The Benefits of Using Tookitaki's Solution for AML Compliance in Thailand

.svg)

In today's global financial landscape, anti-money laundering (AML) compliance plays a crucial role in ensuring the integrity of financial systems and preventing illicit activities. As a growing hub for international business and finance, Thailand recognises the significance of AML compliance in maintaining a secure and trustworthy financial environment. Compliance with AML regulations is a legal obligation and a means to protect financial institutions, customers, and the overall economy from the risks associated with money laundering and financial crime.

Tookitaki has emerged as a prominent provider of AML compliance solutions, empowering financial institutions in Thailand and across the globe to tackle the challenges of financial crime effectively. With their innovative technology and expertise in AML compliance, Tookitaki offers comprehensive solutions that enhance detection, reduce false positives, and streamline compliance processes.

By leveraging advanced technologies, Tookitaki enables financial institutions to stay ahead of evolving threats and confidently maintain regulatory compliance. Their commitment to excellence and customer-centric approach make them a trusted partner for organisations striving for robust AML compliance in Thailand.

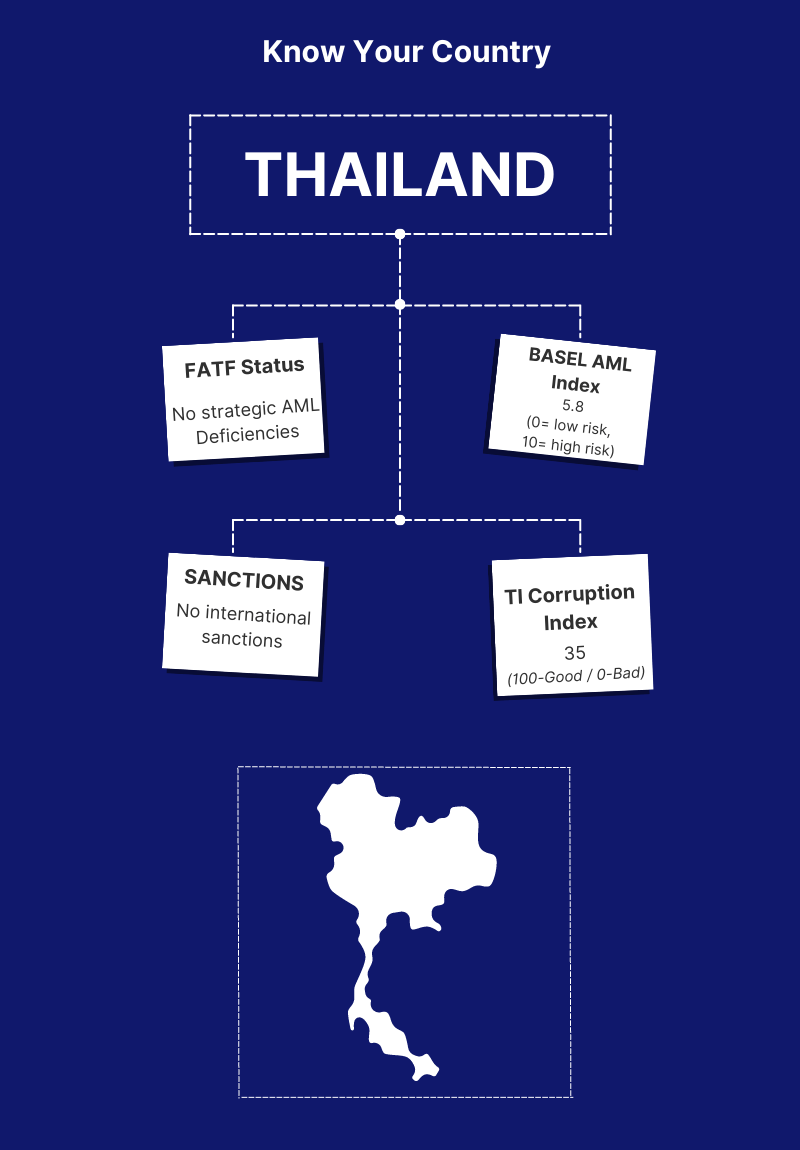

AML Compliance Landscape in Thailand

Overview of the Regulatory Framework for AML in Thailand

Thailand has implemented a comprehensive regulatory framework to combat money laundering and financial crime. Key regulatory bodies and guidelines include:

- Anti-Money Laundering Office (AMLO): The primary authority responsible for implementing AML policies and regulations in Thailand.

- Anti-Money Laundering Act (AMLA): Legislation that sets out the legal framework for AML compliance and enforcement.

- Know Your Customer (KYC) Regulations: Guidelines that require financial institutions to verify customer identities, assess risk profiles, and conduct due diligence.

- Reporting Obligations: Requirements for financial institutions to report suspicious transactions and adhere to transaction monitoring practices.

