The AUD 3.5 Million Email Scam That Fooled the Government

.svg)

In August 2025, the Australian Federal Police (AFP) uncovered a sophisticated Business Email Compromise scheme that siphoned off 3.5 million Australian dollars from a federal government agency.

The incident has stunned the public sector, revealing how one forged email can pierce layers of bureaucratic control and financial safeguards. It also exposed how vulnerable even well-governed institutions have become to cyber-enabled fraud that blends deception, precision, and human error.

For investigators, this was a major victory. For governments and corporations, it was a wake-up call.

Background of the Scam

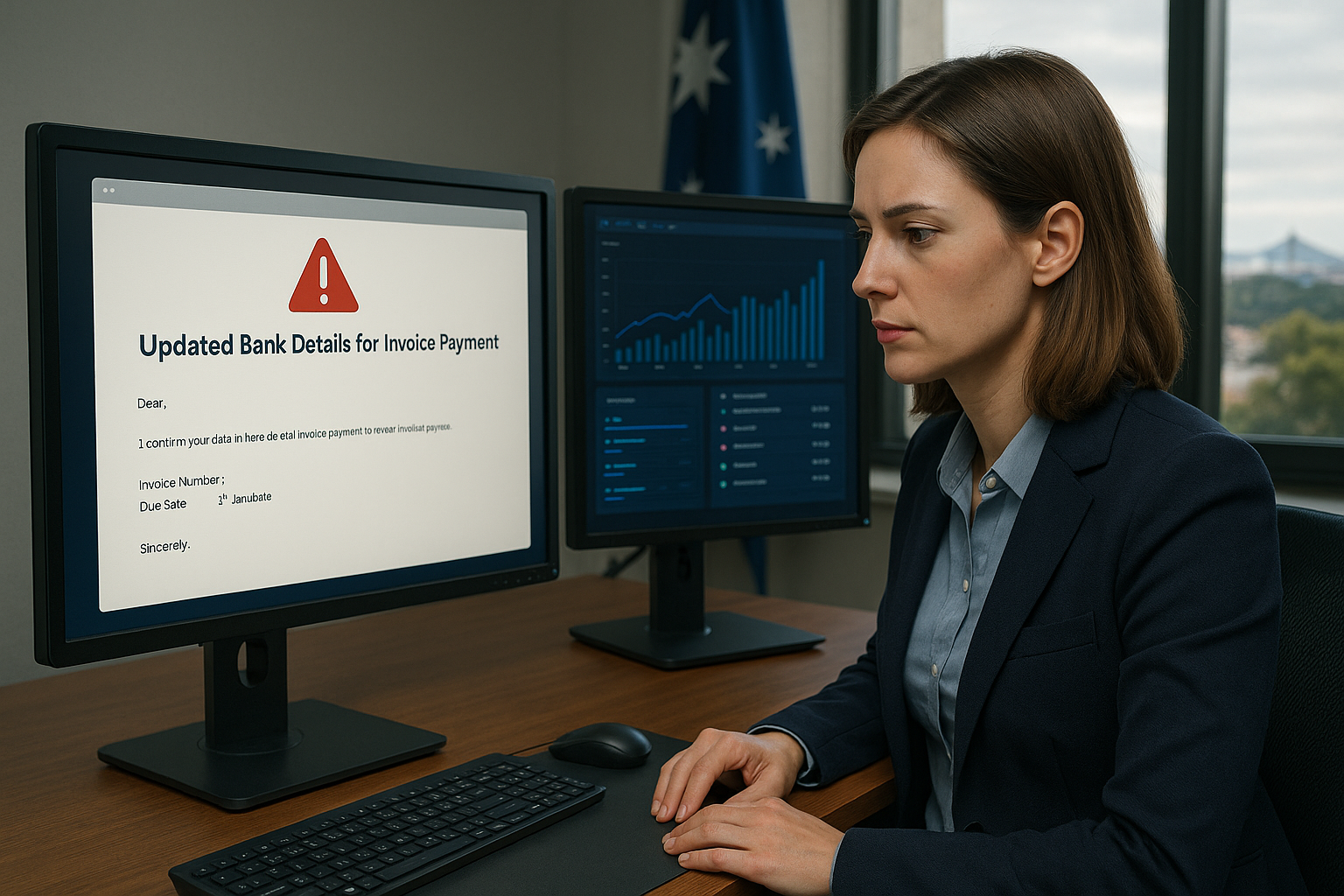

The fraud began with a single deceptive message. Criminals posing as an existing corporate supplier emailed the finance department of a government agency with an apparently routine request: to update the vendor’s banking details.

