Money Laundering Risks in Malaysia: How to Protect Your Business

.svg)

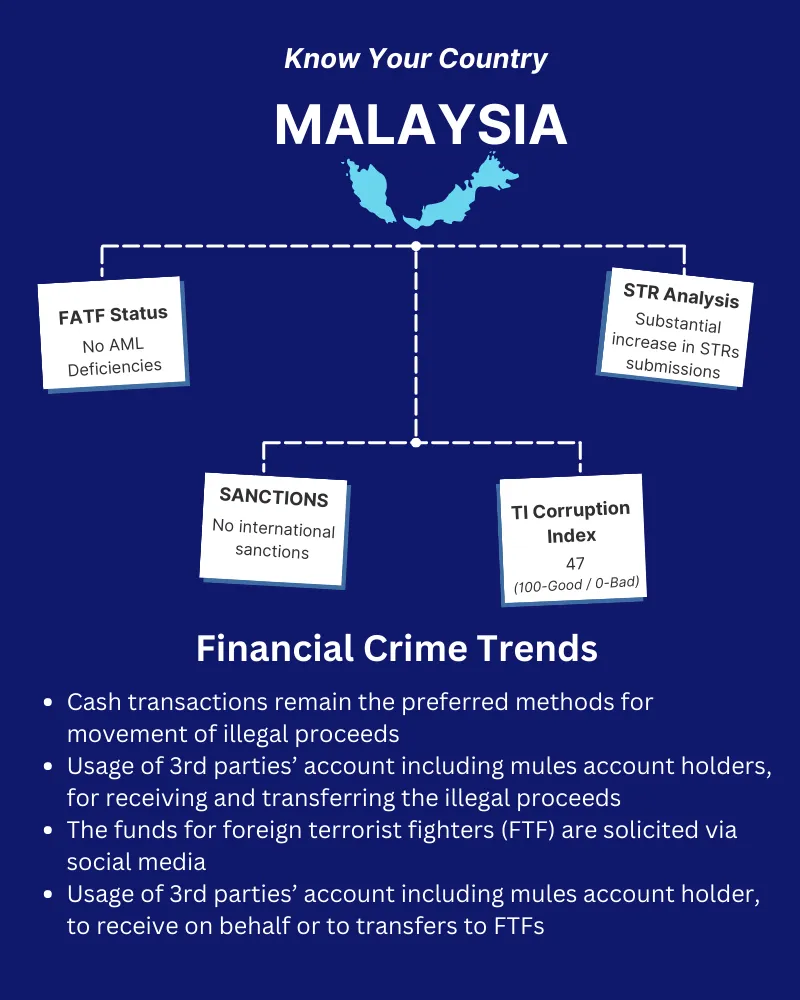

Money laundering risks in Malaysia are evolving and businesses can no longer afford to ignore them.

Malaysia’s growing economy, strategic geographic position, and increasing digitalisation have made it a prime target for financial crime. From the infamous 1MDB scandal to the Genneva Malaysia gold scheme, the country has witnessed several high-profile cases that have exposed deep vulnerabilities in its financial ecosystem.

These incidents have triggered stronger regulatory reforms—but the threat persists. Money laundering risks in Malaysia continue to pose serious challenges for businesses, financial institutions, and regulators alike. Beyond legal consequences, involvement in money laundering—whether intentional or not—can lead to financial penalties, reputational damage, and loss of operating licences.

This article explores the key drivers of money laundering in Malaysia, recent trends, and what businesses can do to strengthen their AML defences. By understanding the risks and responding proactively, organisations can not only remain compliant, but also play a vital role in safeguarding the nation’s financial integrity.

Understanding Money Laundering Risks in Malaysia

Common methods of money laundering

Money laundering in Malaysia typically involves various techniques designed to obscure the illegal origin of funds, making them appear legitimate. Some common methods used by criminals include:

- Layering: This involves moving funds through multiple transactions and accounts to create a complex trail that is difficult to trace. Criminals may use shell companies, offshore accounts, and multiple financial institutions to accomplish this.

- Smurfing: In this technique, large amounts of illicit funds are broken down into smaller transactions to avoid detection by financial institutions and regulatory authorities. Smurfing can involve cash deposits, wire transfers, or even the purchase and sale of high-value assets.

- Trade-based money laundering: Criminals may use trade transactions to launder money by over- or under-invoicing goods and services or using complex trade financing arrangements. This method allows them to move funds across borders and legitimize the proceeds of crime.

