators.

The suspicious behaviour often becomes visible only when viewed collectively across:

- multiple accounts,

- devices,

- counterparties,

- transaction patterns,

- and behavioural relationships.

Increasingly, organised financial crime detection is becoming less about isolated alerts and more about understanding networks.

The Convergence of Gambling, Fraud, and Money Laundering

The Thailand case also reinforces a broader regional trend:

the convergence of multiple financial crime categories within the same ecosystem.

Online gambling networks today may overlap with:

- mule-account recruitment,

- cyber-enabled scams,

- organised fraud,

- illicit payment processing,

- and cross-border laundering activity.

This convergence matters because criminal organisations rarely specialise narrowly anymore.

The same infrastructure used to process gambling proceeds may also support:

- scam-related fund movement,

- account abuse,

- identity fraud,

- or broader organised criminal activity.

For financial institutions, separating these risks into isolated categories can create dangerous blind spots.

The financial flows are increasingly interconnected.

Detection strategies must evolve accordingly.

What Financial Institutions Should Monitor

Cases like this highlight several important behavioural and transactional indicators institutions should monitor more closely.

Rapid pass-through activity

Accounts receiving and quickly redistributing funds across multiple beneficiaries.

Clusters of interconnected accounts

Multiple accounts sharing behavioural similarities, counterparties, devices, or transaction structures.

High-volume low-value transfers

Repeated fragmented payments designed to avoid scrutiny while moving significant aggregate value.

Frequent account rotation

Beneficiary accounts changing rapidly within short timeframes.

Unusual payment velocity

Transaction behaviour inconsistent with expected customer profiles.

Links between gambling-related transactions and broader suspicious activity