Everything about the message looked legitimate. The logo, email signature, writing tone, and invoice references matched prior correspondence. Without suspicion, the staff processed several large payments to the new account provided.

That account belonged to the scammer.

By the time discrepancies appeared in reconciliation reports, 3.5 million dollars had already been transferred and partially dispersed through a network of mule accounts. The AFP launched an immediate investigation, working with banks to trace and freeze what funds remained.

Within weeks, a 38-year-old man from New South Wales was arrested and charged with multiple counts of fraud. The case, part of Operation HAWKER, highlighted a surge in email impersonation scams targeting both government and private entities across Australia.

What the Case Revealed

The AFP’s investigation showed that this was not a random phishing attempt but a calculated infiltration of trust. Several insights emerged.

1. Precision Social Engineering

The perpetrator had studied the agency’s procurement process, payment cadence, and vendor language patterns. The fake emails mirrored the tone and formatting of legitimate correspondence, leaving little reason to doubt their authenticity.

2. Human Trust as a Weak Point

Rather than exploiting software vulnerabilities, the fraudsters exploited confidence and routine. The email arrived at a busy time, used an authoritative tone, and demanded urgency. It was designed to bypass logic by appealing to habit.

3. Gaps in Verification

The change in banking details was approved through email alone. No secondary confirmation, such as a phone call or secure vendor portal check, was performed. In modern finance operations, this single step remains the most common point of failure.

4. Delayed Detection

Because the transaction appeared legitimate, no automated alert was triggered. Business Email Compromise schemes often leave no digital trail until funds are gone, making recovery exceptionally difficult.

This was a crime of psychology more than technology. The fraudster never hacked a system. He hacked human behaviour.

Impact on Government and Public Sector Entities

The financial and reputational fallout was immediate.

1. Loss of Public Funds

The stolen 3.5 million dollars represented taxpayer money intended for legitimate projects. While part of it was recovered, the incident forced a broader review of how government agencies manage vendor payments.

2. Operational Disruption

Following the breach, payment workflows across several departments were temporarily suspended for review. Staff were reassigned to audit teams, delaying genuine transactions and disrupting supplier relationships.

3. Reputational Scrutiny

In a climate of transparency, even a single lapse in safeguarding public money draws intense media and political attention. The agency involved faced questions from oversight bodies and the public about how a simple email could override millions in internal controls.

4. Sector-Wide Warning

The attack exposed how Business Email Compromise has evolved from a corporate nuisance into a national governance issue. With government agencies managing vast supplier ecosystems, they have become prime targets for impersonation and payment fraud.

Lessons Learned from the Scam

The AFP’s findings offer lessons that extend far beyond this one case.

1. Verify Before You Pay

Every bank detail change should be independently verified through a trusted communication channel. A short phone call or video confirmation can prevent multi-million-dollar losses.

2. Email Is Not Identity

A familiar name or logo is no proof of authenticity. Fraudsters register look-alike domains or hijack legitimate accounts to deceive recipients.

3. Segregate Financial Duties

Dividing invoice approval and payment execution creates built-in checks. Dual approval for high-value transfers should be non-negotiable.

4. Train Continuously

Cybersecurity training must evolve with threat patterns. Staff should be familiar with red flags such as urgent tone, sudden banking changes, or secrecy clauses. Awareness converts employees from potential victims into active defenders.

5. Simulate Real Threats

Routine phishing drills and simulated payment redirection tests keep defences sharp. Detection improves dramatically when teams experience realistic scenarios.

The AFP noted that no malware or technical breach was involved. The scammer simply persuaded a person to trust the wrong email.

The Role of Technology in Prevention

Traditional financial controls are built to detect anomalies in customer behaviour, not subtle manipulations in internal payments. Modern Business Email Compromise bypasses those defences by blending seamlessly into legitimate workflows.