Challenges Faced by Financial Institutions in Achieving AML Compliance

Financial institutions operating in Thailand encounter several challenges in achieving AML compliance, including:

- Evolving Regulatory Landscape: Adapting to changing AML regulations and guidelines can be a daunting task for financial institutions, as it requires a significant amount of resources, time, and effort. Regulations and guidelines are constantly evolving, and it can be challenging to keep up with the changes and ensure that compliance measures are up-to-date. Additionally, compliance teams must navigate a complex web of regulations and guidelines issued by various regulatory bodies, making compliance a multifaceted and intricate process.

- High False Positive Rates: Traditional AML systems often generate a high volume of false positives, resulting in increased manual effort and operational costs. False positives can occur due to various reasons, such as outdated technology, insufficient data analysis, or rigid rule-based systems that fail to adapt to changing circumstances. These false alerts not only add to the workload of compliance teams but also increase the risk of missing genuine threats. Furthermore, manually reviewing each alert can be time-consuming and costly, leading to delays in investigations and potentially putting the institution at risk of regulatory penalties.

- Rapidly Evolving Financial Crimes: Financial criminals are constantly evolving their tactics to stay ahead of AML systems. They are becoming increasingly sophisticated in their methods, utilizing complex networks of shell companies, cryptocurrencies, and other innovative techniques to hide their illicit activities. This requires financial institutions to be proactive in their approach to AML compliance and stay ahead of emerging threats.

- Resource Constraints: Financial institutions operating in today's dynamic market face a plethora of challenges, including resource constraints. The shortage of skilled personnel, outdated technology infrastructure, and limited financial resources can impede the institution's ability to effectively combat money laundering and financial crime. The hiring and retention of skilled compliance professionals can be costly and challenging, while outdated technology infrastructure can limit the institution's ability to leverage advanced technologies like machine learning. Additionally, limited financial resources can result in budget constraints, preventing the institution from investing in the latest AML solutions.

The Need for Effective and Efficient AML Solutions in the Thai Market

Given the challenges financial institutions face, there is a pressing need for effective and efficient AML solutions in the Thai market. These solutions should offer the following:

- Enhanced Detection Accuracy: AML solutions must leverage advanced technologies like machine learning to improve detection accuracy and reduce false positives.

- Streamlined Compliance Processes: Automation and intelligent workflows can help streamline compliance processes, minimizing manual effort and improving operational efficiency.

- Regulatory Compliance: AML solutions should align with the Thai regulatory framework, enabling financial institutions to meet their compliance obligations.

- Scalability and Adaptability: Solutions should be scalable to accommodate business growth and adaptable to evolving AML regulations and emerging financial crime trends.

Tookitaki's AML compliance solutions address these needs, providing financial institutions in Thailand with the tools and capabilities necessary to overcome AML compliance challenges effectively.

Tookitaki's AML Solution for Thailand

Tookitaki offers a comprehensive AML solution -- the Anti-Money Laundering Suite (AML Suite) -- that empowers financial institutions in Thailand to combat money laundering and financial crime effectively. Its solution combines advanced machine learning algorithms, data analytics, and automation to enhance detection accuracy, streamline compliance processes, and ensure regulatory compliance.

The AML Suite operates as an end-to-end operating system, covering various stages of the compliance process, from initial screening to ongoing monitoring and case management. Banks and fintechs can achieve a seamless workflow, eliminate data silos, and ensure consistent compliance across different modules by having a cohesive and integrated system. The end-to-end approach enhances operational efficiency, reduces manual efforts, and facilitates a more holistic view of AML compliance, enabling financial institutions to stay ahead of evolving risks.

Modules within the AML Suite

Smart Screening Solutions

- Prospect Screening: This module enables real-time screening capabilities for prospect onboarding. By leveraging smart, AI-powered fuzzy identity matching, it reduces regulatory compliance costs and exposure to risk. Prospect Screening helps financial institutions detect and prevent financial crime by screening potential customers against various watchlists, including sanctions lists, PEP databases, and adverse media. The solution provides efficient and streamlined screening processes, reducing false positive hits and assisting compliance specialists in various scenarios.

- Name Screening: Tookitaki's Name Screening solution utilizes machine learning and Natural Language Processing (NLP) techniques to accurately score and distinguish true matches from false matches across names and transactions, in real-time and batch mode. The solution supports screening against sanctions lists, PEPs, adverse media, and local/internal blacklists, ensuring comprehensive coverage. With 50+ name-matching techniques, support for multiple attributes like name, address, gender, and a built-in transliteration engine, Name Screening provides razor-sharp matching accuracy. The state-of-the-art real-time screening architecture reduces held transactions and improves straight-through processing (STP) for a seamless customer experience.