Key industries at risk

Certain industries in Malaysia are particularly susceptible to money laundering due to their nature or business practices. Some of these high-risk sectors include:

- Financial services: Banks, money service businesses, and other financial institutions are often targeted by money launderers because of the large volume of transactions they handle daily.

- Real estate: The high-value nature of property transactions makes the real estate sector an attractive target for money launderers. Criminals may use property investments to hide the origin of illicit funds or as a means to legitimize their proceeds.

- Gaming and gambling: Casinos and other gaming establishments often deal with large amounts of cash, making them vulnerable to money laundering activities.

- Precious metals and gemstones: The trade in high-value items such as gold, diamonds, and other precious metals can be used to launder money, as these commodities can be easily bought, sold, or transported across borders.

Red flags and indicators of money laundering activities

Businesses should be vigilant in detecting and reporting suspicious activities that may indicate money laundering. Some common red flags include:

- Unusual transaction patterns: Transactions that deviate from a customer's typical behaviour or are inconsistent with their business profile may signal money laundering activities.

- Complex or illogical transactions: Transactions involving multiple intermediaries, shell companies, or seemingly unrelated parties can indicate money laundering.

- Incomplete or inconsistent documentation: Money launderers may provide false or incomplete information to obscure the origin and destination of funds.

- Rapid movement of funds: Frequent and rapid transfers of funds between accounts or across borders, especially to or from high-risk jurisdictions, can be a sign of money laundering.

By understanding the risks and common indicators of money laundering, businesses can better protect themselves and ensure compliance with anti-money laundering regulations.

Regulatory Framework and Compliance in Malaysia

Bank Negara Malaysia's anti-money laundering regulations

Bank Negara Malaysia (BNM), the country's central bank, plays a crucial role in combating money laundering by implementing the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLA). This act is the primary legislation for preventing and addressing money laundering and terrorism financing in Malaysia. BNM provides guidelines and directives to financial institutions, businesses, and individuals to adhere to these AML regulations.

Compliance requirements for businesses

Businesses operating in Malaysia must comply with AMLA and follow the guidelines issued by BNM. Some of the key compliance requirements include:

- Customer due diligence (CDD): Businesses must conduct proper CDD to identify and verify the identity of their customers, understand the nature of their business relationships, and monitor their transactions to detect suspicious activities.

- Record-keeping: Businesses must maintain records of their customer identification data, transactions, and any other relevant information for at least six years. This helps in the event of an investigation or audit conducted by the authorities.

- Risk assessment: Companies should periodically assess their money laundering and terrorism financing risks and implement appropriate controls and procedures to mitigate them.

- Training and awareness: Businesses should provide regular training and awareness programs to their employees to ensure they understand AML regulations and can identify potential money laundering activities.

Reporting suspicious transactions

Businesses and individuals must report any suspicious transactions to the Financial Intelligence and Enforcement Department of BNM. Suspicious transactions are those that are inconsistent with a customer's known activities, involve large amounts of cash, or have no clear economic or lawful purpose. Timely reporting of such transactions can help authorities detect and prevent money laundering activities and prosecute the individuals involved.

Best Practices to Protect Your Business from Money Laundering Risks in Malaysia

Implementing a comprehensive AML program

To protect your business from money laundering risks, it's essential to establish a comprehensive AML program tailored to your organization's size, complexity, and risk profile. This program should include policies, procedures, and internal controls designed to detect and prevent money laundering activities. Regularly review and update your AML program to ensure its effectiveness and compliance with the latest regulations.

Conducting risk assessments

Regular risk assessments are crucial in identifying and understanding the money laundering risks your business may face. This process involves evaluating your customer base, products and services, geographical location, and delivery channels. By conducting risk assessments, you can identify vulnerabilities and implement targeted measures to mitigate the risks.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

CDD is a critical component of any AML program. This process involves collecting and verifying the identity of your customers, understanding the nature of their business, and assessing the risk associated with each customer. In high-risk situations, such as dealing with politically exposed persons (PEPs) or customers from high-risk countries, Enhanced Due Diligence (EDD) should be applied. EDD involves additional verification measures, ongoing monitoring, and scrutinizing transactions to ensure they are legitimate.

{{cta-guide}}

Ongoing monitoring and transaction surveillance

Continuous monitoring of customer transactions and account activities is vital for identifying unusual or suspicious activities. Implement a transaction surveillance system that can detect and flag potentially suspicious transactions based on predefined parameters. Regularly review and update these parameters to ensure they detect money laundering activities effectively. In addition, train your employees to recognize red flags and report suspicious transactions promptly. By closely monitoring transactions and maintaining a proactive approach, you can protect your business from money laundering risks and ensure compliance with regulatory requirements in Malaysia.