To counter this new frontier of fraud, institutions need dynamic, intelligence-driven monitoring systems capable of connecting behavioural and transactional clues in real time. This is where Tookitaki’s FinCense and the AFC Ecosystem play a pivotal role.

Typology-Driven Detection

FinCense continuously evolves through typologies contributed by over 200 financial crime experts within the AFC Ecosystem. New scam patterns, including Business Email Compromise and invoice redirection, are incorporated quickly into its detection models. This ensures early identification of suspicious payment instructions before funds move out.

Agentic AI

At the heart of FinCense lies an Agentic AI framework. It analyses transactions, context, and historical data to identify unusual payment requests. Each finding is fully explainable, providing investigators with clear reasoning in natural language. This transparency reduces investigation time and builds regulator confidence.

Federated Learning

FinCense connects institutions through secure, privacy-preserving collaboration. When one organisation identifies a new fraud pattern, others benefit instantly. This shared intelligence enables industry-wide defence without compromising data security.

Smart Case Disposition

Once a suspicious event is flagged, FinCense generates automated case summaries and prioritises critical alerts for immediate human review. Investigators can act quickly on the most relevant threats, ensuring efficiency without sacrificing accuracy.

Together, these capabilities enable organisations to move from reactive investigation to proactive protection.

Moving Forward: Building a Smarter Defence

The $3.5 million case demonstrates that financial crime is no longer confined to the private sector. Public institutions, with complex payment ecosystems and high transaction volumes, are equally at risk.

The path forward requires collaboration between technology providers, regulators, and law enforcement.

1. Strengthen Human Vigilance

Human verification remains the strongest firewall. Agencies should reinforce protocols for vendor communication and empower staff to question irregular requests.

2. Embed Security by Design

Payment systems must integrate verification prompts, behavioural analytics, and anomaly detection directly into workflow software. Security should be part of process design, not an afterthought.

3. Invest in Real-Time Analytics

With payments now processed within seconds, detection must happen just as fast. Real-time transaction monitoring powered by AI can flag abnormal patterns before funds leave the account.

4. Foster Industry Collaboration

Initiatives like the AFP’s Operation HAWKER show how shared intelligence can accelerate disruption. Financial institutions, fintechs, and government bodies should exchange anonymised data to map and intercept fraud networks.

5. Rebuild Public Trust

Transparent communication about risks, response measures, and preventive steps strengthens public confidence. When agencies openly share what they have learned, others can avoid repeating the same mistakes.

Conclusion: A Lesson Written in Lost Funds

The $3.5 million scam was not an isolated lapse but a symptom of a broader challenge. In an era where every transaction is digital and every identity can be imitated, trust has become the new battleground.

A single forged email bypassed audits, cybersecurity systems, and years of institutional experience. It proved that financial crime today operates in plain sight, disguised as routine communication.

The AFP’s rapid response prevented further losses, but the lesson is larger than the recovery. Prevention must now be as intelligent and adaptive as the crime itself.

The fight against Business Email Compromise will be won not only through stronger technology but through stronger collaboration. By combining collective intelligence with AI-driven detection, the public sector can move from being a target to being a benchmark of resilience.

The scam was a costly mistake. The next one can be prevented.

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Experience the most intelligent AML and fraud prevention platform

Top AML Scenarios in ASEAN

The Role of AML Software in Compliance

Talk to an Expert

Our Thought Leadership Guides

Reducing False Alerts and Improving AML Detection Rates with Tookitaki's FinCense

False positives overwhelm AML compliance teams while genuine financial crime goes undetected. Tookitaki addresses this two ways: an Alert Prioritization AI Agent that works on top of any legacy system, and FinCense Transaction Monitoring with scenario-based detection and automated threshold tuning.

AML Compliance for Digital Banks in Malaysia: Meeting BNM's Requirements with FinCense

Malaysia's digital banks face BNM's 2023 AML/CFT Policy Document, FATF's updated recommendations, and mounting pressure on eKYC and transaction monitoring standards. Here is how FinCense addresses these requirements.

Living Under the STR Clock: The Growing Pressure on AML Investigators

AML investigators face increasing pressure to make Suspicious Transaction Report decisions under tight timelines and growing alert volumes. Explore the challenges behind STR reporting and the shift toward intelligence-led investigations.