Dynamic Risk Scoring

- Prospect Risk Scoring: Prospect Risk Scoring (PRS) is a powerful solution that enables financial institutions to onboard prospects with reduced regulatory compliance costs and risk exposure. By defining a set of parameters that correspond to the rules, PRS offers real-time risk scoring capabilities. Financial institutions can leverage PRS to take initial scope, including factors such as address, nationality, gender, occupation, monthly income, and more, into account for risk scoring. The configurable scores for risk categories allow financial institutions to streamline the prospect onboarding process, make informed decisions, and mitigate risks effectively.

- Customer Risk Scoring: Tookitaki's Customer Risk Scoring (CRS) is a core module within the AML Suite, powered by advanced machine learning. CRS provides scalable customer risk rating by dynamically identifying relevant risk indicators across a customer's activity. The solution offers a 360-degree customer risk profile, continuous on-demand risk scoring, and perpetual KYC for ongoing due diligence. With actionable insights based on customer risk scores, financial institutions can make accelerated and informed decisions, ensuring effective risk mitigation.

Transaction Monitoring

Tookitaki's Transaction Monitoring solution is the most comprehensive in the industry, utilizing a first-of-its-kind industry-wide typology repository and AI capabilities. It provides comprehensive risk detection and efficient alert management, offering 100% risk coverage and the ability to detect new suspicious cases. The solution includes automated threshold management, reducing the manual effort involved in threshold tuning by over 70%. With superior pattern-based detection techniques, leveraging typologies that represent real-world red flags, Transaction Monitoring helps financial institutions safeguard against new risks and threats effectively.

Case Manager

The Case Manager within Tookitaki's AML Suite provides compliance teams with a collaborative platform to work seamlessly on cases. The Case Manager includes automation that empowers investigators by automating processes such as case creation, allocation, and data gathering. Financial institutions can configure the Case Manager to improve operational efficiency, reduce manual efforts, and enhance overall effectiveness in managing and resolving cases.

{{cta-ebook}}

Ensuring Compliance with Thai Regulatory Requirements

Tookitaki's solution is designed to align with the regulatory framework and requirements set by the Anti-Money Laundering Office (AMLO) and the Anti-Money Laundering Act (AMLA) in Thailand. By using Tookitaki's solution, financial institutions can ensure adherence to these regulations, reducing compliance risks and potential penalties.

Overall, the benefits of using Tookitaki's solution for AML compliance in Thailand extend beyond improved detection accuracy and streamlined processes. Financial institutions can achieve significant cost savings, optimize resource allocation, and maintain compliance with Thai regulatory requirements, enabling them to effectively combat money laundering and protect their operations and customers from financial crime risks.

Final Thoughts

Tookitaki's solution offers numerous advantages for financial institutions seeking robust AML compliance in Thailand. The benefits include enhanced detection accuracy, streamlined compliance processes, cost savings, and ensuring adherence to Thai regulatory requirements. By leveraging Tookitaki's advanced technology, financial institutions can effectively combat money laundering and financial crime while optimizing operational efficiency and resource allocation.

In today's dynamic and rapidly evolving financial landscape, traditional approaches to AML compliance are no longer sufficient. Financial institutions must harness the power of advanced technology to stay ahead of emerging threats and meet regulatory obligations effectively. Tookitaki's innovative solution combines machine learning, data analytics, and automation to provide comprehensive AML compliance capabilities tailored to the specific needs of the Thai market.

Tookitaki is a trusted partner for financial institutions in Thailand, offering cutting-edge AML compliance solutions. Financial institutions are encouraged to explore Tookitaki's solution further, understand its features and benefits, and book a demo to experience firsthand how it can transform their AML compliance processes. By leveraging Tookitaki's solution, financial institutions can strengthen their defence against money laundering, protect their reputation, and safeguard their customers and the financial ecosystem in Thailand.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

Talk to an Expert

Our Thought Leadership Guides

Reducing False Alerts and Improving AML Detection Rates with Tookitaki's FinCense

False positives overwhelm AML compliance teams while genuine financial crime goes undetected. Tookitaki addresses this two ways: an Alert Prioritization AI Agent that works on top of any legacy system, and FinCense Transaction Monitoring with scenario-based detection and automated threshold tuning.

AML Compliance for Digital Banks in Malaysia: Meeting BNM's Requirements with FinCense

Malaysia's digital banks face BNM's 2023 AML/CFT Policy Document, FATF's updated recommendations, and mounting pressure on eKYC and transaction monitoring standards. Here is how FinCense addresses these requirements.

Living Under the STR Clock: The Growing Pressure on AML Investigators

AML investigators face increasing pressure to make Suspicious Transaction Report decisions under tight timelines and growing alert volumes. Explore the challenges behind STR reporting and the shift toward intelligence-led investigations.