Leveraging Technology to Combat Money Laundering

Role of RegTech in AML compliance

RegTech, or regulatory technology, has emerged as a vital tool in helping businesses meet their AML compliance obligations. RegTech solutions use advanced technologies, such as artificial intelligence (AI), machine learning, and big data analytics, to automate and streamline compliance processes, reduce risks, and improve the detection of money laundering activities. By implementing RegTech solutions, businesses can efficiently manage their AML compliance requirements while minimizing manual errors and reducing operational costs.

Benefits of using AML software solutions

AML software solutions offer several benefits to businesses looking to combat money laundering risks. These include:

- Enhanced risk detection: AML software can analyze vast amounts of data and identify suspicious patterns or trends, enabling businesses to detect money laundering risks more effectively.

- Improved efficiency: Automating compliance processes reduces the time and resources needed to perform manual tasks, allowing businesses to focus on their core operations.

- Reduced false positives: AI and machine learning algorithms can adapt and learn from historical data, reducing the number of false positivesand enhancing the overall accuracy of risk detection.

- Regulatory compliance: AML software ensures businesses remain compliant with evolving regulations by automatically updating rules and processes as needed.

Tookitaki and its AML Solutions

Tookitaki is a leading RegTech company that offers innovative AML solutions to businesses operating in Malaysia and worldwide. As a global leader in financial crime prevention software, Tookitaki revolutionises the fight against financial crime by breaking the siloed AML approach and connecting the community through its innovative Anti-Money Laundering Suite (AMLS) and Anti-Financial Crime (AFC) Ecosystem. Tookitaki's unique community-based approach empowers financial institutions to effectively detect, prevent, and combat money laundering and related criminal activities, resulting in a sustainable AML program with holistic risk coverage, sharper detection, and fewer false alerts.

The AMLS is an end-to-end operating system that modernises compliance processes for banks and fintechs. In parallel, our AFC Ecosystem serves as a community of experts dedicated to uncovering hidden money trails that traditional methods cannot detect. Powered by federated machine learning, the AMLS collaborates with the AFC Ecosystem to ensure that financial institutions stay ahead of the curve in their AML programs.

Conclusion: Navigating Money Laundering Risks in Malaysia with Confidence

As financial crime continues to evolve, money laundering risks in Malaysia remain a serious concern for businesses, especially those in the banking, fintech, and corporate sectors. The consequences of non-compliance, ranging from heavy penalties to reputational loss—are too significant to ignore.

To mitigate these risks, companies must take a proactive approach by building resilient AML programmes, conducting regular risk assessments, and staying aligned with local regulatory updates from Bank Negara Malaysia and global AML standards.

Technology is now a critical enabler in this fight. Advanced solutions like Tookitaki’s FinCense combine AI, machine learning, and federated intelligence to identify complex laundering patterns, reduce false positives, and adapt to emerging threats in real time.

Whether you're a financial institution or a corporate entity, addressing money laundering risks in Malaysia requires both strategic intent and intelligent tools. Tookitaki empowers compliance teams to detect red flags earlier, act faster, and contribute to a safer financial ecosystem.

Protect your business, preserve your reputation, and stay ahead of financial crime—book a demo with Tookitaki today.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

The Role of AML Software in Compliance

Talk to an Expert

Our Thought Leadership Guides

AML Compliance Tools: How to Build a Technology Stack that Holds up Under Examination

Most AML compliance technology problems are not tool problems — they are stack problems. This guide covers the four layers of a complete AML/CFT technology stack, how they need to integrate, and what gaps look like when they don't.

Anti-Money Laundering Software: A Buyer's Guide for Banks and Fintechs

Anti-money laundering software covers four distinct functions: transaction monitoring, sanctions screening, case management, and customer risk scoring. This guide covers how to evaluate each module and what separates platforms that hold up under regulatory examination from those that don't.

AML Compliance Tools: How to Build a Technology Stack that Holds up Under Examination

Most AML compliance technology problems are not tool problems — they are stack problems. This guide covers the four layers of a complete AML/CFT technology stack, how they need to integrate, and what gaps look like when they don't.

Anti-Money Laundering Software: A Buyer's Guide for Banks and Fintechs

Anti-money laundering software covers four distinct functions: transaction monitoring, sanctions screening, case management, and customer risk scoring. This guide covers how to evaluate each module and what separates platforms that hold up under regulatory examination from those that don't.